Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Investing Activities definitions

You can tap to flip the card.

Investing Activities

You can tap to flip the card.

👆

Investing Activities

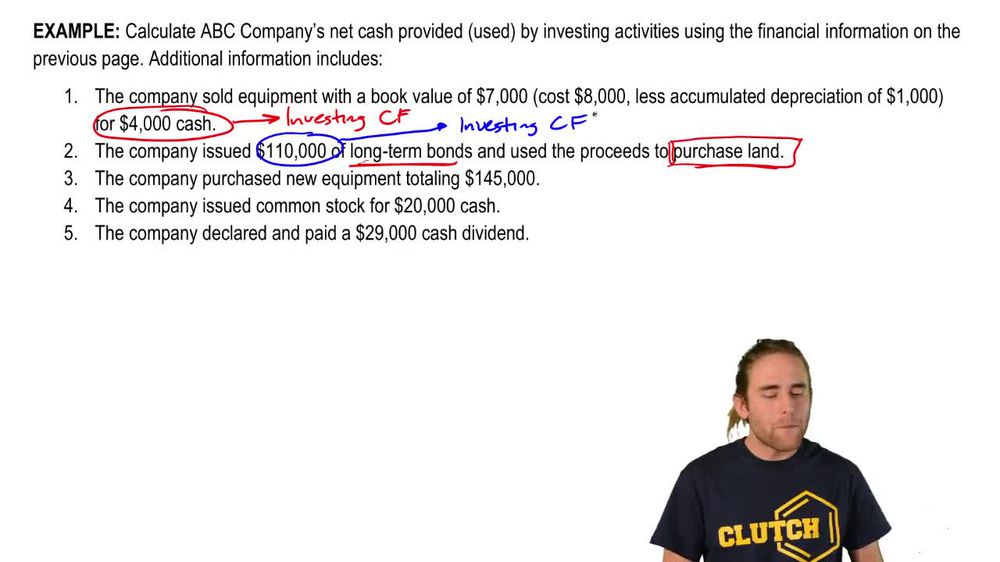

Section of the cash flow statement focused on transactions involving long-term assets such as equipment, land, and investments.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Investing Activities quiz #1

Investing Activities

10 Terms

Investing Activities

13. Statement of Cash Flows

10 problems

Topic

Financing Activities

13. Statement of Cash Flows

10 problems

Topic

13. Statement of Cash Flows

6 topics

15 problems

Chapter

Guided course

08:04

Investing Activities Summary

1353

views

23

rank

Guided course

12:23

Investing Activities

1024

views

20

rank

1

comments

Terms in this set (15)

Hide definitions

Investing Activities

Section of the cash flow statement focused on transactions involving long-term assets such as equipment, land, and investments.

Long-term Assets

Resources like equipment, land, and buildings expected to provide benefits for more than one year and tracked in investing activities.

Plant Assets

Tangible long-term resources such as equipment and buildings used in operations and subject to depreciation.

Intangibles

Non-physical long-term resources like patents or trademarks, included in investing activities when bought or sold.

Cash Inflow

Money received from selling long-term assets or investments, recorded in the investing section of the cash flow statement.

Cash Outflow

Money paid to acquire long-term assets or investments, shown as a negative amount in the investing section.

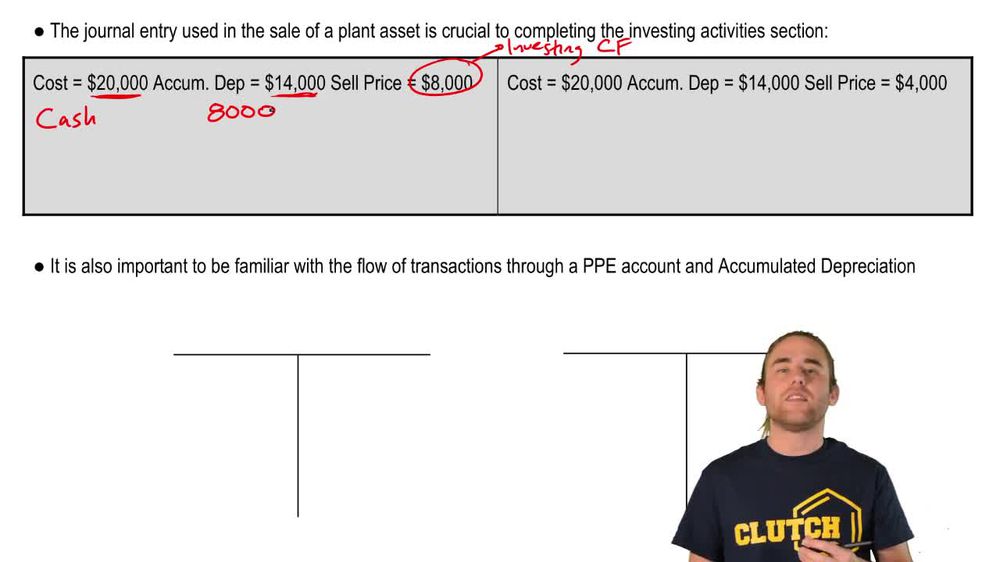

Journal Entry

Accounting record that documents the details of asset sales, including cash received, cost, and accumulated depreciation.

Historical Cost

Original purchase price of a long-term asset, used in journal entries to remove the asset from the books upon sale.

Accumulated Depreciation

Total depreciation recorded against a long-term asset, reducing its book value and removed when the asset is sold.

Contra Asset

Account that offsets a related asset account, such as accumulated depreciation reducing the value of equipment.

Gain on Sale

Excess of proceeds over the book value when a long-term asset is sold, recorded as a credit in the journal entry.

Loss on Sale

Shortfall when proceeds from selling a long-term asset are less than its book value, recorded as a debit in the journal entry.

Depreciation Expense

Periodic allocation of an asset’s cost over its useful life, increasing accumulated depreciation each period.

Book Value

Net amount of an asset on the books, calculated as historical cost minus accumulated depreciation.

Cash Flow Statement

Financial report summarizing cash inflows and outflows from operating, investing, and financing activities.

BackBack

BackBack

08:04

08:04