Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Tariffs on Imports quiz #1

You can tap to flip the card.

What is an example of a tariff?

You can tap to flip the card.

👆

What is an example of a tariff?

A government imposes a \$2 tax on every imported pair of shoes.

Track progress

Control buttons has been changed to "navigation" mode.

1/28

Related flashcards

Related practice

Recommended videos

Tariffs on Imports definitions

Tariffs on Imports

15 Terms

Tariffs on Imports

9. International Trade

10 problems

Topic

Import Quotas and VERs

9. International Trade

10 problems

Topic

9. International Trade

5 topics

15 problems

Chapter

Guided course

14:35

Tariffs on Imports

3104

views

48

rank

1

comments

Terms in this set (28)

Hide definitions

What is an example of a tariff?

A government imposes a \$2 tax on every imported pair of shoes.

Why does the federal government impose tariffs?

To generate tax revenue and to protect domestic industries from foreign competition.

What happens if a country lowers tariffs?

Lowering tariffs reduces the price of imports, increases imports, and benefits consumers through lower prices.

What is a protective tariff?

A protective tariff is a tax on imports designed to help domestic industries compete against lower-priced foreign goods.

Which type of trade barrier is a tax on imported goods?

A tariff is a trade barrier that is a tax on imported goods.

What effect do tariffs have on the price and quantity of imported goods?

Tariffs increase the price of imported goods and reduce the quantity of imports.

Which statements about tariffs and quotas are true?

Both tariffs and quotas restrict imports, but tariffs generate government revenue while quotas do not.

What is the primary function of protective tariffs?

To help domestic producers compete by making imported goods more expensive.

Which observation about tariffs is true?

Tariffs reduce consumer surplus and increase producer surplus for domestic producers.

What is a tax or fee that must be paid on goods imported from other countries called?

A tariff.

What are the effects of a tariff on imported goods and government revenue?

A tariff raises the price of imported goods, reducing imports and generating government revenue.

What is true about the effects of tariffs and trade restrictions on trade?

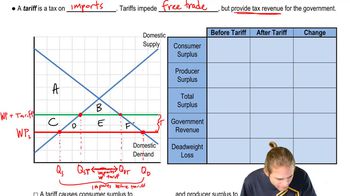

Tariffs and trade restrictions impede free trade and can create deadweight loss.

Which two groups are positively impacted when an import tariff is enacted? (Check all that apply.)

Domestic producers and the government (through increased revenue).

How do tariffs affect domestic producers and consumers?

Tariffs benefit domestic producers but harm consumers by raising prices.

Which scenario describes the operation of a tariff?

A country imposes a tax on imported steel, making it more expensive than domestic steel.

Which type of goods becomes more expensive as a result of tariffs?

Imported goods.

What is the long-term effect of tariffs and other trade barriers?

They reduce total economic surplus and can lead to deadweight loss.

Why would a government want to make imported goods more expensive?

To protect domestic industries from foreign competition.

Under what situation would the European Union impose tariffs on imports?

If foreign goods are being sold at lower prices than domestic goods, threatening local industries.

What is the most likely reason that nations raised tariffs on imports during the Great Depression?

To protect domestic industries and jobs during economic hardship.

Which statement best reflects the difference between tariffs and quotas?

Tariffs are taxes on imports that generate revenue, while quotas limit the quantity of imports without generating revenue.

Why do high tariff levels restrict international trade?

Because they increase the cost of imported goods, reducing the quantity imported.

What are laws calling for a tax on imported goods called?

Tariff laws.

When a country that imports a particular good imposes a tariff on that good, what happens?

The price of the imported good rises, imports decrease, and domestic producers supply more.

Introducing a tariff on vitamin Z would:

Increase the price of imported vitamin Z, reduce imports, and benefit domestic producers.

Raising an existing tariff on grapes from Argentina will:

Make imported grapes more expensive, reduce imports, and help domestic grape producers.

What is an example of a tariff?

A \$5 tax on every imported bicycle.

What are the four direct effects of a tariff?

Decrease in consumer surplus, increase in producer surplus, government revenue generation, and deadweight loss.

BackBack

BackBack

14:35

14:35