Straight Line Amortization of Bond Premium or Discount definitions Flashcards

Back

BackStraight Line Amortization of Bond Premium or Discount definitions

You can tap to flip the card.

Control buttons has been changed to "navigation" mode.

1/15

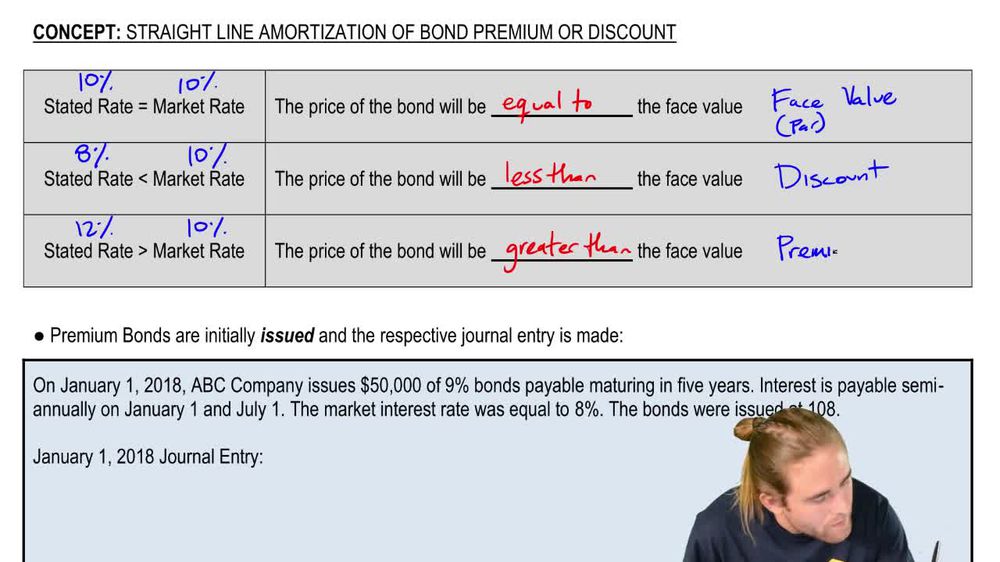

Face Value

Principal amount of a bond stated on its certificate, representing the sum repaid to bondholders at maturity.Stated Rate

Interest percentage printed on a bond, used to calculate periodic interest payments to bondholders.Market Rate

Prevailing interest percentage in the market for similar bonds, influencing bond pricing at issuance.Premium

Excess amount received over a bond’s face value when issued, occurring when the stated rate exceeds the market rate.Discount

Shortfall between cash received and a bond’s face value at issuance, resulting when the stated rate is below the market rate.Straight Line Amortization

Method allocating equal portions of bond premium or discount to each interest period over the bond’s life.Interest Expense

Total cost recognized each period for borrowing, combining cash interest and amortized premium or discount.Bonds Payable

Long-term liability account representing the total principal owed to bondholders at maturity.Premium on Bonds Payable

Liability account reflecting the amount received above face value, reduced over time through amortization.Discount on Bonds Payable

Contra-liability account showing the amount below face value, systematically reduced as interest expense increases.Carrying Value

Net amount of bonds payable after adjusting for unamortized premium or discount, representing the bond’s book value.Semiannual Interest Period

Six-month interval used for calculating and paying interest on bonds, doubling the number of periods per year.Issuance Entry

Initial journal record capturing cash received, liability created, and any premium or discount at bond issuance.Interest Payment

Periodic cash outflow to bondholders, calculated using the face value and stated rate, often adjusted for payment frequency.Plug

Balancing figure in a journal entry, ensuring debits and credits are equal, often used for interest expense in amortization.

04:07

04:07