Back

BackCapital Budgeting: Cash Flows, Earnings, and Project Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Capital Budgeting

Introduction to Capital Budgeting

Capital budgeting is the process by which businesses evaluate potential major projects or investments. The goal is to determine whether these projects will generate sufficient returns to justify their costs.

Earnings are not actual cash flows; they are accounting measures and may not represent real profits.

Depreciation is a non-cash expense used for accounting purposes.

Net Working Capital (NWC) is the difference between current assets and current liabilities, including cash, inventory, receivables, and payables.

Pro-forma statement is based on hypothetical data to forecast project performance.

Capital Budgeting Process

The capital budgeting process involves identifying relevant cash flows, forecasting incremental earnings, and analyzing the impact of the project on the firm's financials.

Cash flow consequences of an investment must be considered.

Obsolescence refers to assets becoming outdated and no longer useful.

Forecasting Incremental Earnings

Incremental earnings are calculated to assess the additional profits generated by a project. Only incremental revenues and costs—those directly resulting from the project—should be included.

Incremental earnings before interest and taxes (EBIT):

Corporate tax expense must be accounted for in incremental earnings.

Capital expenditures (Capex) are investments in property, plant, and equipment and are not included in earnings calculations.

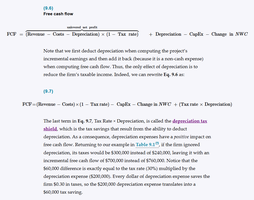

Forecasting Incremental Free Cash Flows (FCFs)

Free cash flow is a key metric in capital budgeting, representing the cash generated by a project after accounting for all expenses, taxes, and changes in working capital.

If NWC increases, it represents a decrease in cash flow for that year.

Depreciation is deducted to reduce taxable income, but added back to cash flow since it is a non-cash expense.

Free Cash Flow (FCF) Formula:

The depreciation tax shield is the tax savings from deducting depreciation.

Other Effects on Incremental FCFs

Several factors can affect incremental free cash flows:

Opportunity costs: The value of the next best alternative foregone.

Project externalities: Effects such as cannibalization, where a new product reduces sales of existing products.

Sunk costs: Costs that have already been incurred and cannot be recovered (e.g., past R&D, fixed overhead).

Project Analysis Techniques

To evaluate projects, managers use various analysis techniques:

Sensitivity analysis: Examines how changes in assumptions affect project outcomes.

Break-even analysis: Determines the point at which a project becomes profitable.

Scenario analysis: Considers different possible future states to assess project risk.

Real Options in Projects

Real options provide flexibility in project management and can add value to investments. Common real options include:

Delay: Waiting to invest until more information is available.

Expand: Increasing the scale of the project if successful.

Abandon: Terminating the project if it becomes unprofitable.

Treasury bills are used as a proxy for risk-free assets.

The option to invest in riskier ventures is generally more valuable.

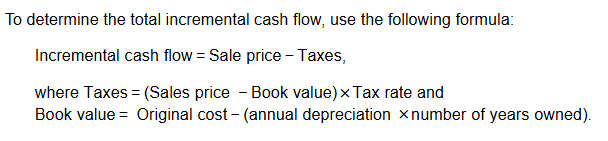

Incremental Cash Flow from Asset Sales

When selling assets, it is important to calculate the incremental cash flow, accounting for taxes on the sale.

Incremental cash flow formula:

Taxes are calculated as:

Book value is:

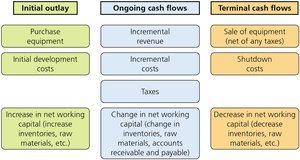

Summary Table: Types of Cash Flows in Capital Budgeting

Initial Outlay | Ongoing Cash Flows | Terminal Cash Flows |

|---|---|---|

Purchase equipment Initial development costs Increase in NWC (inventory, raw materials, etc.) | Incremental revenue Incremental costs Taxes Change in NWC (accounts receivable/payable, inventory) | Sale of equipment (net of taxes) Shutdown costs Decrease in NWC (inventory, raw materials, etc.) |

Learning Objectives Recap

After studying this chapter, you should be able to:

Identify types of cash flows needed in capital budgeting.

Forecast incremental earnings in pro-forma statements.

Convert forecasted earnings to free cash flows and compute net present value.

Recognize common pitfalls in identifying incremental free cash flows.

Assess sensitivity of project net present value to changes in assumptions.

Identify common options available to managers and understand their value.