Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Depreciation: Straight Line definitions

You can tap to flip the card.

Depreciation

You can tap to flip the card.

👆

Depreciation

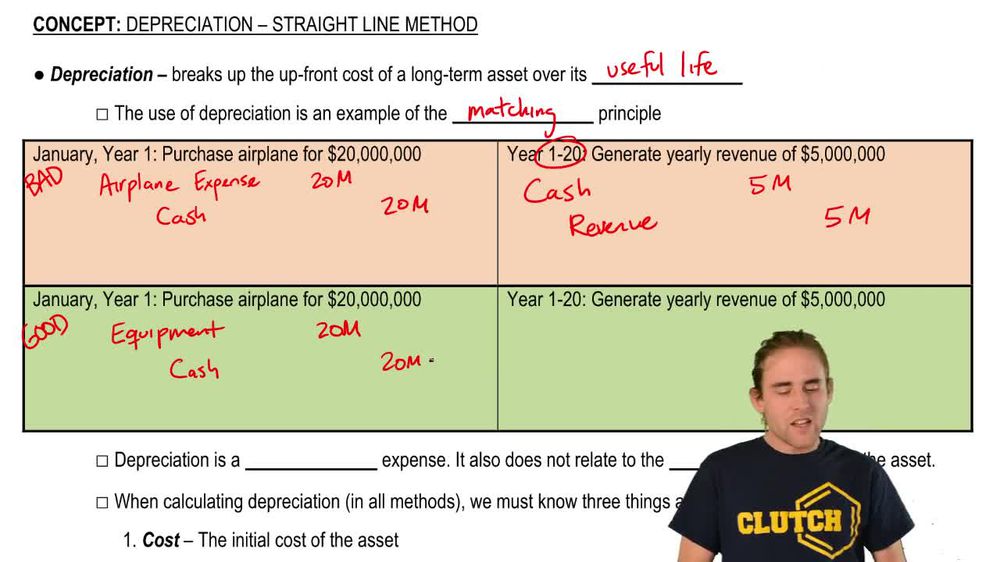

Allocation of a fixed asset's cost over its useful life to match expenses with related revenues, as required by GAAP.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Depreciation: Straight Line quiz #1

Depreciation: Straight Line

21 Terms

Depreciation: Straight Line

8. Long Lived Assets

9 problems

Topic

Depreciation: Declining Balance

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets

14 topics

15 problems

Chapter

Guided course

05:42

Straight Line Method Through Life of Asset

1090

views

27

rank

Guided course

11:55

Introduction to Depreciation

1779

views

25

rank

Guided course

06:30

Straight Line Depreciation

1463

views

32

rank

Terms in this set (15)

Hide definitions

Depreciation

Allocation of a fixed asset's cost over its useful life to match expenses with related revenues, as required by GAAP.

Straight-Line Method

Technique that spreads the depreciable base evenly over the asset's useful life, resulting in equal annual expense amounts.

Fixed Asset

Long-term tangible resource used in operations, such as equipment or vehicles, expected to provide benefits for multiple years.

Matching Principle

Accounting guideline requiring expenses to be recognized in the same period as the revenues they help generate.

GAAP

Set of standardized accounting rules in the U.S. that govern financial reporting and require systematic expense allocation.

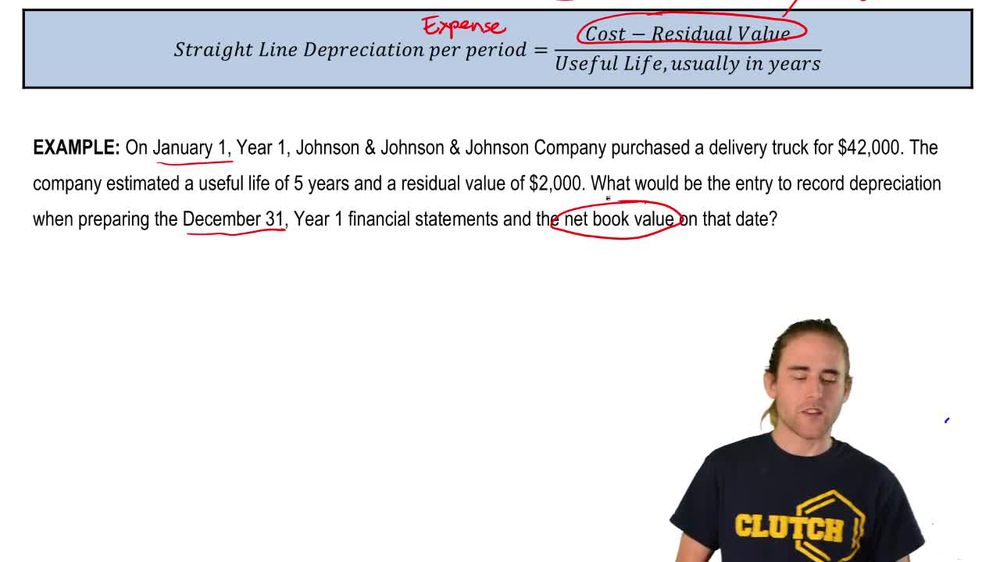

Depreciation Expense

Annual charge reflecting the portion of an asset's cost allocated to the current period under a chosen depreciation method.

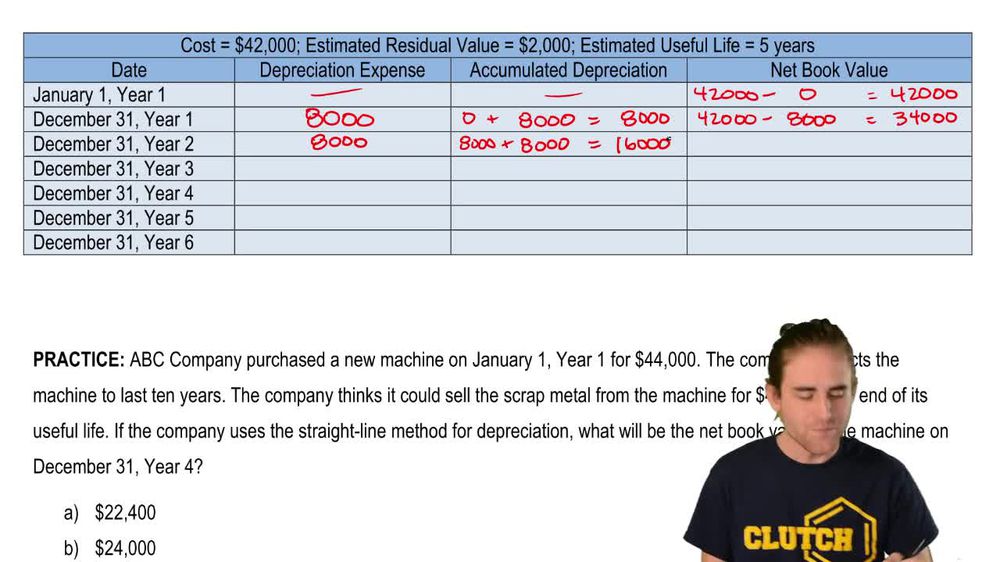

Accumulated Depreciation

Total depreciation recorded against an asset since acquisition, shown as a contra asset account on the balance sheet.

Contra Asset Account

Account that offsets a related asset account, reducing its book value on the balance sheet.

Net Book Value

Amount reported for an asset on the balance sheet, calculated as historical cost minus accumulated depreciation.

Residual Value

Estimated amount expected to be recovered at the end of an asset's useful life, also known as salvage value.

Useful Life

Estimated period over which an asset is expected to contribute to revenue generation for a business.

Depreciable Base

Difference between an asset's cost and its residual value, representing the total amount to be depreciated.

Historical Cost

Original purchase price of an asset, used as the basis for calculating depreciation and reported on the balance sheet.

Non-Cash Expense

Expense recognized in the accounting records that does not involve an actual cash outflow during the period.

Journal Entry

Formal accounting record documenting the debit to depreciation expense and credit to accumulated depreciation for each period.

BackBack

BackBack

05:42

05:42