Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Perpetual Inventory - FIFO, LIFO, and Average Cost definitions

You can tap to flip the card.

Perpetual Inventory System

You can tap to flip the card.

👆

Perpetual Inventory System

A method where inventory records are updated continuously after each purchase or sale, reflecting real-time inventory levels.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Related practice

Recommended videos

Perpetual Inventory - FIFO, LIFO, and Average Cost quiz

Perpetual Inventory - FIFO, LIFO, and Average Cost

15 Terms

Financial Statement Effects of Inventory Costing Methods

5. Inventory

10 problems

Topic

5. Inventory

7 topics

15 problems

Chapter

Guided course

10:12

Perpetual Inventory Average Cost

2061

views

34

rank

1

comments

Guided course

09:44

Perpetual Inventory FIFO

2702

views

49

rank

Guided course

07:15

Perpetual Inventory LIFO

1723

views

43

rank

Terms in this set (13)

Hide definitions

Perpetual Inventory System

A method where inventory records are updated continuously after each purchase or sale, reflecting real-time inventory levels.

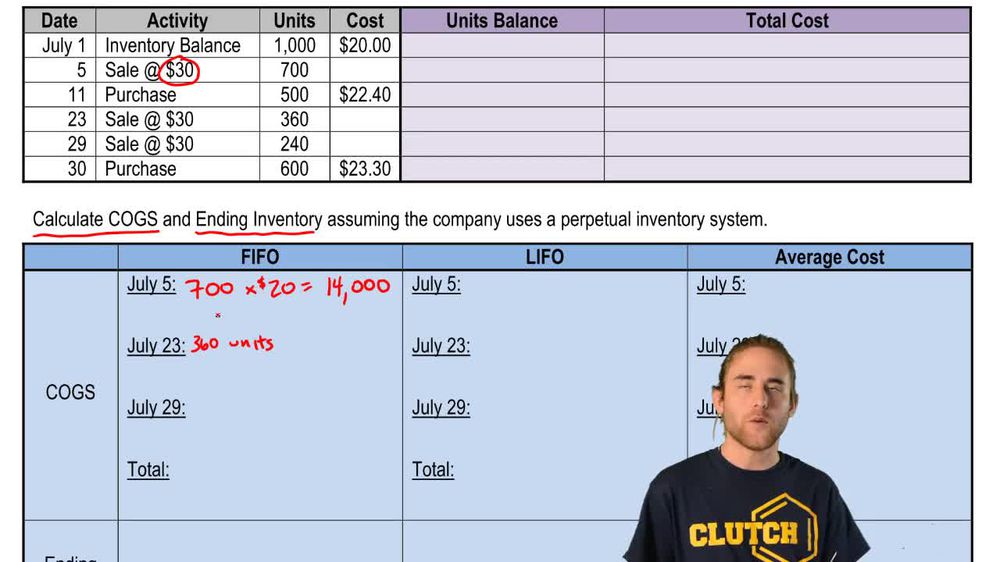

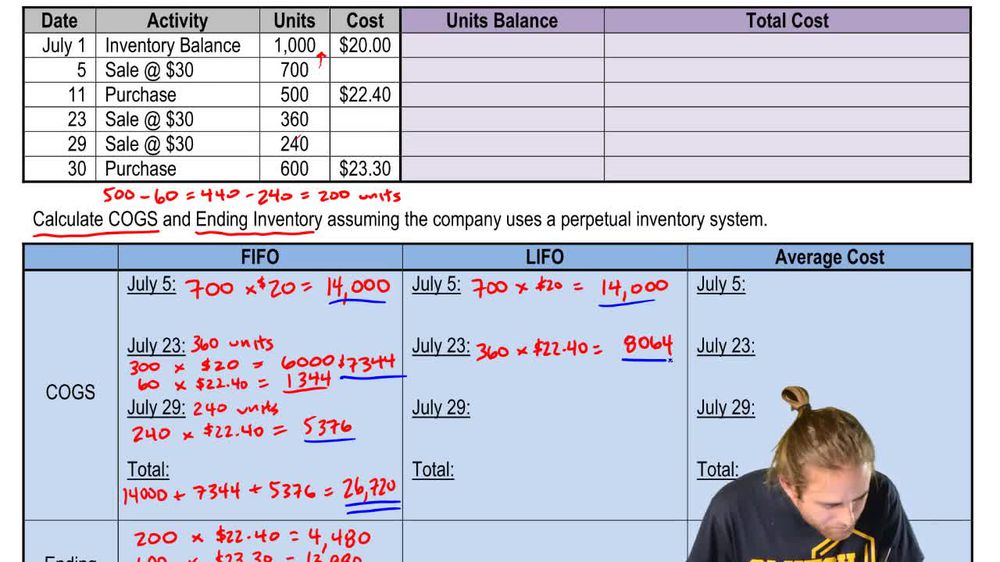

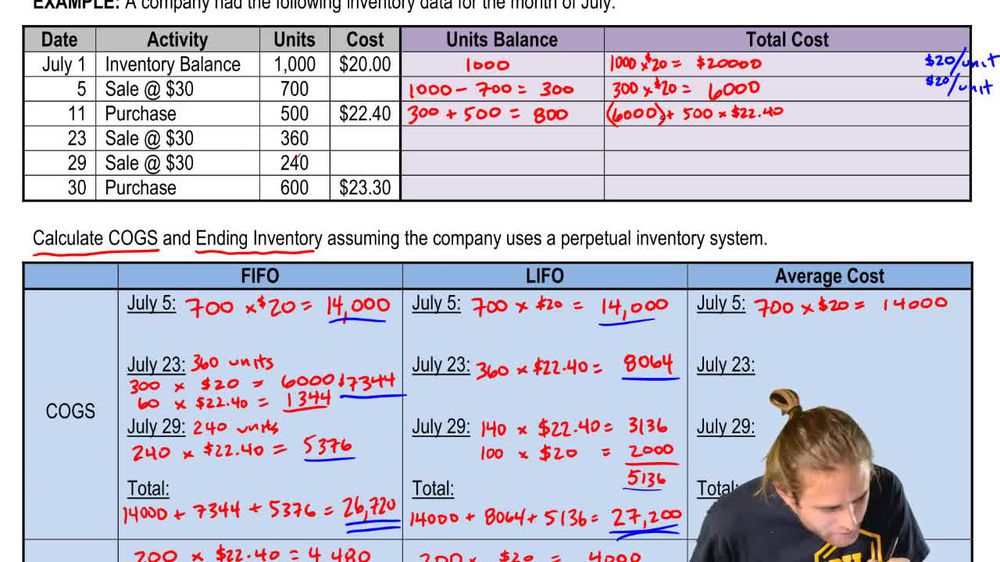

FIFO

A cost flow assumption where the oldest inventory units are considered sold first, impacting cost of goods sold with earlier purchase prices.

LIFO

A cost flow assumption where the newest inventory units are considered sold first, causing cost of goods sold to reflect recent purchase prices.

Average Cost Method

A technique that allocates cost of goods sold based on the average cost of all units available, recalculated after each transaction.

Moving Average

A recalculated average cost per unit in a perpetual system, updated after every inventory purchase or sale.

Cost Flow Assumption

An accounting approach that determines which inventory costs are assigned to cost of goods sold and ending inventory.

Cost of Goods Sold

The total cost assigned to inventory items that have been sold during a period, based on the chosen cost flow method.

Physical Flow of Goods

The actual movement of inventory items, which may differ from the accounting method used to assign costs.

Identical Inventory Items

Units of inventory that are indistinguishable from each other, such as cans of soda, requiring cost flow assumptions.

Cost per Unit

The result of dividing total inventory cost by the number of units available, used in the average cost method.

Inventory Record

A continuously updated log that tracks quantities and costs of inventory on hand in a perpetual system.

Purchase Price

The amount paid to acquire inventory units, which may vary between purchases and affect cost calculations.

Accounting Process

The systematic approach to recording, classifying, and summarizing inventory transactions using cost flow methods.

BackBack

BackBack

10:12

10:12