Receivables are assets representing money owed to a company by others, typically customers.

How is an accounts receivable created in a journal entry?

Accounts receivable is created by debiting Accounts Receivable and crediting Revenue when a sale is made on account.

What distinguishes notes receivable from accounts receivable?

Notes receivable are formalized by written contracts and include interest, while accounts receivable are informal and usually do not include interest.

When does a company record a notes receivable instead of an accounts receivable?

A company records a notes receivable when a customer cannot pay on time and offers a formal note, often with interest, in place of the original accounts receivable.

What is the typical duration for accounts receivable and notes receivable?

Accounts receivable are usually due within 1 to 3 months, while notes receivable typically last from 3 months to a year or longer.

How is interest receivable different from notes receivable?

Interest receivable represents interest that has been earned but not yet received in cash, while notes receivable is the principal amount owed under a formal agreement.

What is a dividend receivable?

A dividend receivable is an asset representing dividends declared by another company that have been earned but not yet received.

What are trade receivables?

Trade receivables arise from normal business operations and include accounts receivable and some notes receivable from customers.

What are non-trade receivables?

Non-trade receivables do not arise from normal business operations and can include cash advances to employees or loans made from excess cash.

How does a company record the conversion of an accounts receivable to a notes receivable?

The company debits Notes Receivable and credits Accounts Receivable for the same amount.

Why are receivables considered assets?

Receivables are considered assets because they represent future economic benefits in the form of cash to be received.

What is the journal entry when a company earns interest but has not yet received the cash?

The company debits Interest Receivable and credits Interest Revenue.

Give an example of a non-trade receivable.

A cash advance to an employee is an example of a non-trade receivable.

What is the main difference between trade and non-trade receivables?

Trade receivables arise from core business activities, while non-trade receivables arise from activities outside the normal business operations.

How does a company record a sale on account?

The company debits Accounts Receivable and credits Revenue.

What happens to accounts receivable when it is replaced by a note receivable?

Accounts receivable is credited (decreased), and notes receivable is debited (increased) for the same amount.

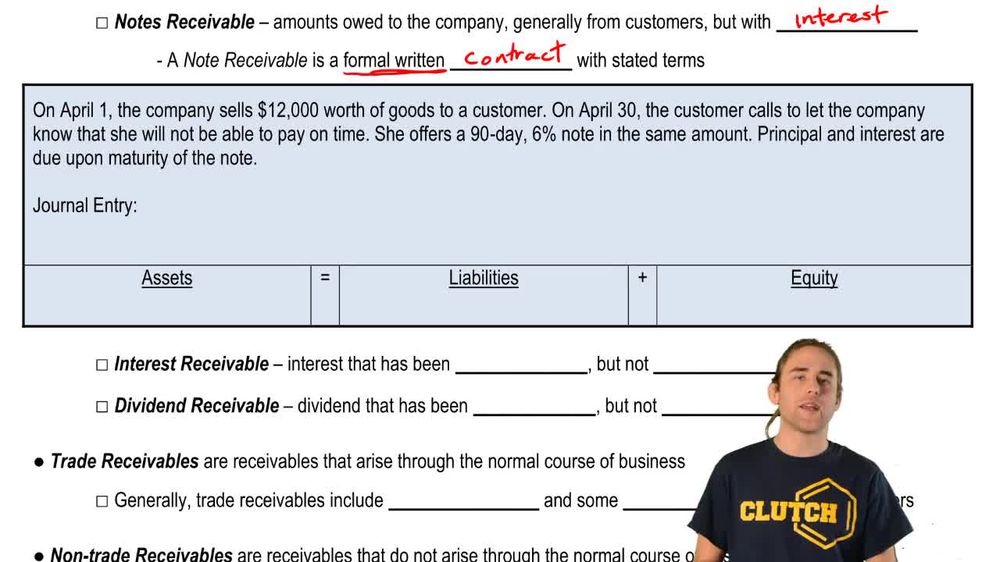

Why might a company issue a note receivable to a customer?

A company might issue a note receivable if a customer cannot pay their account receivable on time and agrees to a formal note with interest.

What is the principal amount in a note receivable?

The principal amount is the original sum of money loaned or owed, excluding interest.

How are receivables classified on the balance sheet?

Receivables are classified as assets on the balance sheet.

What is the purpose of a formal written contract in notes receivable?

A formal written contract in notes receivable specifies the terms, including the principal, interest rate, and maturity date.

Why are accounts receivable typically classified as current assets?

Accounts receivable are classified as current assets because they are expected to be collected within a short period, usually within one to three months.

What types of transactions should increase the accounts receivable balance?

Accounts receivable should be increased when a company sells goods or services on credit to customers.

Why are accounts receivable almost always considered current assets?

Accounts receivable are almost always considered current assets because they represent amounts owed by customers that are expected to be collected in the near term, typically within a few months.

What is the accounting effect when a company collects cash from accounts receivable?

When a company collects cash from accounts receivable, the accounts receivable balance decreases and cash increases by the same amount.

What does accounts receivable refer to in financial accounting?

Accounts receivable refers to amounts owed to a company by its customers for goods or services sold on credit.

What type of assets are created by selling goods and services on credit?

Assets created by selling goods and services on credit are called receivables, specifically accounts receivable.

What does the term 'accounts receivable (A/R)' mean?

Accounts receivable (A/R) means amounts owed to a company by customers for goods or services provided on credit.

What is the major problem associated with selling on credit?

The major problem with selling on credit is the risk that customers may not pay what they owe, leading to potential uncollectible accounts.

What type of account is accounts receivable?

Accounts receivable is an asset account.

What is a primary function of accounts receivable in a business?

A primary function of accounts receivable is to record amounts owed by customers for goods or services sold on credit.

At what amount are accounts receivable recorded in the accounting records?

Accounts receivable are recorded at the amount owed by customers for goods or services provided on credit.

Back

Back

08:00

08:00