Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Analysis and Income Statement Presentation definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

US accounting framework established by FASB, characterized by detailed, rules-based standards for financial reporting.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Analysis and Income Statement Presentation quiz

GAAP vs. IFRS: Analysis and Income Statement Presentation

15 Terms

GAAP vs. IFRS: Analysis and Income Statement Presentation

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Statement of Cash Flows

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

05:09

GAAP vs. IFRS: Analysis and Income Statement Presentation

557

views

3

rank

Terms in this set (15)

Hide definitions

GAAP

US accounting framework established by FASB, characterized by detailed, rules-based standards for financial reporting.

IFRS

International accounting standards set by IASB, emphasizing a principles-based approach and global comparability.

FASB

US organization responsible for developing and issuing the official accounting standards known as GAAP.

IASB

International body that formulates and updates IFRS, aiming for consistency in global financial reporting.

Horizontal Analysis

Analytical method comparing financial data across multiple periods to identify trends and growth patterns.

Vertical Analysis

Technique expressing each item in a financial statement as a percentage of a base figure within the same period.

Ratio

Quantitative relationship derived from financial statement figures, used to assess performance and position.

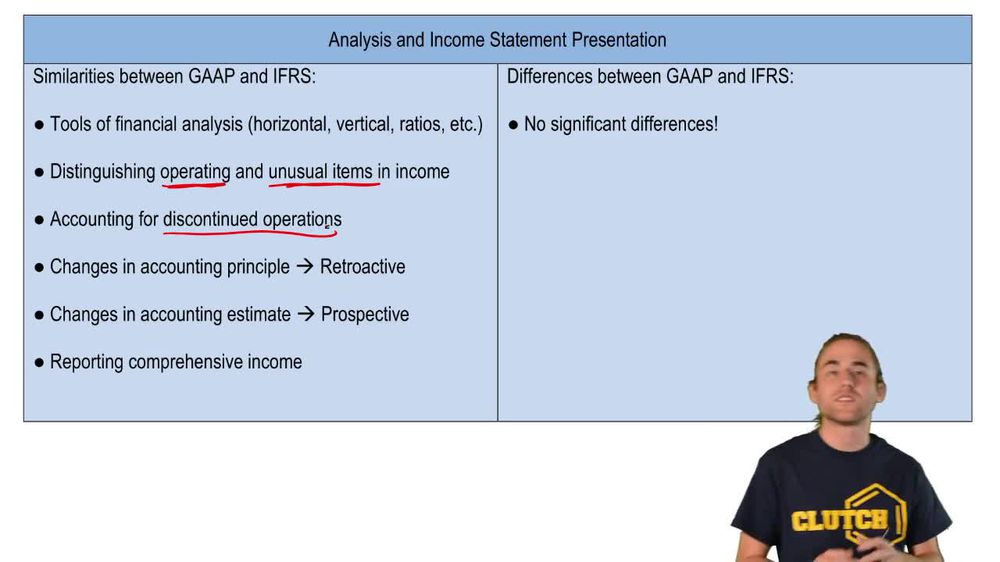

Operating Items

Transactions and events arising from a company's core, day-to-day business activities.

Unusual Items

Non-recurring transactions or events not part of regular business operations, such as one-time losses or gains.

Discontinued Operations

Segments of a business that have been disposed of or are held for sale, reported separately from ongoing activities.

Change in Accounting Principle

Switch in accounting methods, requiring retroactive adjustment to prior financial statements for comparability.

Change in Accounting Estimate

Revision of a previous judgment or assumption, applied prospectively without altering past financial statements.

Comprehensive Income

Total financial performance including net income and other items like unrealized gains and losses not in net income.

Revaluation

Adjustment of the carrying value of long-term assets to reflect current fair value, permitted under IFRS.

LIFO

Inventory valuation method where the most recently acquired items are assumed sold first; not allowed under IFRS.

BackBack

BackBack

05:09

05:09