Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Treasury Stock definitions

You can tap to flip the card.

Treasury Stock

You can tap to flip the card.

👆

Treasury Stock

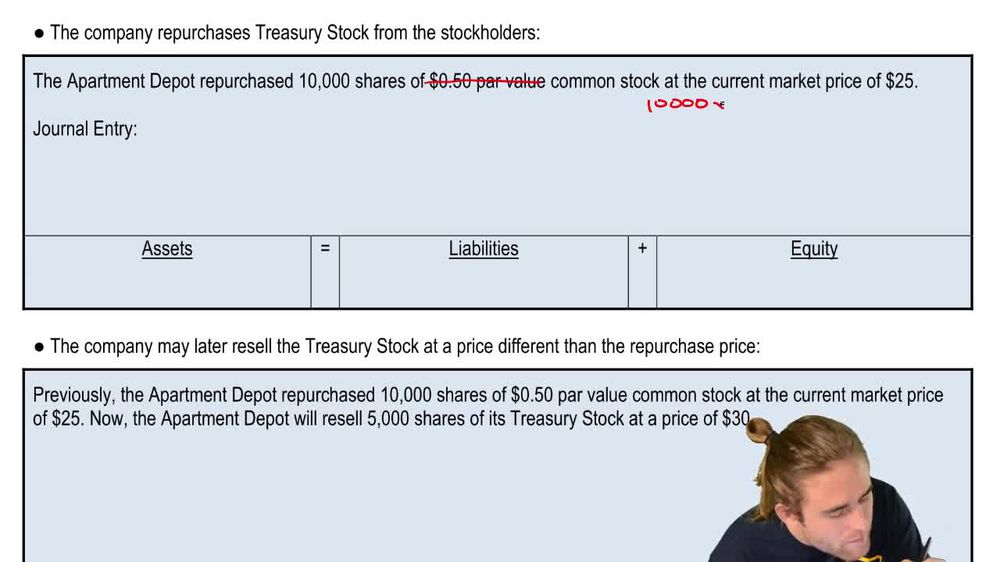

Shares previously issued and later repurchased by a company, held as a contra equity account with a debit balance, not entitled to dividends.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Related practice

Recommended videos

Treasury Stock quiz #1

Treasury Stock

14 Terms

Treasury Stock

12. Stockholders' Equity

10 problems

Topic

Dividends and Dividend Preferences

12. Stockholders' Equity

10 problems

Topic

12. Stockholders' Equity

12 topics

15 problems

Chapter

Guided course

02:53

Treasury Stock

981

views

15

rank

Guided course

04:43

Selling Treasury Stock from the Treasury

797

views

22

rank

Guided course

02:04

Repurchasing Stock into Treasury

865

views

19

rank

Terms in this set (13)

Hide definitions

Treasury Stock

Shares previously issued and later repurchased by a company, held as a contra equity account with a debit balance, not entitled to dividends.

Contra Equity Account

Equity classification that reduces total equity, typically carrying a debit balance, such as the account used for repurchased shares.

Debit Balance

Accounting state where the left side of an account exceeds the right, characteristic of accounts that reduce equity like repurchased shares.

Outstanding Shares

Portion of issued shares still held by external investors, eligible for dividends and not repurchased by the company.

Issued Shares

Total number of shares a company has distributed to investors, including those later repurchased as treasury stock.

Cost Method

Accounting approach for repurchased shares focusing on the amount paid to reacquire stock, ignoring par value in journal entries.

Par Value

Nominal value assigned to shares, not relevant when recording repurchased shares under the cost method.

Market Price

Current trading value of a company's shares, used as the basis for repurchase transactions involving treasury stock.

Dividends

Distributions of profits to shareholders, not paid on shares held as treasury stock.

Additional Paid-In Capital (APIC)

Equity account used to record differences between cash received and original cost when reselling repurchased shares.

Journal Entry

Formal accounting record of a transaction, such as repurchasing or reselling shares, affecting cash, equity, and related accounts.

Equity

Residual interest in a company's assets after liabilities, reduced by treasury stock transactions and increased when such shares are resold.

Cash

Asset account affected by treasury stock transactions, decreased when shares are repurchased and increased when resold.

BackBack

BackBack

02:53

02:53