Back

BackMicroeconomics: Cost, Production, and Market Structures

05:02

05:02

Terms in this set (27)

User cost of capital is the opportunity cost of using capital, including depreciation and the foregone return from investing elsewhere.

Rental cost of capital is the actual cost paid to rent capital for a period, often used when firms do not own the capital.

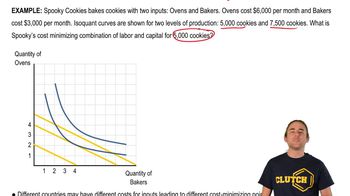

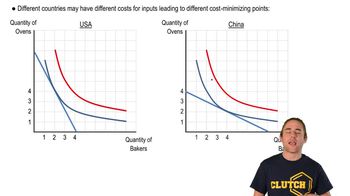

An isocost line shows all combinations of labor (L) and capital (K) that cost the same total amount, given by \(wL + rK = C\).

To minimize cost for a given output, a firm sets the ratio of marginal products equal to the ratio of input prices: \(\frac{MP_L}{MP_K} = \frac{w}{r}\).

The expansion path is the set of cost-minimizing input combinations as output increases, holding input prices constant.

The LRAC curve shows the lowest possible average cost of production when all inputs are variable.

The SRAC curve shows average cost when at least one input is fixed.

The LRAC curve is the lower envelope of all possible SRAC curves.

Economies of scale occur when increasing output lowers average cost (average cost decreases as output increases).

Diseconomies of scale occur when increasing output raises average cost (average cost increases as output increases).

Increasing returns to scale is a technological concept where output increases more than proportionally with inputs; economies of scale is a cost concept referring to declining average costs.

Cost output elasticity measures the percent change in cost from a 1% change in output. If less than 1, economies of scale exist; if greater than 1, diseconomies of scale exist.

Economies of scope exist if producing two goods together costs less than producing them separately.

Diseconomies of scope occur when joint production costs more than separate production.

Many small firms, homogeneous products, price takers, and free entry and exit.

Firms maximize profit by producing where \(MR = MC\). In perfect competition, \(MR = P\).

A firm produces if price covers average variable cost (\(P \geq AVC\)); otherwise, it shuts down.

The firm's short-run supply curve is the portion of the marginal cost curve above the average variable cost curve.

Constant cost (horizontal), increasing cost (upward sloping), and decreasing cost (downward sloping) industries.

Consumer surplus is the difference between what consumers are willing to pay and what they actually pay.

Producer surplus is the difference between the price received and the minimum price producers are willing to accept.

Deadweight loss is the loss of total surplus due to market distortions like taxes or price controls.

A price ceiling sets a legal maximum price, causing shortages and deadweight loss.

A price floor sets a legal minimum price, causing surpluses and deadweight loss.

Tax incidence depends on relative elasticities; the less elastic side bears more of the tax burden.

Taxes increase price for buyers, decrease price received by sellers, reduce quantity traded, and create deadweight loss.

Subsidies decrease price for buyers, increase price received by sellers, increase quantity traded, and may cause deadweight loss.