Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Recording Differences definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

A set of accounting rules established by FASB, primarily used in the US, emphasizing consistency and historical cost.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Recording Differences quiz

GAAP vs. IFRS: Recording Differences

15 Terms

GAAP vs. IFRS: Recording Differences

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Adjusting Entries

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

04:08

GAAP vs. IFRS: Recordkeeping

505

views

14

rank

Terms in this set (15)

Hide definitions

GAAP

A set of accounting rules established by FASB, primarily used in the US, emphasizing consistency and historical cost.

IFRS

A global set of accounting standards created by the International Accounting Standards Board, allowing more frequent asset revaluation.

Financial Accounting Standards Board

The US organization responsible for developing and maintaining generally accepted accounting principles.

International Accounting Standards Board

The international body that sets accounting standards used in many countries outside the US.

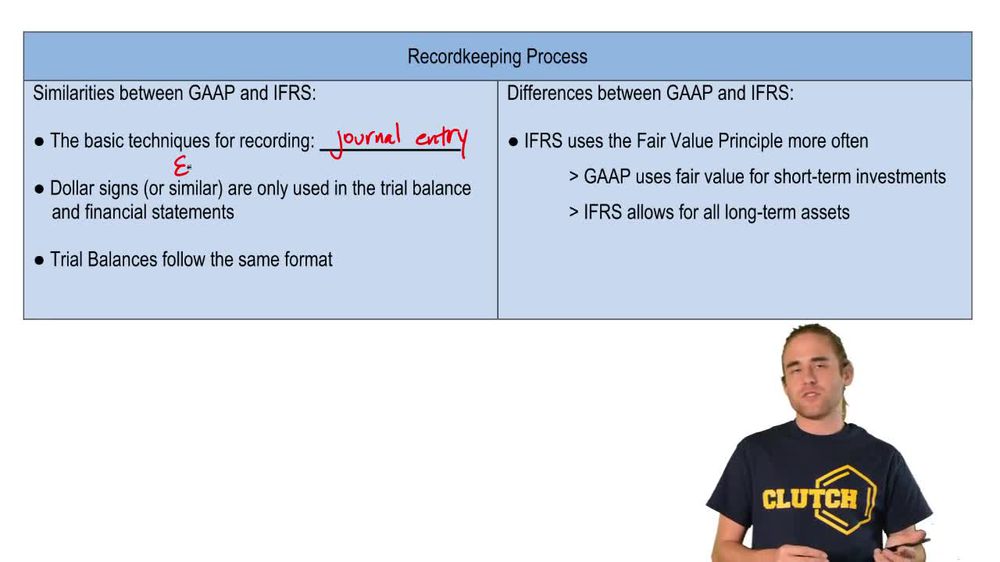

Journal Entry System

A method of recording business transactions using debits and credits to track financial activity.

Debits

Entries on the left side of an account, typically increasing assets or expenses and decreasing liabilities or equity.

Credits

Entries on the right side of an account, usually increasing liabilities or equity and decreasing assets or expenses.

Trial Balance

A list of all accounts and their balances at a specific time, used to verify that total debits equal total credits.

Historical Cost Principle

An accounting guideline requiring assets to be recorded at their original purchase price, regardless of market changes.

Fair Value Principle

A rule allowing assets to be reported at current market value, providing more up-to-date financial information.

Short-Term Investments

Assets expected to be converted to cash within a year, often valued at fair market value under both GAAP and IFRS.

Property, Plant, and Equipment

Long-term tangible assets such as land and buildings, subject to revaluation under IFRS but not typically under GAAP.

Unit of Measure Principle

A concept requiring all financial transactions to be recorded using a consistent currency throughout the accounting records.

Assets

Resources owned by a business, including cash, inventory, and property, listed on the balance sheet.

Liabilities

Obligations or debts owed by a business to outside parties, reported on the balance sheet.

BackBack

BackBack

04:08

04:08