Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Discontinued Operations and Extraordinary Items definitions

You can tap to flip the card.

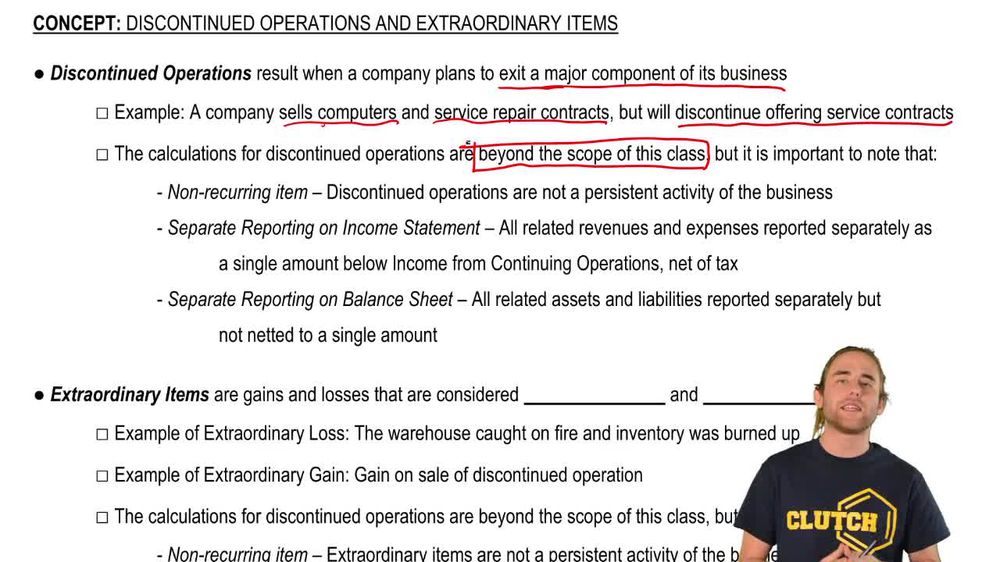

Discontinued Operations

You can tap to flip the card.

👆

Discontinued Operations

Portion of a business a company plans to exit, reported separately at the bottom of the income statement as a single net-of-tax amount.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Discontinued Operations and Extraordinary Items quiz

Discontinued Operations and Extraordinary Items

15 Terms

Discontinued Operations and Extraordinary Items

14. Financial Statement Analysis

10 problems

Topic

Introduction to Ratios

14. Financial Statement Analysis

10 problems

Topic

14. Financial Statement Analysis

15 topics

15 problems

Chapter

Guided course

03:03

Discontinued Operations

550

views

11

rank

Guided course

03:31

Extraordinary Items

424

views

11

rank

Terms in this set (14)

Hide definitions

Discontinued Operations

Portion of a business a company plans to exit, reported separately at the bottom of the income statement as a single net-of-tax amount.

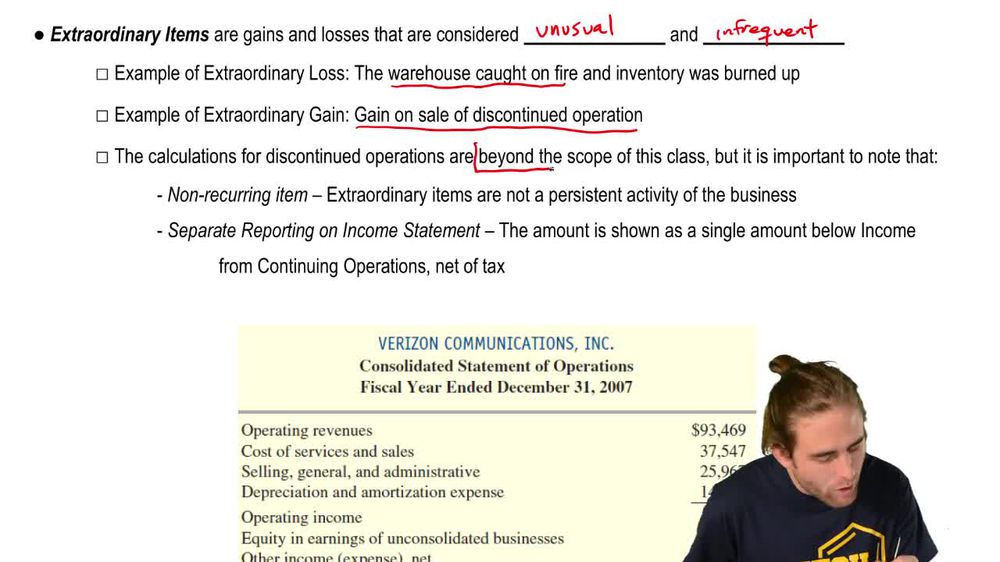

Extraordinary Items

Unusual and infrequent gains or losses, shown separately below continuing operations on the income statement, net of tax.

Income Statement

Financial report displaying revenues, expenses, and profits, with non-recurring items shown separately at the bottom.

Continuing Operations

Ongoing, regular business activities whose results are reported above non-recurring items on the income statement.

Non-Recurring Item

Event not expected to happen regularly, such as discontinued operations or extraordinary items, separated from normal business results.

Net of Tax

Amount shown after deducting related taxes, used for reporting discontinued operations and extraordinary items.

Footnotes

Detailed disclosures in financial statements providing additional information about items like discontinued operations and extraordinary items.

Operating Revenues

Income generated from a company’s main business activities, reported separately from non-recurring items.

Operating Expenses

Costs incurred through normal business operations, distinct from non-recurring items on the income statement.

Extraordinary Gain

Unusual, infrequent profit, such as from selling a business segment, reported separately and net of tax.

Extraordinary Loss

Unusual, infrequent loss, such as from a disaster, reported separately and net of tax on the income statement.

Balance Sheet

Financial statement listing assets and liabilities, with discontinued assets and liabilities shown separately from ongoing items.

Segment

Major component or division of a business, which may be discontinued and reported separately if exited.

Net Income

Final profit figure after all revenues, expenses, discontinued operations, and extraordinary items are accounted for.

BackBack

BackBack

03:03

03:03