Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Accrual Accounting vs. Cash Basis Accounting definitions

You can tap to flip the card.

Accrual Accounting

You can tap to flip the card.

👆

Accrual Accounting

System recognizing revenue and expenses when they are earned or incurred, regardless of cash movement, providing a more accurate financial picture.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Accrual Accounting vs. Cash Basis Accounting quiz #1

Accrual Accounting vs. Cash Basis Accounting

10 Terms

Accrual Accounting vs. Cash Basis Accounting

3. Accrual Accounting Concepts

10 problems

Topic

Revenue Recognition and Expense Recognition

3. Accrual Accounting Concepts

10 problems

Topic

3. Accrual Accounting Concepts

12 topics

14 problems

Chapter

Guided course

04:05

Cash Basis Accounting

3590

views

154

rank

Guided course

06:49

Accrual Accounting

5878

views

139

rank

1

comments

Terms in this set (15)

Hide definitions

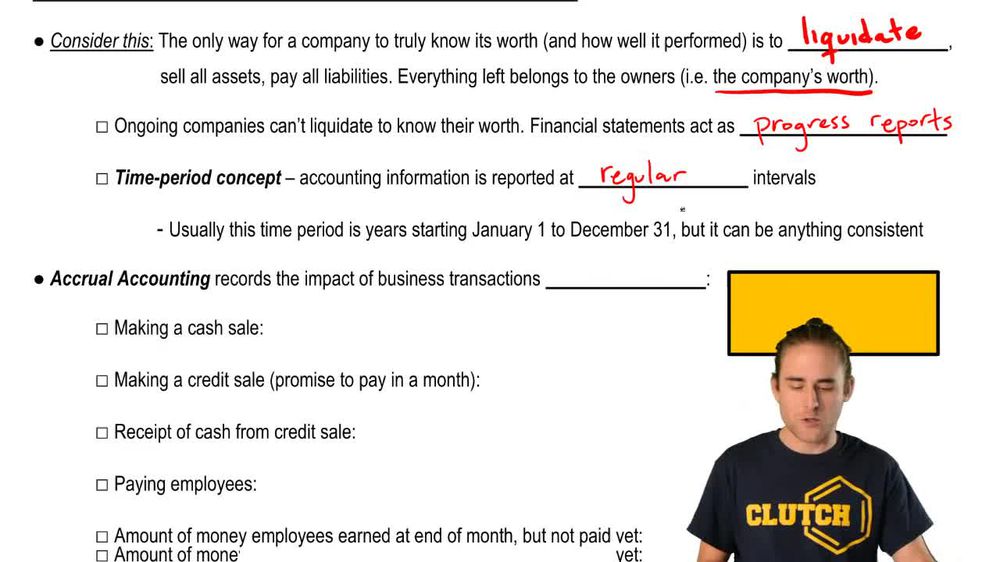

Accrual Accounting

System recognizing revenue and expenses when they are earned or incurred, regardless of cash movement, providing a more accurate financial picture.

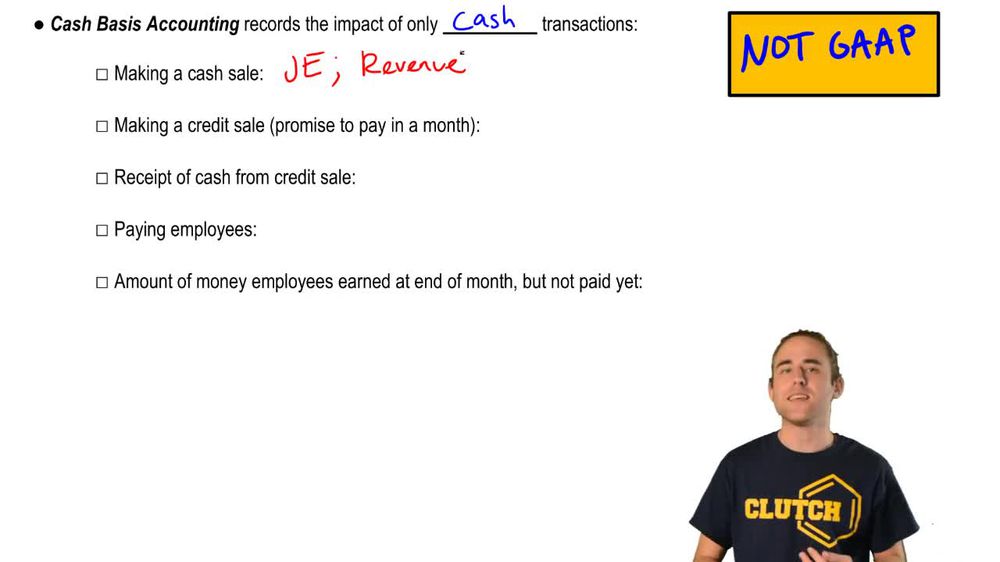

Cash Basis Accounting

Method recording revenue and expenses only when cash is received or paid, often used by small businesses for its simplicity.

GAAP

Set of standardized accounting principles in the United States requiring accrual accounting for financial reporting.

Financial Statements

Periodic reports summarizing a company's financial position and performance, acting as progress reports for stakeholders.

Revenue Recognition

Process of recording income when a product is delivered or a service is completed, not necessarily when cash is received.

Expense Recognition

Recording of costs when they are incurred, matching them to the period in which the related benefit is received.

Journal Entry

Formal record in accounting documenting the details of a business transaction, triggered by specific events.

Accounts Receivable

Amounts owed to a business by customers for goods or services delivered on credit, representing future cash inflows.

Liability

Obligation arising from past transactions, such as unpaid wages or debts, requiring future payment or settlement.

Time Period Concept

Accounting principle dividing business activities into regular intervals, such as months or years, for reporting purposes.

Credit Sale

Transaction where goods or services are provided to a customer with payment to be made at a later date.

Cash Sale

Transaction in which payment is received immediately upon delivery of goods or services.

Matching Principle

Guideline ensuring expenses are recorded in the same period as the revenues they help generate, enhancing accuracy.

Adjusting Entry

Accounting update made at the end of a period to allocate income and expenses to the correct period.

Progress Report

Summary provided by financial statements to show a company's financial status at regular intervals.

BackBack

BackBack

04:05

04:05