Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Useful Information quiz #1

You can tap to flip the card.

What are the two fundamental qualitative characteristics of useful financial information according to the FASB conceptual framework?

You can tap to flip the card.

👆

What are the two fundamental qualitative characteristics of useful financial information according to the FASB conceptual framework?

The two fundamental qualitative characteristics are relevance and faithful representation.

Track progress

Control buttons has been changed to "navigation" mode.

1/40

Related flashcards

Related practice

Recommended videos

Useful Information definitions

Useful Information

19 Terms

Useful Information quiz #2

Useful Information

11 Terms

Useful Information

1. Introduction to Accounting

10 problems

Topic

Fundamental Accounting Equation

1. Introduction to Accounting

10 problems

Topic

1. Introduction to Accounting

7 topics

15 problems

Chapter

Guided course

03:43

Enhancing Characteristics

5832

views

185

rank

Guided course

02:49

Four Underlying Assumptions

5120

views

147

rank

Guided course

03:16

Fundamental Qualitative Characteristics

8580

views

276

rank

1

comments

Terms in this set (40)

Hide definitions

What are the two fundamental qualitative characteristics of useful financial information according to the FASB conceptual framework?

The two fundamental qualitative characteristics are relevance and faithful representation.

What does relevance mean in the context of financial information?

Relevance means the information can influence users' decisions by having predictive and/or confirmatory value.

What is predictive value in financial reporting?

Predictive value is the ability of information to help users forecast future outcomes.

What is confirmatory value in financial reporting?

Confirmatory value is the ability of information to help users confirm or correct prior predictions.

What does faithful representation require in financial information?

Faithful representation requires information to be complete, neutral, and free from material error.

What does completeness mean in the context of faithful representation?

Completeness means all relevant information is provided and nothing significant is omitted.

What does neutrality mean in financial reporting?

Neutrality means the information is unbiased and not presented to favor any particular outcome.

What does freedom from material error mean in financial information?

It means the information does not contain significant errors or omissions that could affect users' decisions.

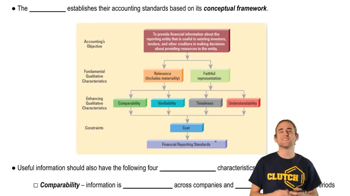

What are the four enhancing qualitative characteristics of useful financial information?

The four enhancing characteristics are comparability, verifiability, timeliness, and understandability.

What is comparability in financial reporting?

Comparability allows users to identify similarities and differences between different companies or periods.

What is verifiability in financial information?

Verifiability means that different knowledgeable and independent observers can reach consensus that information is faithfully represented.

What is timeliness in the context of financial information?

Timeliness means information is available to users in time to influence their decisions.

What is understandability in financial reporting?

Understandability means information is presented clearly and concisely so users can comprehend it.

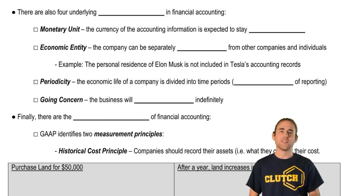

What is the monetary unit assumption in financial accounting?

The monetary unit assumption states that financial statements are reported in a stable currency, ignoring inflation.

What is the economic entity assumption?

The economic entity assumption requires that business transactions are kept separate from those of owners or other businesses.

What is the periodicity assumption in accounting?

The periodicity assumption means a company's economic life can be divided into artificial time periods for reporting.

What is the going concern assumption?

The going concern assumption presumes that a business will continue to operate indefinitely.

What is the historical cost principle?

The historical cost principle states that assets should be recorded at their original purchase cost.

What is the fair value principle?

The fair value principle states that assets and liabilities should be reported at their current market value.

What is the full disclosure principle?

The full disclosure principle requires that all information that could affect users' decisions be disclosed in financial statements.

What is the cost constraint in financial reporting?

The cost constraint means that the benefits of providing information should outweigh the costs of obtaining and presenting it.

How does materiality affect the reporting of errors in financial statements?

Materiality determines whether an error is significant enough to affect users' decisions and thus must be corrected or disclosed.

Why is comparability important for financial statement users?

Comparability allows users to evaluate financial information across different companies and time periods, aiding decision-making.

How does verifiability enhance the usefulness of financial information?

Verifiability increases users' confidence that information is accurate and can be confirmed by independent parties.

Why is timeliness crucial in financial reporting?

Timeliness ensures that information is available when needed for decision-making, increasing its relevance.

How does understandability benefit users of financial statements?

Understandability ensures that users can comprehend the information, making it more useful for decision-making.

Why is the monetary unit assumption necessary in accounting?

It provides a consistent measurement unit, allowing for meaningful aggregation and comparison of financial data.

How does the economic entity assumption affect financial reporting?

It ensures that only business transactions are included in the company's financial statements, not personal transactions of owners.

What is the purpose of the periodicity assumption?

It allows companies to report financial results at regular intervals, such as monthly, quarterly, or annually.

Why is the going concern assumption important for financial statements?

It justifies the use of historical cost and deferral of certain expenses, assuming the business will continue operating.

When is the historical cost principle typically used?

It is used for long-term assets like land and buildings, which are recorded at their original purchase price.

When is the fair value principle typically applied?

It is often applied to financial instruments like stocks and bonds, which are reported at current market value.

How does the full disclosure principle relate to faithful representation?

Full disclosure supports faithful representation by ensuring all relevant information is complete and available to users.

What is the role of the cost constraint in the full disclosure principle?

It limits disclosures to those whose benefits to users exceed the costs of providing the information.

How does materiality differ for large and small companies?

A small error may be material for a small company but immaterial for a large company, depending on its impact on decisions.

Why might a company not disclose every possible piece of information?

Because the cost of gathering and reporting some information may outweigh its usefulness to users.

What is the objective of the FASB's conceptual framework?

The objective is to provide useful financial information to users for decision-making.

How do enhancing qualitative characteristics improve financial information?

They make information more useful by increasing its comparability, verifiability, timeliness, and understandability.

What is an example of the economic entity assumption in practice?

A business owner's personal residence is not included in the company's financial statements.

How does the periodicity assumption support timeliness?

By dividing financial reporting into regular periods, it ensures timely information is available to users.

BackBack

BackBack

03:43

03:43