Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Held-to-Maturity (HTM) Securities definitions

You can tap to flip the card.

Held-to-Maturity Investments

You can tap to flip the card.

👆

Held-to-Maturity Investments

Debt securities acquired with the intent and ability to hold until maturity, reported at amortized cost on the balance sheet.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Held-to-Maturity (HTM) Securities quiz #1

Held-to-Maturity (HTM) Securities

10 Terms

Held-to-Maturity (HTM) Securities

7. Receivables and Investments

10 problems

Topic

Equity Method

7. Receivables and Investments

10 problems

Topic

7. Receivables and Investments

10 topics

15 problems

Chapter

Guided course

03:45

Discount on Bonds Receivable

395

views

6

rank

Guided course

03:02

Stated Rate vs. Market Rate for Held-to-Maturity Investments

503

views

10

rank

Guided course

04:53

Premium on Bonds Receivable

382

views

6

rank

Terms in this set (15)

Hide definitions

Held-to-Maturity Investments

Debt securities acquired with the intent and ability to hold until maturity, reported at amortized cost on the balance sheet.

Principal Amount

Face value of a bond, representing the sum to be repaid to the investor at maturity, regardless of purchase price.

Stated Rate

Interest rate specified on the bond, used to calculate periodic interest payments to the bondholder.

Market Rate

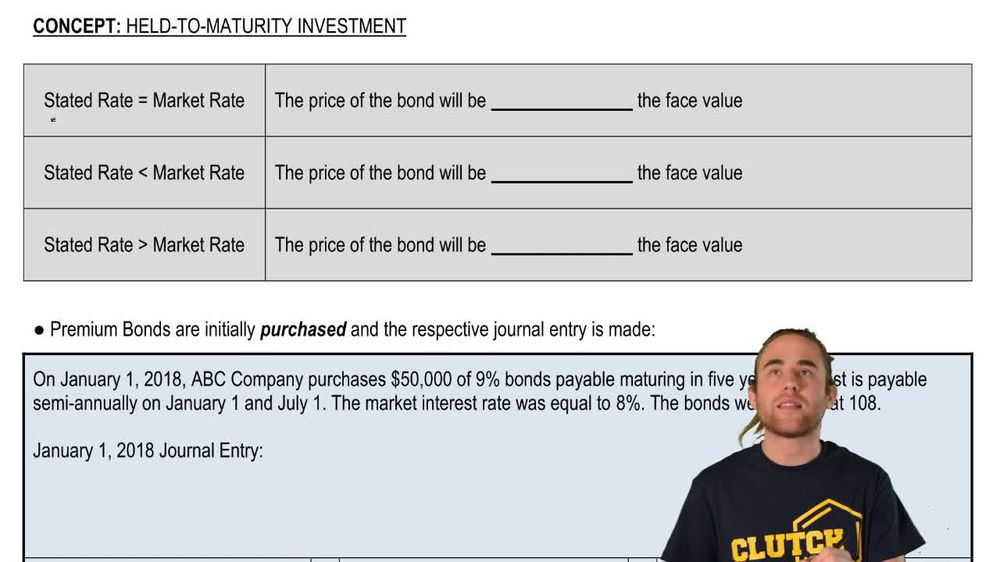

Prevailing interest rate in the market for similar bonds, influencing a bond's selling price as premium or discount.

Premium

Excess of a bond's purchase price over its principal, arising when the stated rate exceeds the market rate.

Discount

Shortfall of a bond's purchase price below its principal, occurring when the stated rate is less than the market rate.

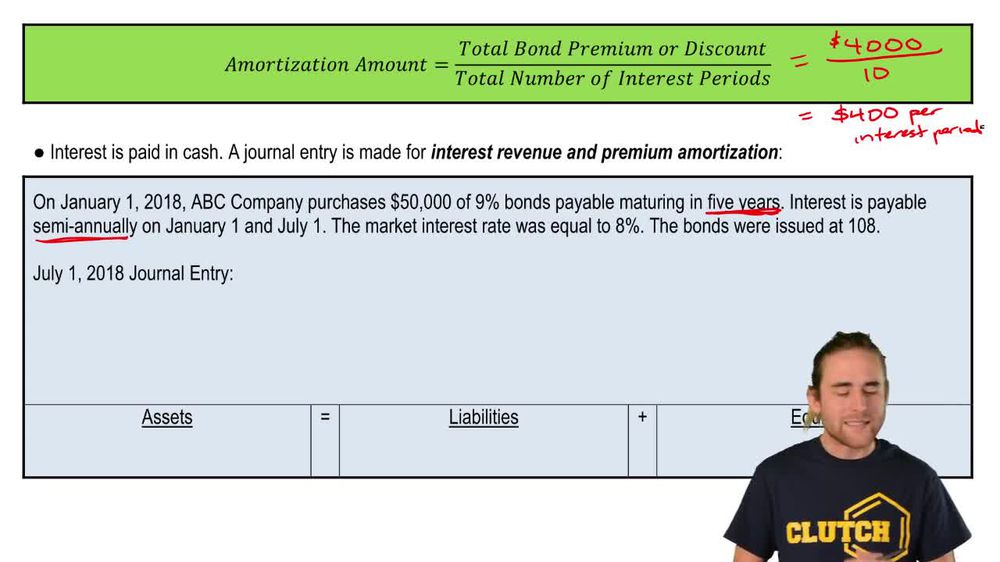

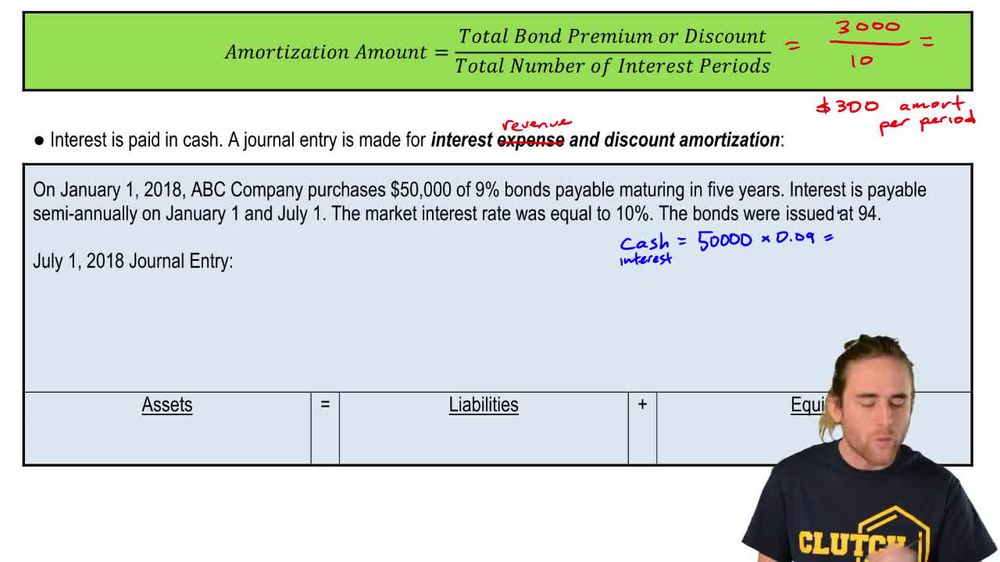

Amortization

Systematic allocation of premium or discount over the bond's life, adjusting the investment's book value to principal at maturity.

Straight-Line Method

Technique dividing total premium or discount evenly across all interest periods, simplifying amortization calculations.

Bonds Receivable

Asset account recording the principal amount of bonds owned by an investor, separate from any premium or discount.

Interest Revenue

Income recognized from earning interest on bonds, including both cash received and amortized premium or discount.

Semiannual Interest

Interest payments made twice a year, requiring division of annual stated rate by two for each payment calculation.

Amortized Cost

Carrying value of an investment after adjusting for cumulative amortization of premium or discount.

Journal Entry

Accounting record documenting transactions such as bond purchases, interest receipts, and amortization adjustments.

Net Assets

Total assets minus total liabilities, affected by changes in investment values and interest revenue recognition.

Balance Sheet

Financial statement presenting assets, liabilities, and equity, including held-to-maturity investments at amortized cost.

BackBack

BackBack

03:45

03:45