Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

AE Model: Algebraic Approach definitions

You can tap to flip the card.

Aggregate Expenditures

You can tap to flip the card.

👆

Aggregate Expenditures

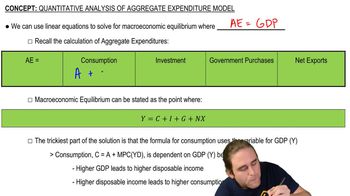

Total planned spending in an economy, including consumption, investment, government spending, and net exports.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Related practice

Recommended videos

AE Model: Algebraic Approach quiz

AE Model: Algebraic Approach

15 Terms

AE Model: Algebraic Approach

15. Deriving the Aggregate Expenditures Model

10 problems

Topic

Deriving the Multiplier Algebraically

15. Deriving the Aggregate Expenditures Model

10 problems

Topic

16. Deriving the Aggregate Expenditures Model

7 topics

13 problems

Chapter

Guided course

04:46

Aggregate Expenditures

1374

views

17

rank

Guided course

02:20

Algebraic Approach to the AE Model

1433

views

14

rank

Terms in this set (13)

Hide definitions

Aggregate Expenditures

Total planned spending in an economy, including consumption, investment, government spending, and net exports.

Macroeconomic Equilibrium

The point where total spending matches total output, ensuring no unplanned changes in inventories.

Linear Equation

A mathematical expression showing a straight-line relationship, used to model aggregate expenditures and GDP.

Consumption

Spending by households, calculated as a base amount plus a portion of income determined by the marginal propensity to consume.

Investment

Expenditures by businesses on capital goods, treated as a constant in the aggregate expenditures model.

Government Spending

Purchases of goods and services by the public sector, considered a fixed component in equilibrium calculations.

Net Exports

The value of exports minus imports, representing the international sector's contribution to aggregate expenditures.

GDP

The total market value of all final goods and services produced within a country, denoted as Y in equations.

Marginal Propensity to Consume

The fraction of additional income that households spend on consumption, influencing the slope of the consumption function.

Disposable Income

Income available to households after taxes, often approximated as total income in equilibrium calculations.

Base Consumption

The minimum level of household spending that occurs even when income is zero.

Equilibrium Equation

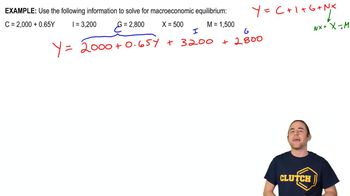

The algebraic statement Y = C + I + G + NX, used to solve for the output level where spending equals production.

Interdependence

The mutual relationship where changes in output affect consumption, which in turn influences total expenditures.

BackBack

BackBack

04:46

04:46