When are revenues recorded under accrual accounting?

Under accrual accounting, revenues are recorded when the sale occurs or the service is performed, regardless of when cash is received.

How does the accrual method of accounting determine when to record revenues and expenses?

The accrual method records revenues when they are earned and expenses when they are incurred, regardless of when cash is received or paid.

Under accrual accounting, when is revenue recorded and reported?

Revenue is recorded and reported at the time the product is delivered or the service is completed, not necessarily when cash is received.

What is the primary disadvantage of accrual accounting compared to cash basis accounting?

The primary disadvantage of accrual accounting is that it is more complex to implement and maintain than cash basis accounting.

Which statement accurately describes accrual accounting?

Accrual accounting records transactions as they occur, recognizing revenues when earned and expenses when incurred, regardless of cash flow.

How does cash basis accounting differ from accrual accounting in recognizing revenue and expenses?

Cash basis accounting recognizes revenue only when cash is received and expenses only when cash is paid, while accrual accounting recognizes them when they are earned or incurred.

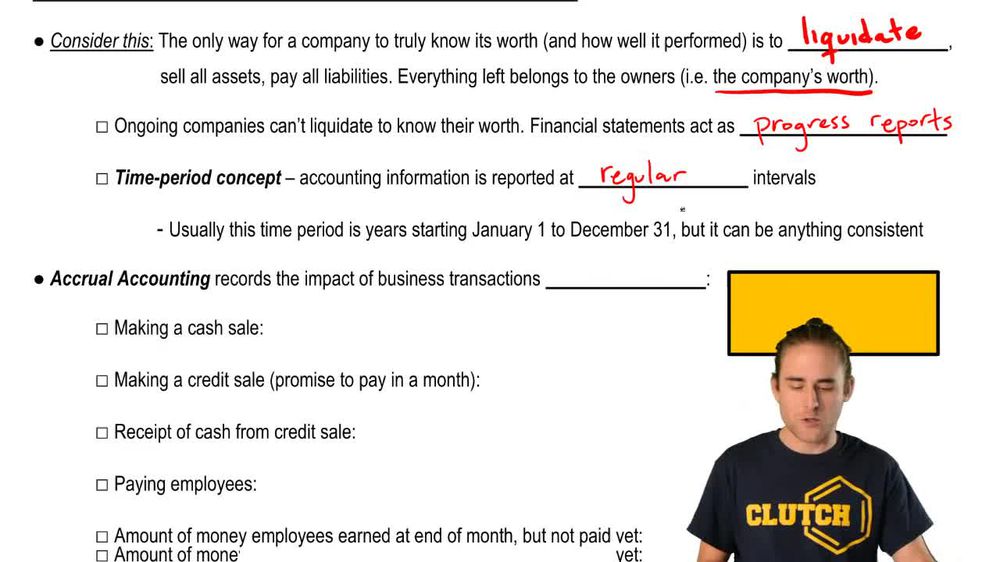

What is the time period concept in accrual accounting?

The time period concept means financial statements are prepared at consistent intervals, such as monthly, quarterly, or yearly. This allows companies to report their financial progress over specific periods without liquidating.

How does accrual accounting handle revenue from credit sales before cash is received?

Accrual accounting records revenue when the product is delivered or service performed, even if payment is deferred. A journal entry is made at the time of sale, and later, a separate entry is made when cash is collected.

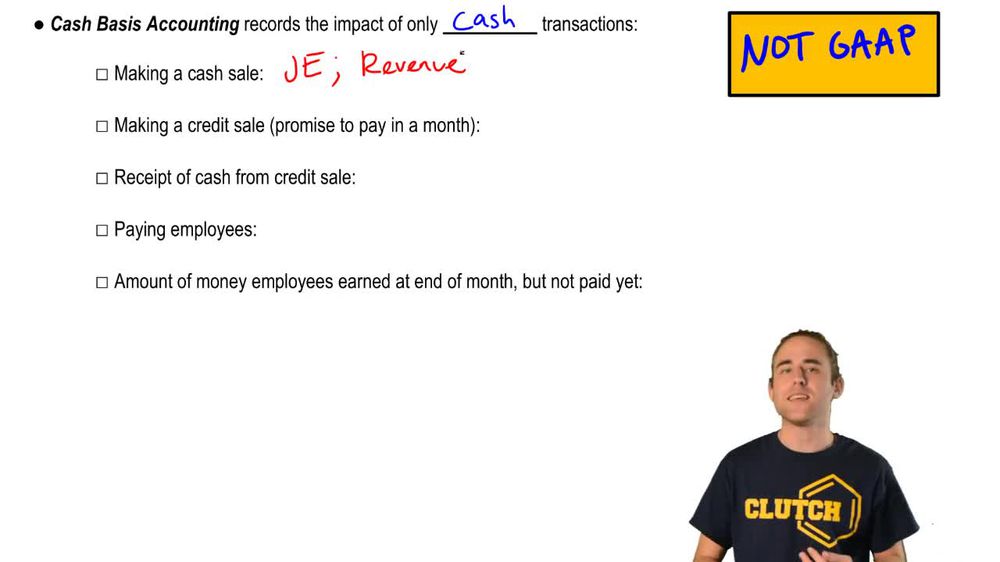

In cash basis accounting, when is revenue from a credit sale recognized?

Revenue from a credit sale is recognized only when cash is actually received from the customer. No journal entry is made at the time of the sale if no cash is exchanged.

How are unpaid employee wages at the end of a reporting period treated under accrual accounting?

Accrual accounting requires a journal entry to accrue the expense for unpaid wages earned during the period, even if payment occurs later. This ensures expenses are matched to the period in which the work was performed.

Back

Back

06:49

06:49