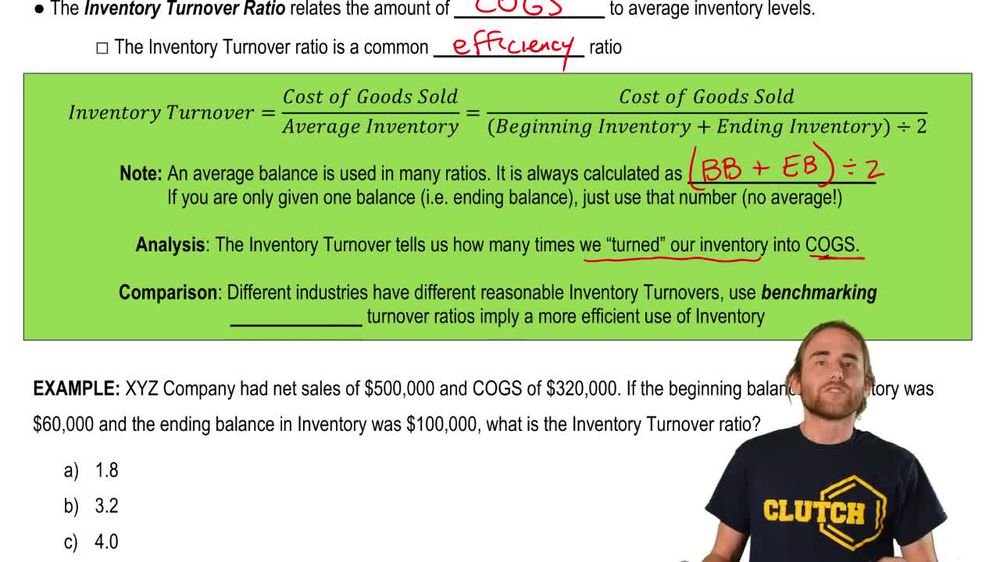

What does the inventory turnover ratio measure in a company?

The inventory turnover ratio measures how efficiently a company uses its inventory by comparing cost of goods sold (COGS) to average inventory levels.

How do you calculate average inventory for the inventory turnover ratio?

Average inventory is calculated by adding the beginning and ending inventory balances and dividing by two.

What is the formula for the inventory turnover ratio?

The formula is: Inventory Turnover Ratio = Cost of Goods Sold (COGS) / Average Inventory.

If a company has a beginning inventory of \$50,000 and an ending inventory of \$90,000, what is its average inventory?

The average inventory is (\(50,000 + \)90,000) / 2 = \$70,000.

Why is a higher inventory turnover ratio generally considered better?

A higher inventory turnover ratio indicates more efficient inventory management, meaning fewer resources are tied up in unsold goods.

How can benchmarking help when analyzing inventory turnover ratios?

Benchmarking allows a company to compare its inventory turnover ratio to competitors, helping assess if it is managing inventory more efficiently than others in the industry.

If a company has COGS of \$200,000 and average inventory of \$50,000, what is its inventory turnover ratio?

The inventory turnover ratio is \(200,000 / \)50,000 = 4.0.

What does an inventory turnover ratio of 4.0 indicate?

It indicates that the company turned its average inventory into cost of goods sold four times during the period.

Why should you use COGS instead of net sales when calculating inventory turnover?

COGS should be used because inventory and COGS both relate to the cost of goods, while net sales reflect the selling price, not the cost.

What could be a risk of maintaining too little inventory, even if turnover is high?

Maintaining too little inventory could result in stockouts, meaning the company may not be able to fulfill customer orders.

If only one inventory balance is provided, how should it be used in the inventory turnover calculation?

If only one inventory number is given, use it as the average inventory in the calculation.

What costs are associated with holding excess inventory?

Holding excess inventory increases storage and warehouse costs, tying up resources that could be used elsewhere.

How does the inventory turnover ratio relate to warehouse efficiency?

A higher inventory turnover ratio suggests that inventory is moving quickly through the warehouse, reducing storage costs and increasing efficiency.

What is the main purpose of analyzing the inventory turnover ratio?

The main purpose is to assess how effectively a company manages its inventory in relation to its sales and cost structure.

What does the inventory turnover ratio directly measure in financial accounting?

The inventory turnover ratio directly measures how efficiently a company uses its inventory by showing how many times average inventory is converted into cost of goods sold during a period.

What is the formula for computing a company's inventory turnover ratio?

The inventory turnover ratio is calculated as: Inventory Turnover Ratio = Cost of Goods Sold (COGS) ÷ Average Inventory.

What does inventory turnover measure in the context of financial accounting?

Inventory turnover measures the number of times a company's average inventory is sold and replaced over a period, indicating the efficiency of inventory management.

How is average inventory computed for the inventory turnover ratio?

Average inventory is computed by adding the beginning inventory balance and the ending inventory balance, then dividing by two: Average Inventory = (Beginning Inventory + Ending Inventory) ÷ 2.

Why is a higher inventory turnover ratio considered favorable for a company?

A higher inventory turnover ratio is considered favorable because it indicates more efficient inventory management, meaning fewer resources are tied up in unsold goods.

How can benchmarking inventory turnover ratios help a company?

Benchmarking inventory turnover ratios against competitors helps a company assess if it is managing its inventory more efficiently compared to others in the industry.

What is the significance of using cost of goods sold (COGS) instead of net sales in the inventory turnover ratio?

COGS is used in the inventory turnover ratio because it reflects the cost of inventory sold, which is directly related to inventory levels, whereas net sales represent revenue and do not measure inventory efficiency.

How do you find average inventory if only one inventory value is provided?

If only one inventory value is provided, that value is used as the average inventory for calculating the inventory turnover ratio.

What does an inventory turnover ratio of 4.0 indicate about a company's inventory management?

An inventory turnover ratio of 4.0 indicates that the company turned its average inventory into cost of goods sold four times during the period, suggesting efficient inventory management.

Back

Back

07:45

07:45