What is the primary focus of Financial Accounting 1B (AFE3692)?

To apply IFRS principles to complex financial transactions, prepare compliant financial statements, analyze financial instruments, understand segment reporting, revenue recognition, and evaluate credit risk and impairment.

What are the key characteristics of IFRS for SMEs?

Simplified recognition and measurement, reduced disclosure requirements, less frequent updates, and no earnings per share calculations for non-listed entities.

How should entities treat transactions not covered by IFRS for SMEs?

Refer to full IFRS standards, consider the IASB Framework, and develop accounting policies that provide relevant and reliable information.

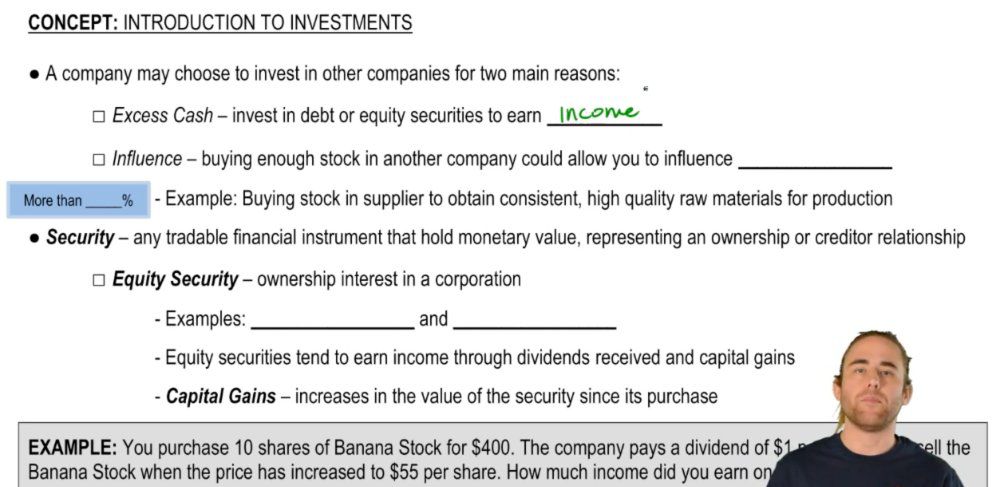

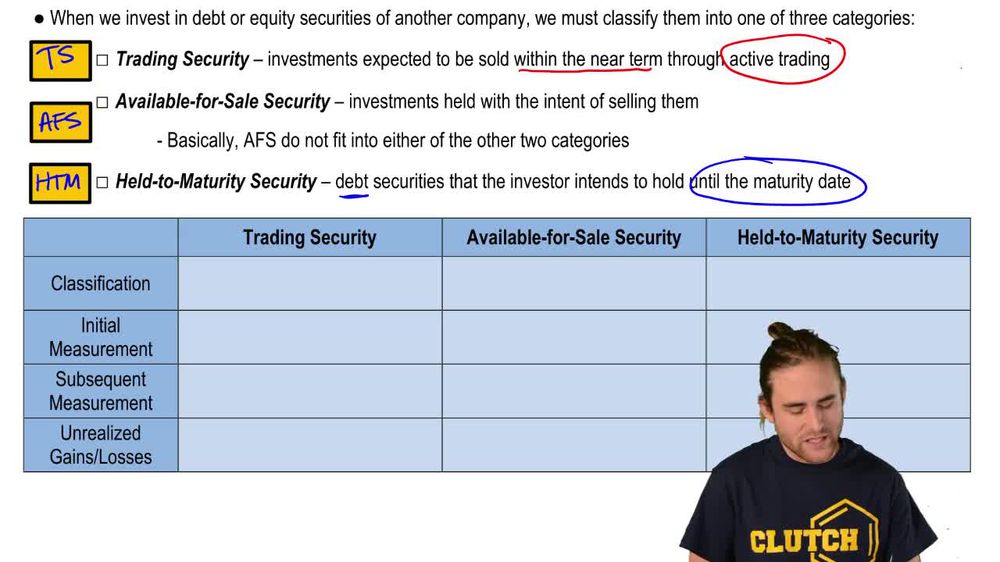

Under IFRS 9, what are the three classifications of financial assets?

Amortised Cost, Fair Value Through Other Comprehensive Income (FVOCI), and Fair Value Through Profit or Loss (FVTPL).

What conditions must be met for a financial asset to be classified at amortised cost under IFRS 9?

Held in a business model to collect contractual cash flows and cash flows are solely payments of principal and interest (SPPI).

How are financial assets initially measured under IFRS 9?

At fair value plus transaction costs for assets not classified as FVTPL.

What is the subsequent measurement method for financial assets classified at amortised cost?

Measured using the effective interest method; gains and losses recognized in profit or loss upon derecognition.

Describe the three-stage approach for impairment of financial assets under IFRS 9.

Stage 1: 12-month expected credit losses; Stage 2: Lifetime expected credit losses due to significant credit risk increase; Stage 3: Lifetime expected credit losses for credit-impaired assets.

When is reclassification of financial assets permitted under IFRS 9?

Only when there is a genuine change in the entity's business model for managing the financial assets.

What is the core principle of IFRS 15 Revenue from Contracts with Customers?

Recognise revenue to depict the transfer of promised goods or services to customers in an amount reflecting the consideration expected.

List the five steps of the IFRS 15 revenue recognition model.

1. Identify the contract; 2. Identify performance obligations; 3. Determine transaction price; 4. Allocate transaction price; 5. Recognise revenue when performance obligations are satisfied.

When is revenue recognised under IFRS 15?

When control of a good or service transfers to the customer, satisfying the performance obligation.

What does IFRS 16 require lessees to recognise on the balance sheet?

A right-of-use asset and a lease liability representing the present value of lease payments.

How is the initial lease liability calculated under IFRS 16?

Present value of lease payments using the implicit interest rate or incremental borrowing rate.

What are the criteria for identifying operating segments under IFRS 8?

Segments engage in business activities, results reviewed by the chief operating decision maker, and discrete financial information is available.

What quantitative thresholds determine reportable segments under IFRS 8?

Segments meeting 10% of total revenue, profit/loss, or assets thresholds, and collectively covering at least 75% of total external revenue.

How is the functional currency determined under IAS 21?

It is the currency of the primary economic environment in which the entity operates.

How are foreign currency transactions initially recorded under IAS 21?

At the spot exchange rate on the transaction date, translated into the functional currency.

What exchange rates are used for subsequent measurement of monetary and non-monetary items?

Monetary items use closing rate; non-monetary items at historical cost use transaction date rate; non-monetary items at fair value use rate at fair value date.

What is component depreciation under IAS 16?

Depreciating significant parts of an item of property, plant, and equipment separately when they have different useful lives.

How is annual depreciation calculated for components under IAS 16?

Using the straight-line method: Cost of each component divided by its useful life.

Back

Back

06:41

06:41