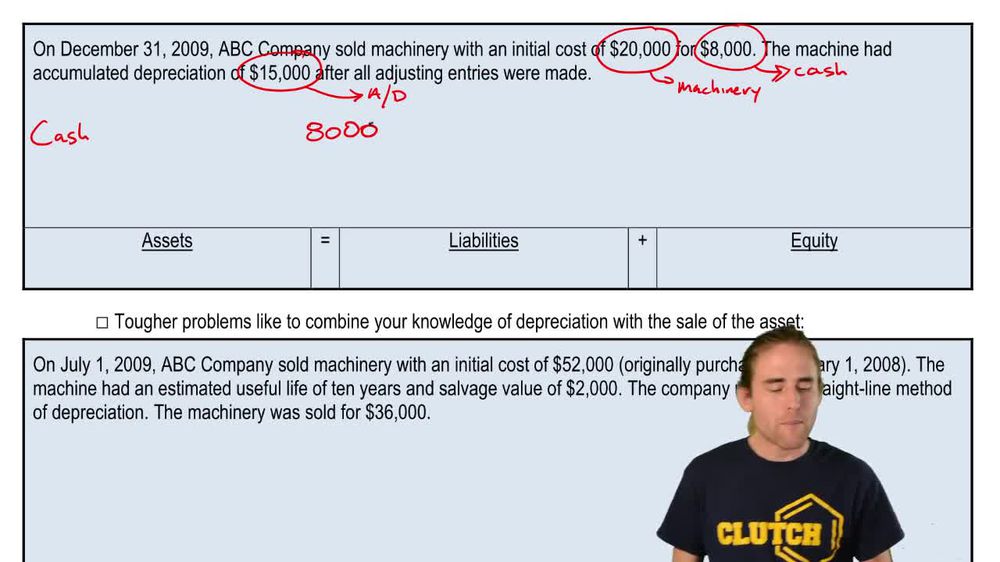

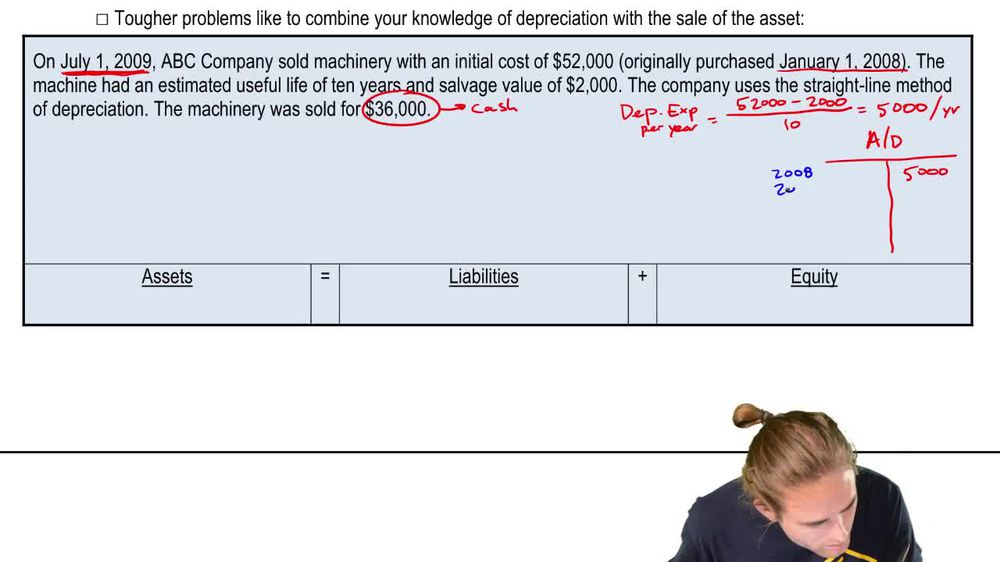

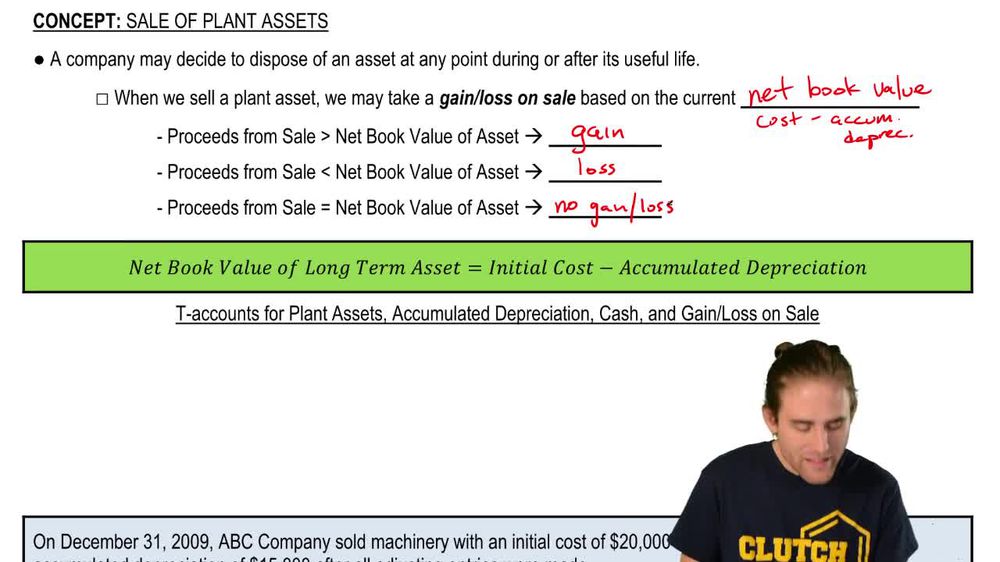

How do you determine whether a gain or loss is recognized when a plant asset is sold, and how is this reported on the income statement?

A gain is recognized if the cash proceeds from the sale exceed the asset's net book value (cost minus accumulated depreciation), while a loss is recognized if the proceeds are less than the net book value. If the proceeds equal the net book value, no gain or loss is recorded. Gains and losses from asset sales are reported in the 'other income' section of the income statement.

Back

Back

05:42

05:42