Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Contingent Liabilities definitions

You can tap to flip the card.

Contingency

You can tap to flip the card.

👆

Contingency

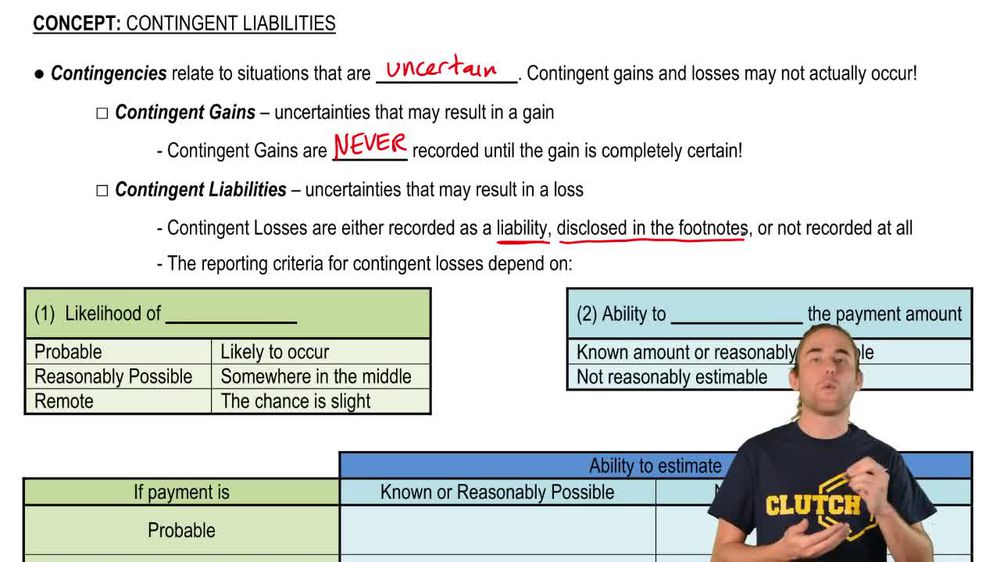

Uncertain situation in accounting that may result in a gain or loss, depending on the outcome of a future event.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Contingent Liabilities quiz #1

Contingent Liabilities

11 Terms

Contingent Liabilities

9. Current Liabilities

9 problems

Topic

Estimated Liabilities: Warranties

9. Current Liabilities

10 problems

Topic

9. Current Liabilities

7 topics

15 problems

Chapter

Guided course

07:27

Contingent Liabilities and Gains

906

views

21

rank

Terms in this set (15)

Hide definitions

Contingency

Uncertain situation in accounting that may result in a gain or loss, depending on the outcome of a future event.

Contingent Liability

Potential obligation arising from a past event, recognized if payment is probable and the amount can be estimated.

Contingent Gain

Possible benefit from an uncertain event, not recorded until it is realized due to accounting conservatism.

Accrual

Recording of an expense or liability in the financial statements before payment is made, based on probability and estimability.

Disclosure

Explanation provided in financial statement footnotes about uncertainties or risks not recognized as liabilities.

Footnotes

Sections in financial statements offering additional details about items such as contingencies and potential obligations.

Probability

Likelihood that a future event will require payment, categorized as probable, reasonably possible, or remote.

Estimability

Ability to reasonably determine the amount of a potential loss or obligation.

Probable

Classification indicating a high likelihood that a future event will result in a loss or payment.

Reasonably Possible

Classification for events with more than a remote but less than probable chance of resulting in a loss.

Remote

Classification for events with only a slight chance of resulting in a loss, requiring no action in financial statements.

Conservatism

Accounting principle favoring the recognition of potential losses over gains to avoid overstating financial health.

Legal Expense

Cost recognized when a probable and estimable loss from a legal case is accrued as a liability.

Financial Statements

Formal records, including balance sheet and footnotes, that present an entity’s financial position and disclosures.

Obligation

Potential or actual duty to pay or perform, often arising from past transactions or events.

BackBack

BackBack

07:27

07:27