Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Net Accounts Receivable: Direct Write-off Method definitions

You can tap to flip the card.

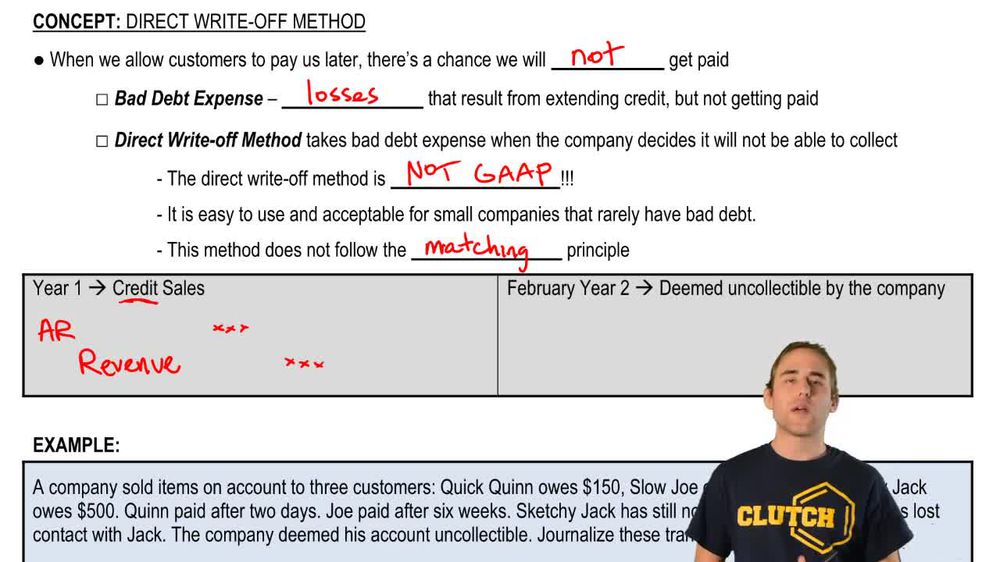

Bad Debt Expense

You can tap to flip the card.

👆

Bad Debt Expense

Loss recognized when amounts owed by customers from credit sales are determined to be uncollectible.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Net Accounts Receivable: Direct Write-off Method quiz #1

Net Accounts Receivable: Direct Write-off Method

25 Terms

Net Accounts Receivable: Direct Write-off Method

7. Receivables and Investments

10 problems

Topic

Net Accounts Receivable: Allowance for Doubtful Accounts

7. Receivables and Investments

9 problems

Topic

7. Receivables and Investments

10 topics

15 problems

Chapter

Guided course

05:59

Net Accounts Receivable: Direct Write-off Method

2056

views

63

rank

Terms in this set (15)

Hide definitions

Bad Debt Expense

Loss recognized when amounts owed by customers from credit sales are determined to be uncollectible.

Direct Write-off Method

Accounting approach where losses from uncollectible accounts are recorded only when specific accounts are deemed uncollectible.

Matching Principle

Accounting guideline requiring expenses to be recorded in the same period as the revenues they help generate.

Accounts Receivable

Amounts owed to a business by customers who purchased goods or services on credit.

Credit Sale

Transaction where goods or services are provided to a customer with payment to be received at a later date.

Revenue

Income earned from the sale of goods or services before any expenses are deducted.

Uncollectible Account

Receivable that is determined to be impossible to recover from the customer.

GAAP

Set of standardized accounting principles and guidelines used to ensure consistency and transparency in financial reporting.

Income Statement

Financial report showing a company’s revenues and expenses over a specific period, resulting in net income or loss.

Journal Entry

Formal accounting record documenting a business transaction’s financial impact on accounts.

Debit

Accounting entry that increases assets or expenses, or decreases liabilities or equity.

Credit

Accounting entry that increases liabilities or equity, or decreases assets or expenses.

Net Accounts Receivable

Total receivables expected to be collected, after deducting amounts estimated to be uncollectible.

Loss

Negative financial impact resulting from uncollected receivables or other unfavorable events.

Financial Statement

Formal record summarizing the financial activities and position of a business at a specific point in time.

BackBack

BackBack

05:59

05:59