Back

BackFinancial Accounting Key Terms and Concepts

02:47

02:47

Terms in this set (29)

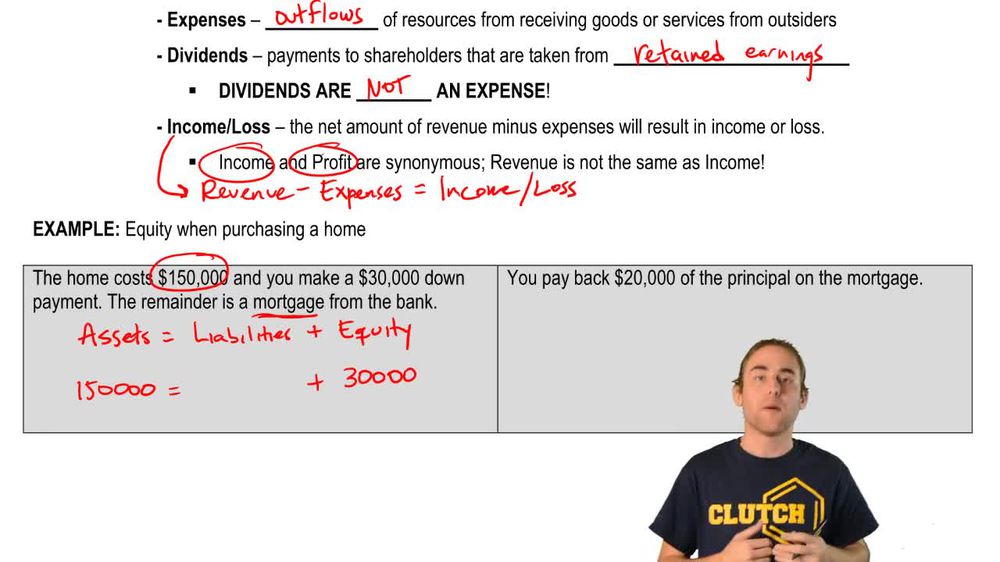

The foundation of double-entry accounting: \(\text{Assets} = \text{Liabilities} + \text{Equity}\). Ensures books stay balanced.

Resources a business owns or controls expected to provide current or future benefits.

A financial statement showing assets, liabilities, and equity at a specific point in time.

Requires treating the business separately from its owners to ensure clarity and legal separation.

A legal entity separate from owners; shareholders have limited liability.

Financial information should be disclosed only if benefits to users exceed the costs of providing it.

Allocating the cost of a long-term asset over its useful life to reflect usage and obsolescence.

Expenses must be recorded in the same period as the revenues they help generate.

Accounting aimed at external users, focusing on reporting financial information.

Rules and standards governing U.S. financial reporting to ensure consistency and transparency.

Reports revenues, expenses, and net income or loss for a period, showing profitability.

Expenses must be matched with the revenues they help generate; foundation of accrual accounting.

Assumes transactions can be expressed in a stable currency, ignoring inflation unless severe.

Revenues minus expenses when revenues exceed expenses.

A business owned by two or more people sharing profits, losses, and responsibilities without limited liability.

Shows how much of each sales dollar becomes profit: \(\frac{\text{Net Income}}{\text{Net Sales}}\).

Revenue is recorded when earned, not when cash is received.

Reports cash inflows and outflows from operating, investing, and financing activities.

Shows changes in owner’s capital including investments, withdrawals, and net income over a period.

A list of all accounts and their balances used to verify total debits equal total credits.

Cash received before providing goods or services; a liability until earned.

Expenses incurred but not yet paid or recorded, e.g., wages payable.

Revenues earned but not yet billed or received, e.g., services performed but not invoiced.

A hybrid business structure with limited liability and pass-through taxation.

A system where every transaction affects at least two accounts, keeping the accounting equation balanced.

A structured list of all accounts used by a company, organized by category.

Indicates the proportion of assets financed by debt: \(\frac{\text{Total Liabilities}}{\text{Total Assets}}\).

Asset cost minus accumulated depreciation.

Payments made in advance recorded as assets until used, then expensed.