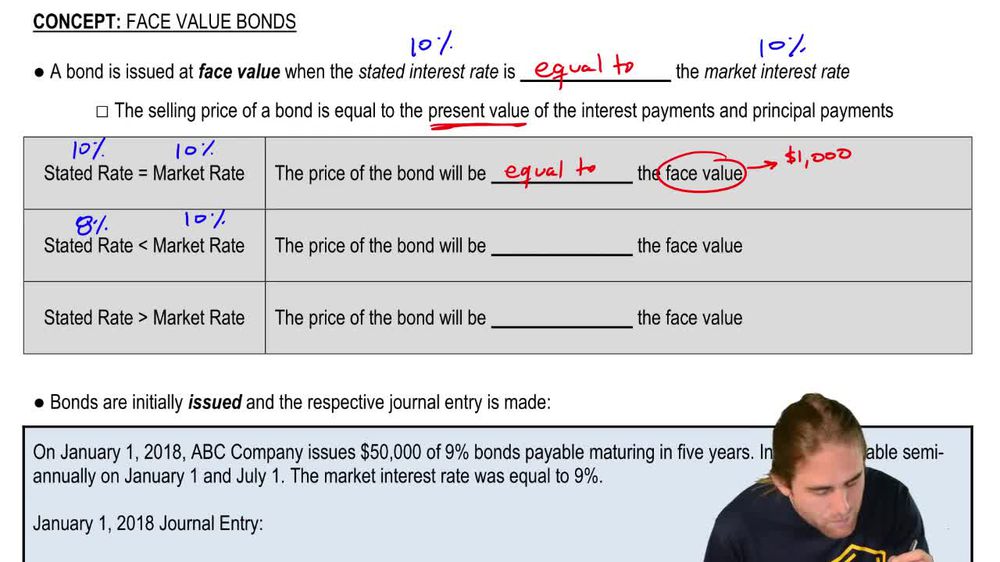

A bond is issued at face value when the stated interest rate equals the market interest rate. This means the bond sells for its principal amount, also called par value.

What is the typical face value of a bond?

The typical face value of a bond is \$1,000. However, companies may issue many bonds, resulting in a much larger total face value.

How do you calculate the cash received when a bond is issued at face value?

The cash received equals the face value of the bonds issued. For example, issuing \$50,000 of bonds at face value means receiving \$50,000 in cash.

What is the journal entry for issuing face value bonds?

Debit Cash for the amount received and credit Bonds Payable for the same amount. Both entries are for the face value of the bonds.

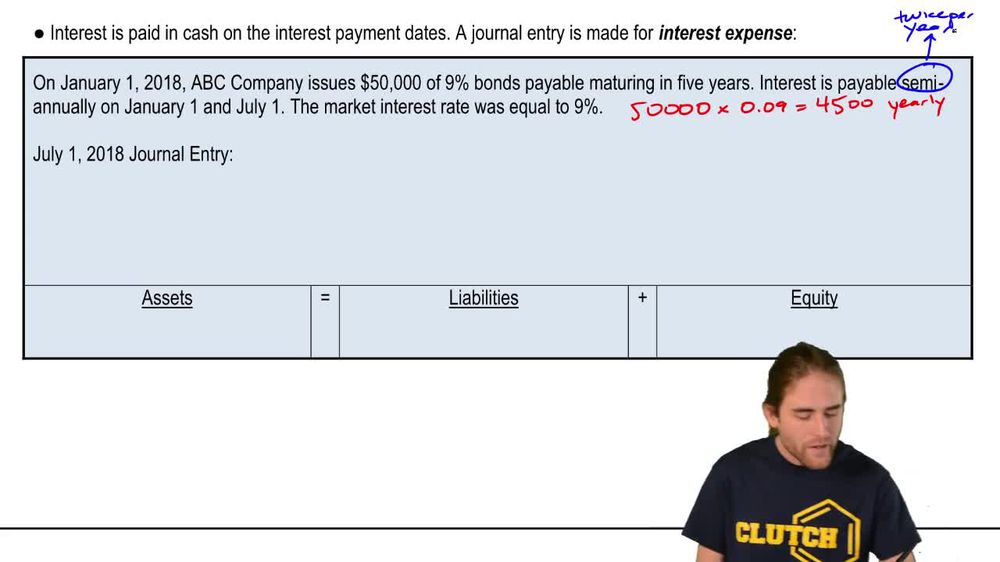

How is interest expense calculated for face value bonds?

Interest expense is calculated as the principal amount times the stated interest rate. If interest is paid semi-annually, divide the yearly interest by two.

How often is interest typically paid on bonds?

Interest is typically paid semi-annually, or twice per year. This means interest payments are made every six months.

What is the journal entry for a semi-annual interest payment on face value bonds?

Debit Interest Expense and credit Cash for the amount of interest paid. The amount is the principal times the stated rate divided by two.

What happens if interest is accrued but not yet paid at year-end?

Interest expense is debited and Interest Payable is credited for the accrued amount. This records the liability to pay interest in the next period.

How is the interest payable liability settled?

When the interest is paid, debit Interest Payable and credit Cash for the amount. This removes the liability from the books.

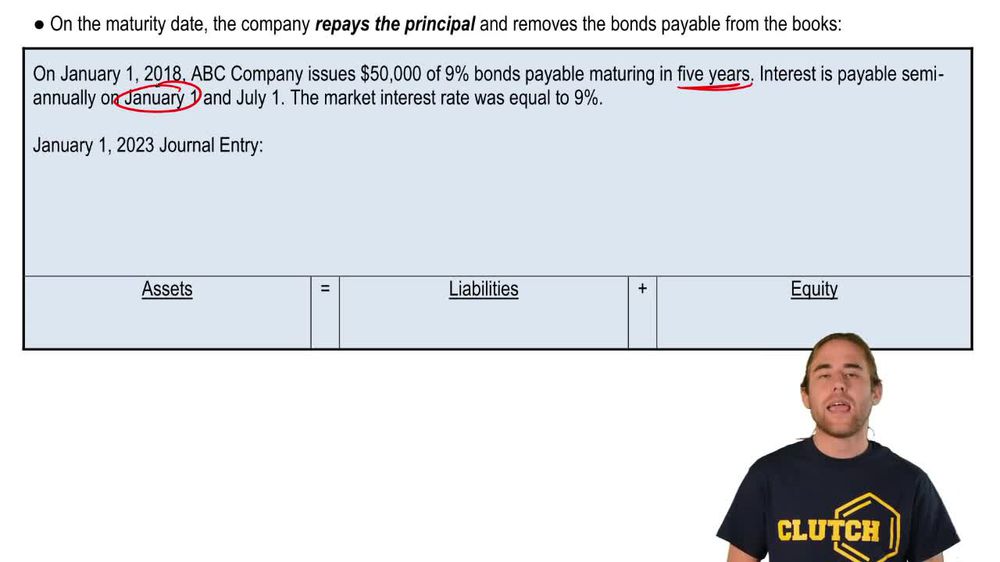

What is the journal entry to repay the principal at bond maturity?

Debit Bonds Payable and credit Cash for the face value of the bonds. This eliminates the liability from the company's books.

What does the bonds payable account always reflect?

The bonds payable account always reflects the face value of the bonds issued. This is true even if the bonds are issued at a discount or premium.

What is the effect of interest expense on equity?

Interest expense reduces equity because it is an expense on the income statement. Expenses decrease net income and, therefore, equity.

What is the relationship between the stated rate and market rate for bonds sold at a discount?

Bonds are sold at a discount when the stated rate is less than the market rate. Investors pay less than face value because the bond offers a lower return.

What is the relationship between the stated rate and market rate for bonds sold at a premium?

Bonds are sold at a premium when the stated rate is greater than the market rate. Investors pay more than face value because the bond offers a higher return.

What does 'par value' mean in the context of bonds?

'Par value' is another term for face value. It is the amount the issuer agrees to pay back at maturity and the basis for interest calculations.

Back

Back

07:36

07:36