Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Adjusting Entries: Accrued Expenses definitions

You can tap to flip the card.

Accrued Expenses

You can tap to flip the card.

👆

Accrued Expenses

Liabilities for costs incurred and benefits received in a period that remain unpaid at the period's end.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Adjusting Entries: Accrued Expenses quiz #1

Adjusting Entries: Accrued Expenses

21 Terms

Adjusting Entries: Accrued Expenses

3. Accrual Accounting Concepts

10 problems

Topic

Adjusting Entries: Accrued Revenues

3. Accrual Accounting Concepts

10 problems

Topic

3. Accrual Accounting Concepts

12 topics

14 problems

Chapter

Guided course

07:59

Adjusting Journal Entries: Accrued Expenses

2860

views

45

rank

Terms in this set (15)

Hide definitions

Accrued Expenses

Liabilities for costs incurred and benefits received in a period that remain unpaid at the period's end.

Liability

Obligation to pay for benefits already received, recorded on the balance sheet until settled.

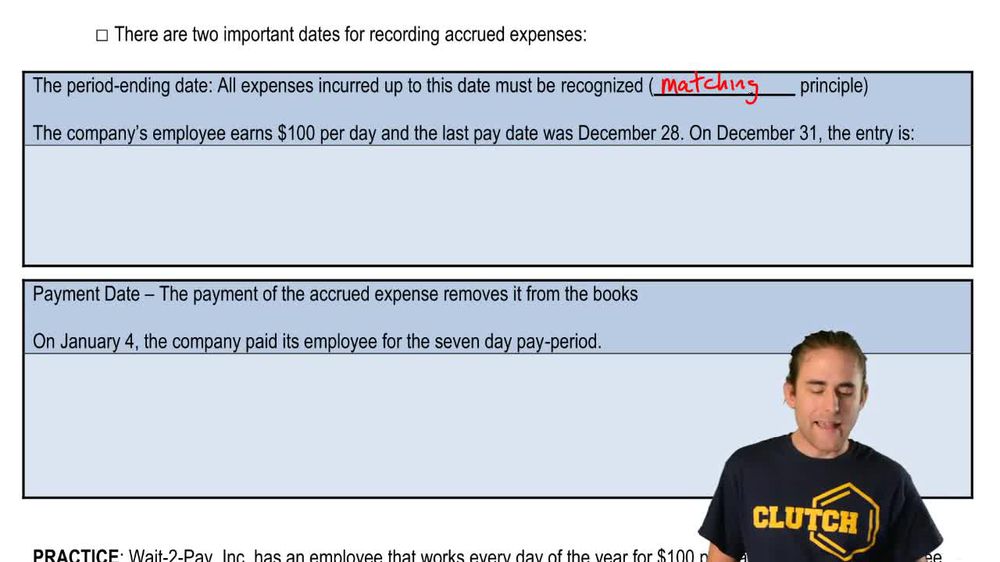

Matching Principle

Accounting rule requiring expenses to be recognized in the same period as the revenues they help generate.

Period Ending Date

Specific date marking the close of an accounting period, triggering the need for adjusting entries.

Wage Expense

Cost recognized for employee services rendered during a period, regardless of payment timing.

Accrued Wage Expense

Liability account representing wages earned by employees but not yet paid at the end of a period.

Debit

Accounting entry increasing assets or expenses, or decreasing liabilities or equity.

Credit

Accounting entry increasing liabilities or equity, or decreasing assets or expenses.

Adjusting Entry

Journal entry made at period end to update accounts for revenues earned or expenses incurred but not yet recorded.

Deferral

Accounting adjustment delaying recognition of revenue or expense to a future period.

Accrual

Accounting method recognizing revenues and expenses when earned or incurred, not when cash is exchanged.

Prepaid Expense

Asset account for payments made in advance for goods or services to be received in future periods.

Cash

Asset representing currency or funds available for immediate use in transactions.

Expense

Outflow of resources or incurrence of obligations resulting from business operations within a period.

Revenue

Income earned from providing goods or services during a specific accounting period.

BackBack

BackBack

07:59

07:59