Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Useful Information definitions

2 students found this helpful

You can tap to flip the card.

Relevance

You can tap to flip the card.

👆

Relevance

Quality of information that influences users' decisions by providing predictive and confirmatory value.

Track progress

Control buttons has been changed to "navigation" mode.

1/19

Related flashcards

Related practice

Recommended videos

Useful Information quiz #1

Useful Information

40 Terms

Useful Information quiz #2

Useful Information

11 Terms

Useful Information

1. Introduction to Accounting

10 problems

Topic

Fundamental Accounting Equation

1. Introduction to Accounting

10 problems

Topic

1. Introduction to Accounting

7 topics

15 problems

Chapter

Guided course

03:43

Enhancing Characteristics

5832

views

185

rank

Guided course

02:49

Four Underlying Assumptions

5120

views

147

rank

Guided course

03:16

Fundamental Qualitative Characteristics

8580

views

276

rank

1

comments

Terms in this set (19)

Hide definitions

Relevance

Quality of information that influences users' decisions by providing predictive and confirmatory value.

Predictive Value

Ability of information to help users forecast future outcomes or trends.

Confirmatory Value

Capacity of information to validate or refute previous predictions made by users.

Faithful Representation

Quality ensuring information is complete, unbiased, and free from significant errors.

Completeness

Extent to which all necessary and relevant details are included in the information provided.

Neutrality

Absence of bias in information, ensuring it is presented without favoring any side.

Material Error

Significant inaccuracy in information that could influence users' decisions, depending on company size.

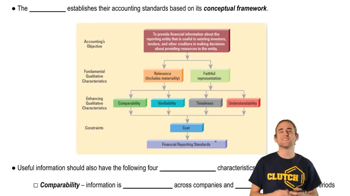

Comparability

Characteristic allowing information to be consistently evaluated across different companies and time periods.

Verifiability

Quality that enables independent confirmation of information accuracy through evidence or audit.

Timeliness

Availability of information to users early enough to impact their decision-making process.

Understandability

Clarity and transparency of information, making it easily comprehensible to users.

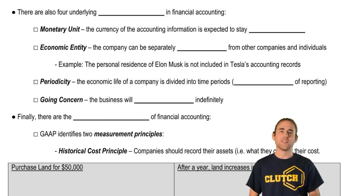

Monetary Unit Assumption

Presumption that financial records use a stable currency, disregarding inflation effects.

Economic Entity Assumption

Separation of business activities from those of owners or other entities in financial reporting.

Periodicity Assumption

Division of a company's economic life into consistent time intervals for reporting purposes.

Going Concern Assumption

Expectation that a business will continue operating indefinitely, not liquidating in the near future.

Historical Cost Principle

Requirement to record assets at their original purchase price, regardless of current market value.

Fair Value Principle

Mandate to report certain assets at their current market value, reflecting up-to-date worth.

Full Disclosure Principle

Obligation to reveal all information that could affect users' decisions, beyond just numerical data.

Cost Constraint

Limitation where the benefit of providing information must outweigh the cost of obtaining it.

BackBack

BackBack

03:43

03:43