Merchandising Company vs. Manufacturing Company definitions Flashcards

Back

BackMerchandising Company vs. Manufacturing Company definitions

You can tap to flip the card.

Control buttons has been changed to "navigation" mode.

1/14

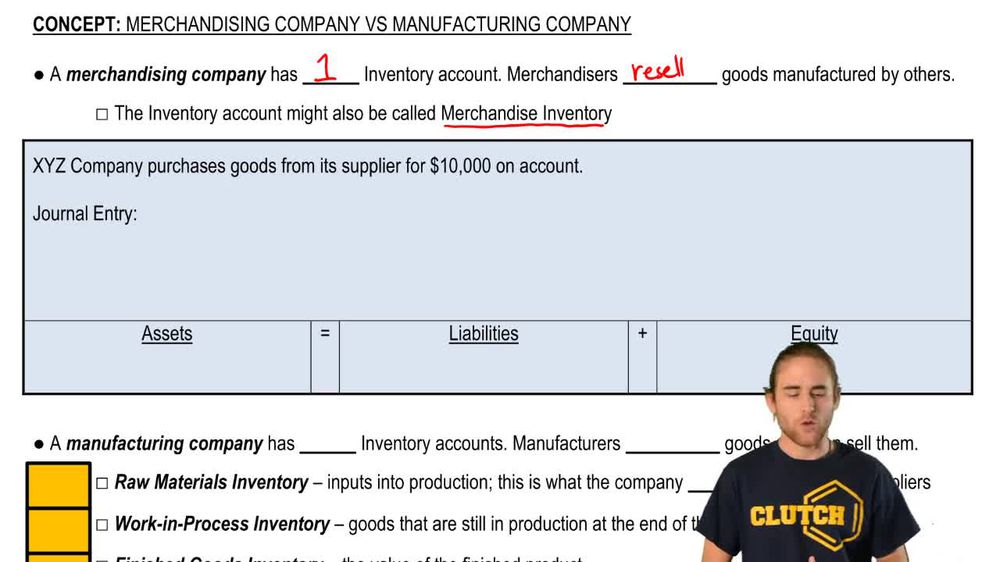

Merchandising Company

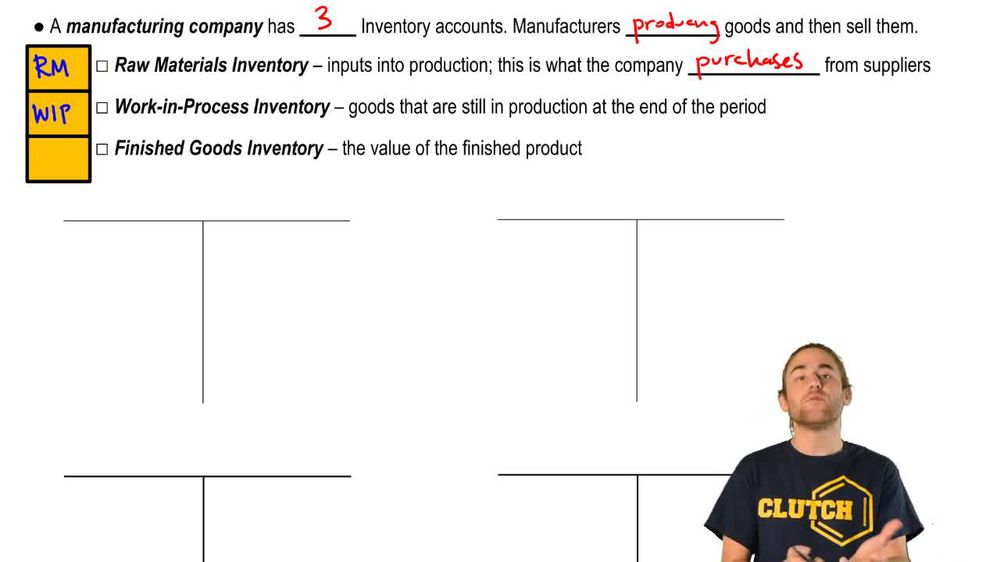

Business that purchases finished products for resale, maintaining a single inventory account for all goods held for sale.Manufacturing Company

Business that produces goods from raw materials, maintaining separate inventory accounts for each production stage.Inventory

Asset account representing goods held for sale or use in production, appearing on the balance sheet.Merchandise Inventory

Single inventory account used by merchandisers to track all purchased goods intended for resale.Raw Materials

Initial inputs acquired for production, such as ingredients or components, before any processing occurs.Work in Process

Inventory account for goods currently being manufactured, including materials, labor, and overhead costs.Finished Goods

Completed products ready for sale to customers, held in a separate inventory account by manufacturers.Perpetual Inventory System

Method where inventory and related accounts are updated continuously with each purchase or sale transaction.Accounts Payable

Liability account representing amounts owed to suppliers for goods or services purchased on credit.Cost of Goods Sold

Expense on the income statement reflecting the cost of inventory sold during a period.Balance Sheet

Financial statement displaying a company's assets, liabilities, and equity at a specific point in time.Income Statement

Financial report summarizing revenues and expenses, including cost of goods sold, over a specific period.Liabilities

Obligations or debts owed by a company to external parties, such as suppliers or lenders.Overhead

Indirect production costs, such as utilities or supervision, included in the value of work in process inventory.

02:03

02:03