Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Long Lived Assets definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

US-based accounting framework established by the Financial Accounting Standards Board, guiding financial reporting and asset treatment.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Long Lived Assets quiz

GAAP vs. IFRS: Long Lived Assets

15 Terms

GAAP vs. IFRS: Long Lived Assets

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Liabilities

15. GAAP vs IFRS

9 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

05:02

GAAP vs. IFRS: Long-Lived Assets

398

views

4

rank

Terms in this set (15)

Hide definitions

GAAP

US-based accounting framework established by the Financial Accounting Standards Board, guiding financial reporting and asset treatment.

IFRS

International accounting standards set by the International Accounting Board, used globally for financial reporting and asset valuation.

Long-lived Assets

Resources such as property, plant, equipment, and intangibles expected to provide economic benefits over multiple years.

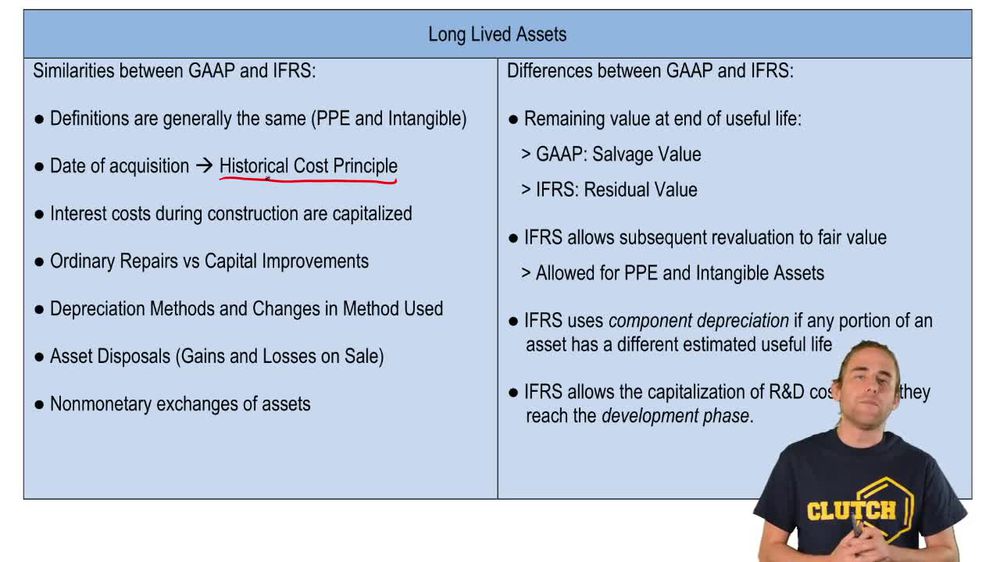

Historical Cost Principle

Accounting rule requiring assets to be recorded at their original purchase price at the time of acquisition.

Property, Plant, and Equipment

Tangible long-term resources like land, buildings, and machinery used in business operations.

Intangibles

Non-physical assets such as patents, trademarks, and copyrights that provide future economic benefits.

Ordinary Repairs

Routine maintenance expenditures that are immediately expensed and do not extend an asset's useful life.

Capital Improvements

Expenditures that increase an asset's value or useful life and are added to the asset's recorded cost.

Depreciation Methods

Approaches for allocating the cost of a tangible asset over its useful life, including straight line and double declining.

Salvage Value

Estimated amount expected to be recovered at the end of an asset's useful life under GAAP.

Residual Value

Term used in IFRS for the expected remaining value of an asset after its useful life.

Fair Value Principle

IFRS concept allowing assets to be revalued to current market value after initial recognition.

Component Depreciation

IFRS practice of depreciating separate parts of an asset individually when they have different useful lives.

Research and Development Costs

Expenditures related to innovation; always expensed under GAAP, but may be capitalized in IFRS after technological feasibility.

Non-monetary Exchanges

Transactions involving the trade of assets without cash, such as swapping equipment, treated similarly under both standards.

BackBack

BackBack

05:02

05:02