What is the primary difference between a merchandising company and a manufacturing company in terms of inventory accounts?

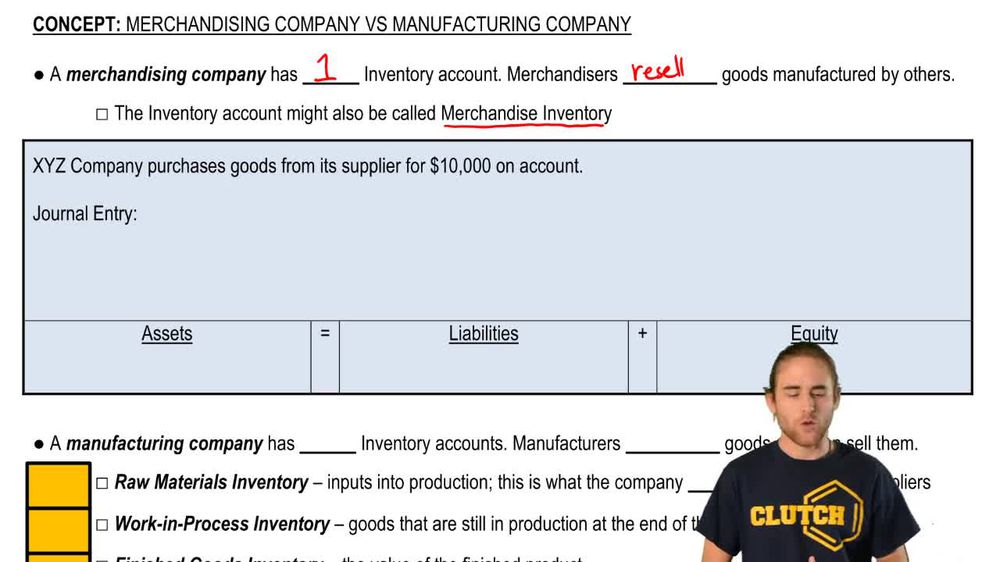

A merchandising company maintains a single inventory account for finished goods, while a manufacturing company maintains three inventory accounts: Raw Materials, Work in Process, and Finished Goods.

How does a merchandising company record the purchase of inventory on account using a perpetual inventory system?

The company debits the Inventory account and credits Accounts Payable, increasing both inventory and liabilities.

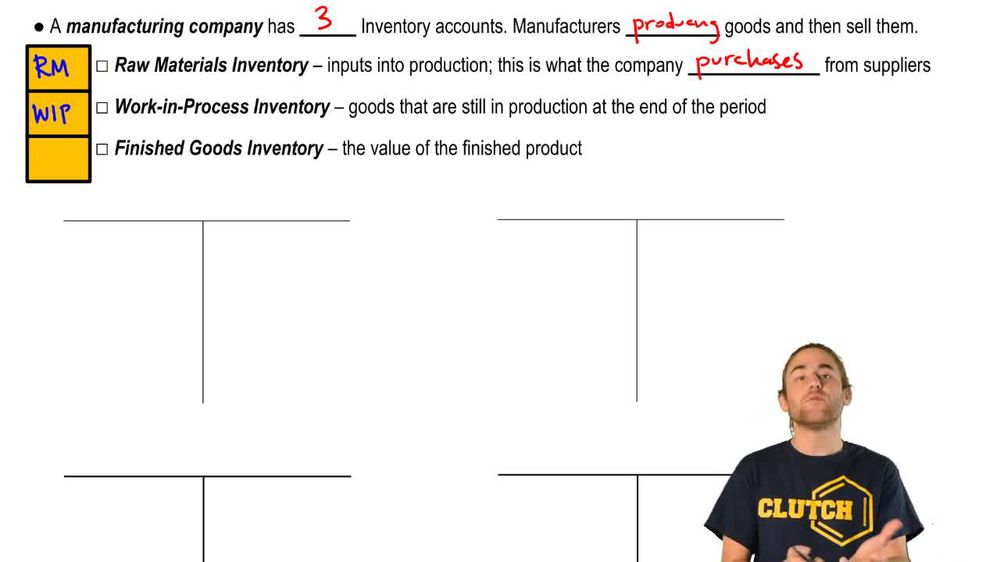

What are the three types of inventory accounts used by manufacturing companies?

Manufacturing companies use Raw Materials, Work in Process, and Finished Goods inventory accounts.

What does the Raw Materials inventory account represent in a manufacturing company?

It represents the initial inputs purchased for production, such as materials that will be used to create finished goods.

What is included in the Work in Process (WIP) inventory account?

WIP includes goods that are currently being manufactured, incorporating costs like raw materials, labor, and overhead.

When are goods transferred from Work in Process to Finished Goods inventory in a manufacturing company?

Goods are transferred from Work in Process to Finished Goods inventory once the manufacturing process is complete.

How is the sale of finished goods recorded in a manufacturing company?

When finished goods are sold, their cost is recorded as Cost of Goods Sold (COGS) on the income statement.

What is the main function of a merchandising company?

A merchandising company purchases finished goods and resells them to customers.

How does the inventory flow in a manufacturing company from purchase to sale?

Inventory flows from Raw Materials to Work in Process, then to Finished Goods, and finally to Cost of Goods Sold when sold.

What is the typical label for the inventory account in a merchandising company?

The inventory account is typically labeled as 'Inventory' or 'Merchandise Inventory.'

What happens to the cost of finished goods when they are sold by a manufacturing company?

The cost is transferred from Finished Goods inventory to Cost of Goods Sold as an expense on the income statement.

Why do manufacturing companies need multiple inventory accounts?

They need multiple accounts to track the different stages of production: raw materials, goods in process, and completed goods.

In a perpetual inventory system, what is the effect of purchasing inventory on account for a merchandising company?

Inventory increases and Accounts Payable increases, reflecting the purchase and the obligation to pay.

What is the final destination of inventory costs in both merchandising and manufacturing companies after a sale?

Inventory costs are ultimately recorded as Cost of Goods Sold on the income statement after a sale.

On which financial statement is finished goods inventory reported for a manufacturing company?

Finished goods inventory is reported on the balance sheet as a current asset for a manufacturing company.

How is work in process inventory generally described in a manufacturing company?

Work in process inventory consists of goods that are in the process of being manufactured, including raw materials that have been used and additional costs such as labor and overhead, but are not yet completed.

Is depreciation on delivery trucks considered manufacturing overhead in a manufacturing company?

Depreciation on delivery trucks is not considered manufacturing overhead; manufacturing overhead typically includes costs related to the production process, such as factory utilities and equipment depreciation, not delivery vehicles.

What type of account is finished goods inventory in a manufacturing company?

Finished goods inventory is a current asset account on the balance sheet of a manufacturing company.

What types of inventory accounts does a manufacturing company maintain?

A manufacturing company maintains three types of inventory accounts: Raw Materials, Work in Process, and Finished Goods.

What is the term for inventory that is partially complete in a manufacturing company?

Inventory that is partially complete in a manufacturing company is known as work in process inventory.

What items are included in raw materials inventory for a manufacturing company?

Raw materials inventory includes the initial inputs purchased for production, such as materials and components that have not yet been used in the manufacturing process.

Back

Back

02:03

02:03