Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Long Run Equilibrium definitions

You can tap to flip the card.

Long Run Equilibrium

You can tap to flip the card.

👆

Long Run Equilibrium

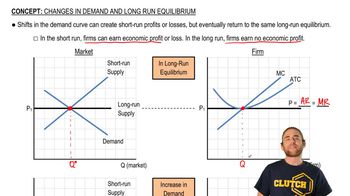

Market condition where price equals minimum average total cost and firms earn zero economic profit after all adjustments.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Long Run Equilibrium quiz #1

Long Run Equilibrium

9 Terms

Long Run Equilibrium

11. Perfect Competition

10 problems

Topic

Perfect Competition and Efficiency

11. Perfect Competition

10 problems

Topic

11. Perfect Competition

11 topics

15 problems

Chapter

Guided course

07:04

Long Run Equilibrium

2396

views

19

rank

1

comments

Terms in this set (15)

Hide definitions

Long Run Equilibrium

Market condition where price equals minimum average total cost and firms earn zero economic profit after all adjustments.

Average Total Cost

Total cost per unit of output, minimized in long run equilibrium, setting the benchmark for market price.

Economic Profit

Surplus earned when price exceeds average total cost, eliminated in the long run by market entry or exit.

Demand Curve

Graphical representation showing how quantity demanded changes with price, shifting right with increased demand.

Supply Curve

Graphical representation showing how quantity supplied changes with price, shifting right as new firms enter.

Marginal Cost

Additional cost incurred from producing one more unit, intersecting marginal revenue at optimal output.

Marginal Revenue

Additional revenue from selling one more unit, equal to price in perfect competition.

Perfect Competition

Market structure with many firms, identical products, and free entry, ensuring zero economic profit in the long run.

Short Run Equilibrium

Temporary market state where firms may earn profits or losses before entry or exit restores long run equilibrium.

Market Entry

Process where new firms join the industry, increasing supply and driving profits toward zero.

Market Exit

Process where firms leave the industry, reducing supply and eliminating losses.

Minimum ATC

Lowest point on the average total cost curve, setting the long run equilibrium price.

Quantity Supplied

Total amount of goods offered by firms at a given price, rising as demand and market entry increase.

Equilibrium Price

Market price where supply equals demand, returning to minimum average total cost after adjustments.

Zero Economic Profit

Outcome where total revenue equals total cost, achieved in the long run as market supply adjusts.

BackBack

BackBack

07:04

07:04