What is an inventory error in the context of financial accounting?

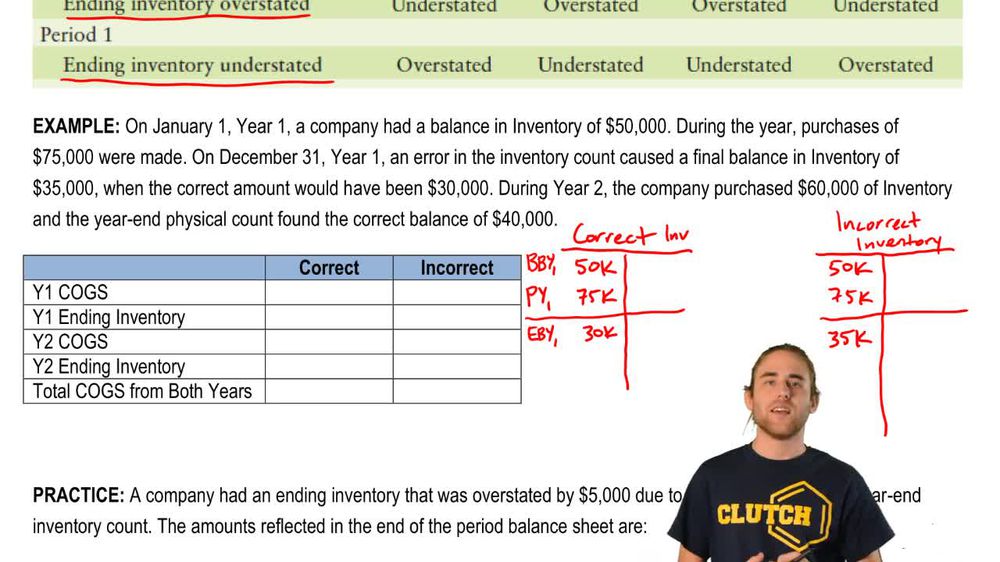

An inventory error occurs when the ending inventory is incorrectly counted, leading to an overstatement or understatement of inventory on the financial statements.

How do inventory errors typically self-correct over time?

Inventory errors usually self-correct after two years if the error is not repeated, as the incorrect ending inventory in one year becomes the incorrect beginning inventory in the next year.

What is the effect of an overstated ending inventory on cost of goods sold (COGS) in the year the error occurs?

An overstated ending inventory causes COGS to be understated in the year the error occurs.

How does an understated ending inventory affect gross profit in the year of the error?

An understated ending inventory causes COGS to be overstated, which reduces gross profit in that year.

If ending inventory is overstated by \$5,000, what is the impact on net income for that year?

Net income will be overstated by \$5,000 because COGS is understated by the same amount.

What happens to the beginning inventory of the following year if an inventory error is made in the current year?

The beginning inventory of the following year will reflect the incorrect ending inventory from the previous year, carrying the error forward.

In the second year after an inventory error, what is the effect on cost of goods sold if the error is not repeated?

COGS in the second year will be adjusted in the opposite direction, correcting the previous year's error.

How does an inventory error affect the total cost of goods sold over two years?

The total COGS over the two years remains the same, as the error in the first year is offset by the correction in the second year.

What is the formula for calculating cost of goods sold (COGS)?

Back

Back

09:45

09:45