Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Five Components of Internal Controls definitions

You can tap to flip the card.

Internal Controls

You can tap to flip the card.

👆

Internal Controls

Policies and procedures designed to safeguard assets, ensure reliable records, and promote compliance, primarily to prevent fraud.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Five Components of Internal Controls quiz #1

Five Components of Internal Controls

40 Terms

Five Components of Internal Controls quiz #2

Five Components of Internal Controls

11 Terms

Five Components of Internal Controls

6. Internal Controls and Reporting Cash

10 problems

Topic

Principles of Control Activities

6. Internal Controls and Reporting Cash

10 problems

Topic

6. Internal Controls and Reporting Cash

8 topics

15 problems

Chapter

Guided course

08:05

Five Components of Internal Controls

1821

views

60

rank

Terms in this set (14)

Hide definitions

Internal Controls

Policies and procedures designed to safeguard assets, ensure reliable records, and promote compliance, primarily to prevent fraud.

COSO Framework

A structured system dividing internal controls into five essential components for effective risk management and fraud prevention.

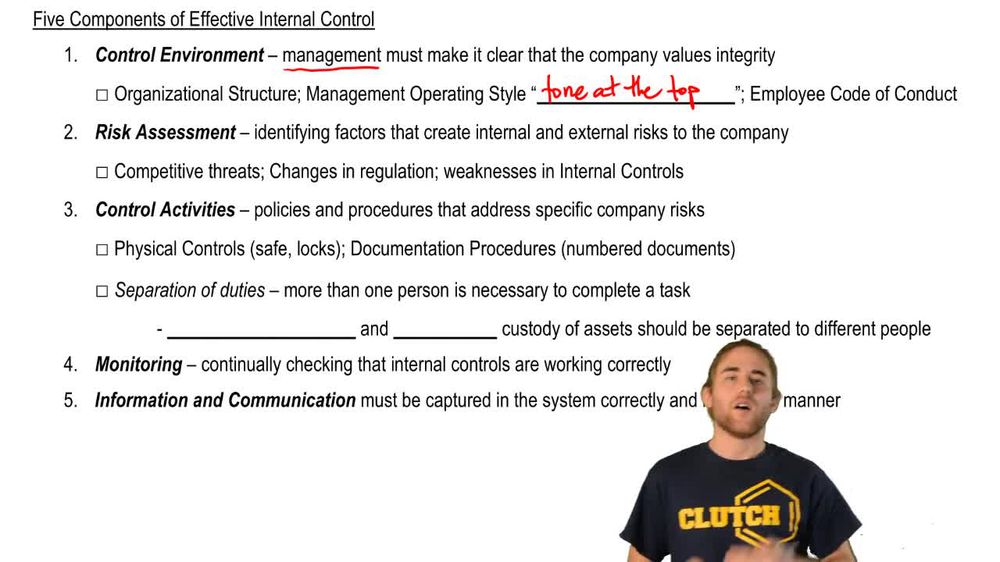

Control Environment

The ethical atmosphere set by management, including organizational structure and codes of conduct, influencing employee behavior.

Tone at the Top

The ethical example set by executives, shaping the honesty and integrity expectations throughout the organization.

Organizational Structure

The arrangement of roles, responsibilities, and authority within a company, impacting how controls are implemented.

Code of Conduct

A formal document outlining expected ethical behavior and standards for employees within an organization.

Risk Assessment

An ongoing process of identifying and evaluating internal and external threats that could exploit weaknesses in controls.

Control Activities

Specific procedures, such as physical safeguards and documentation practices, designed to address identified risks.

Physical Controls

Tangible measures like locks or safes used to protect assets from theft or unauthorized access.

Documentation Procedures

Processes such as using pre-numbered checks to ensure completeness and accuracy in financial records.

Separation of Duties

Dividing responsibilities among multiple people to reduce the risk of errors or fraud by any single individual.

Monitoring

Continuous evaluation to ensure internal controls are functioning as intended and remain effective over time.

Information and Communication

Systems ensuring timely and accurate capture, processing, and sharing of data necessary for effective operations.

CRIME Mnemonic

A memory aid representing the five components: Control Activities, Risk Assessment, Information and Communication, Monitoring, and Environment.

BackBack

BackBack

08:05

08:05