Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Adjusting Entries: Accrued Revenues definitions

You can tap to flip the card.

Accrued Revenues

You can tap to flip the card.

👆

Accrued Revenues

Earnings recognized before cash is received, typically from delivering goods or services on credit to customers.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Related practice

Recommended videos

Adjusting Entries: Accrued Revenues quiz #1

Adjusting Entries: Accrued Revenues

24 Terms

Adjusting Entries: Accrued Revenues

3. Accrual Accounting Concepts

10 problems

Topic

Adjusting Entries: Depreciation

3. Accrual Accounting Concepts

10 problems

Topic

3. Accrual Accounting Concepts

12 topics

14 problems

Chapter

Guided course

04:56

Adjusting Journal Entries: Accrued Revenues

2241

views

39

rank

Terms in this set (13)

Hide definitions

Accrued Revenues

Earnings recognized before cash is received, typically from delivering goods or services on credit to customers.

Accounts Receivable

Asset representing amounts owed by customers who have received goods or services but have not yet paid.

Asset

Resource owned by a company, such as money owed by customers, that provides future economic benefit.

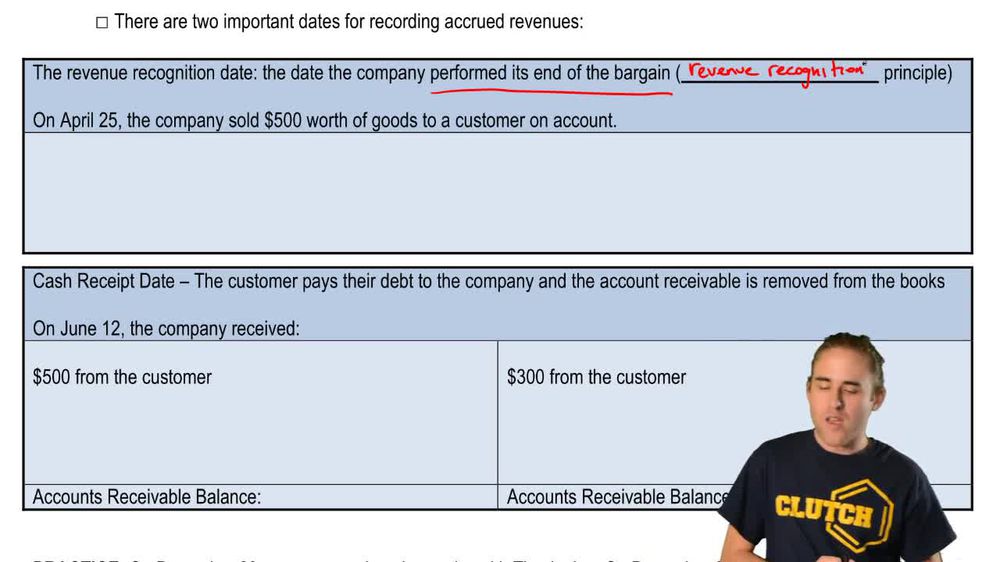

Revenue Recognition Principle

Guideline requiring revenue to be recorded when it is earned, regardless of when cash is received.

Credit Sale

Transaction where goods or services are provided to a customer who agrees to pay at a later date.

Adjusting Entry

Accounting record made at the end of a period to update account balances before preparing financial statements.

Debit

Accounting entry that increases assets or expenses and decreases liabilities or equity.

Credit

Accounting entry that increases liabilities, equity, or revenue and decreases assets or expenses.

Outstanding Balance

Portion of an amount owed by a customer that remains unpaid after a partial payment.

Accrual Accounting

Method where transactions are recorded when they occur, not when cash is exchanged.

On Account

Term indicating a transaction where payment is deferred and will be made at a future date.

IOU

Informal reference to an amount owed by a customer, reflected as an asset until payment is received.

Partial Payment

Situation where a customer pays only a portion of the total amount owed, leaving a remaining balance.

BackBack

BackBack

04:56

04:56