Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Net Accounts Receivable: Allowance for Doubtful Accounts definitions

1 student found this helpful

You can tap to flip the card.

Accounts Receivable

You can tap to flip the card.

👆

Accounts Receivable

Amounts owed by customers for credit sales, recorded as a debit balance and paired with a contra asset to reflect expected uncollectible amounts.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Net Accounts Receivable: Allowance for Doubtful Accounts quiz #1

Net Accounts Receivable: Allowance for Doubtful Accounts

40 Terms

Net Accounts Receivable: Allowance for Doubtful Accounts

7. Receivables and Investments

9 problems

Topic

Net Accounts Receivable: Percentage of Sales Method

7. Receivables and Investments

10 problems

Topic

7. Receivables and Investments

10 topics

15 problems

Chapter

Guided course

05:50

Allowance for Doubtful Accounts

1995

views

55

rank

Guided course

08:06

Net Accounts Receivable: Allowance for Doubtful Accounts

2438

views

60

rank

Terms in this set (15)

Hide definitions

Accounts Receivable

Amounts owed by customers for credit sales, recorded as a debit balance and paired with a contra asset to reflect expected uncollectible amounts.

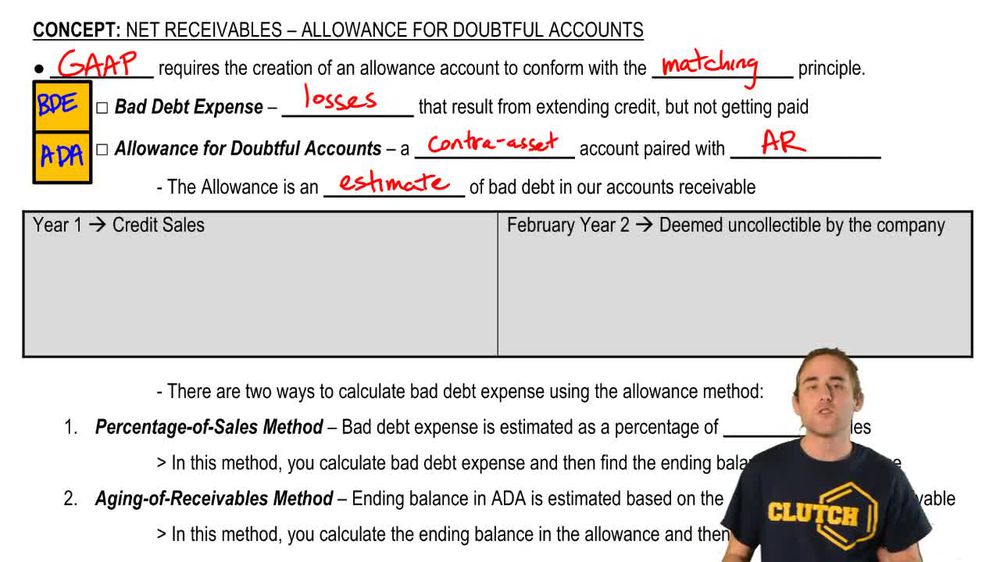

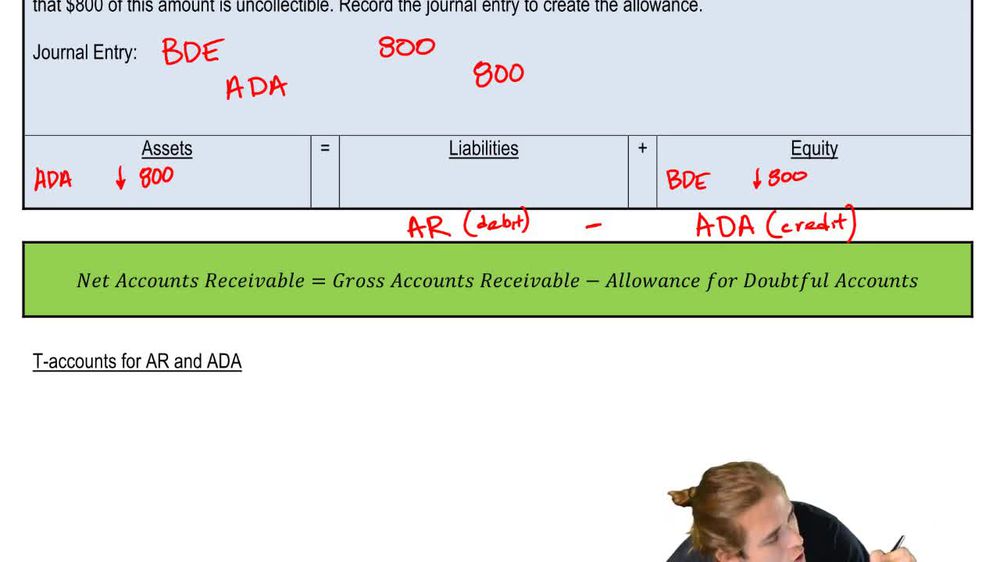

Allowance for Doubtful Accounts

Contra asset account with a credit balance, used to estimate and offset potential losses from uncollectible receivables.

Bad Debt Expense

Estimated loss from credit sales that are not expected to be collected, recorded to match expenses with related revenues.

Matching Principle

Accounting guideline requiring expenses to be recorded in the same period as the revenues they help generate.

Contra Asset

Account with a balance opposite to its related asset, used to reduce the asset's net value on the balance sheet.

Credit Sales

Sales transactions where payment is deferred, creating accounts receivable for the seller.

Direct Write-Off Method

Non-GAAP approach where uncollectible accounts are recognized only when deemed uncollectible, ignoring the matching principle.

Percentage of Sales Method

Estimation technique where bad debt expense is calculated as a set percentage of total credit sales for the period.

Aging of Receivables Method

Estimation approach analyzing receivables by age to determine the required ending balance in the allowance account.

Net Accounts Receivable

Amount expected to be collected from customers, calculated as accounts receivable minus the allowance for doubtful accounts.

Uncollectible Accounts

Receivables deemed unlikely to be collected, typically written off against the allowance for doubtful accounts.

Revenue

Income generated from normal business operations, often recognized at the point of credit sales.

Debit Balance

Normal balance for asset accounts, indicating the amount owed to the company.

Credit Balance

Normal balance for contra asset and liability accounts, used to offset related debit balances.

Write-Off

Accounting action removing uncollectible receivables from the books by reducing both the allowance and accounts receivable.

BackBack

BackBack

05:50

05:50