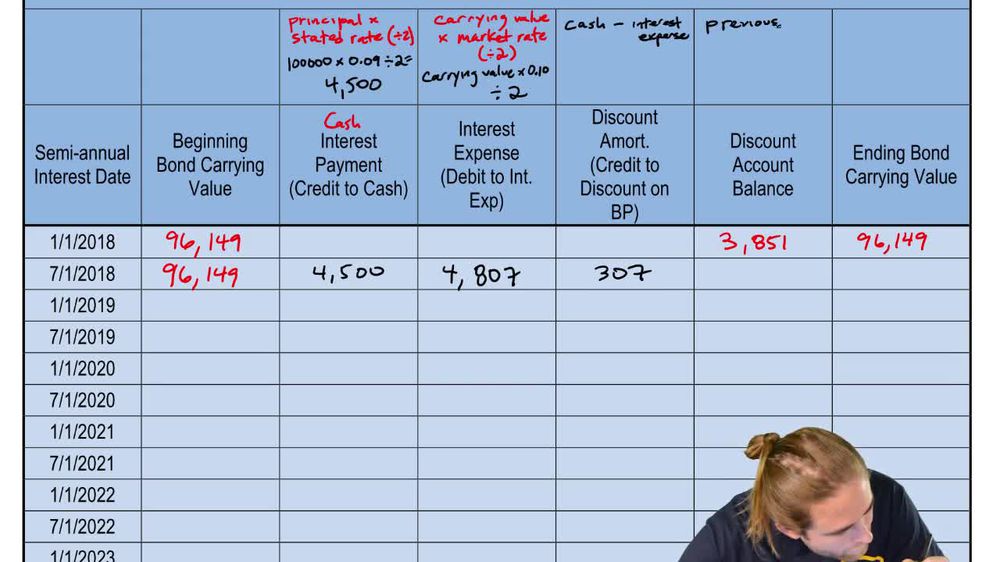

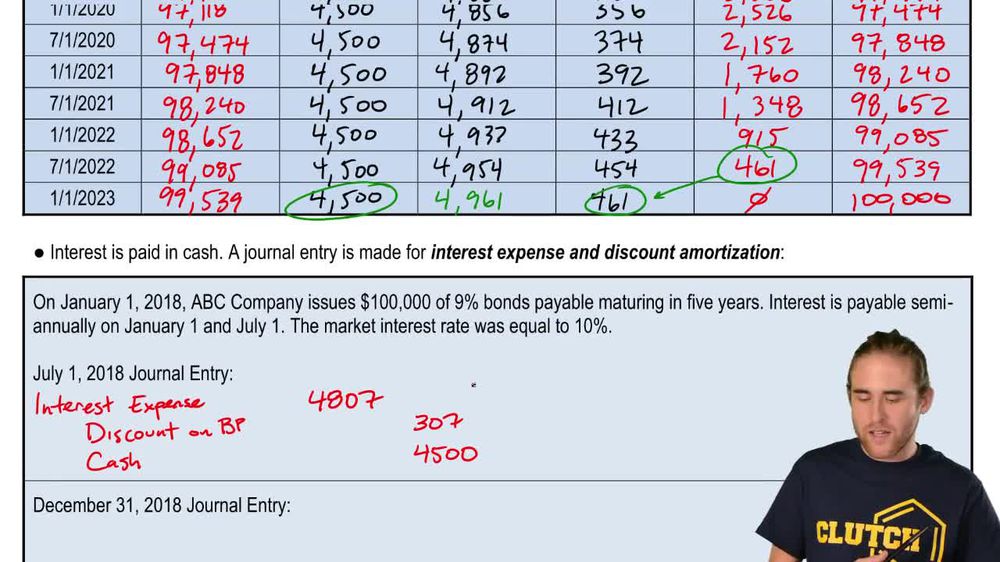

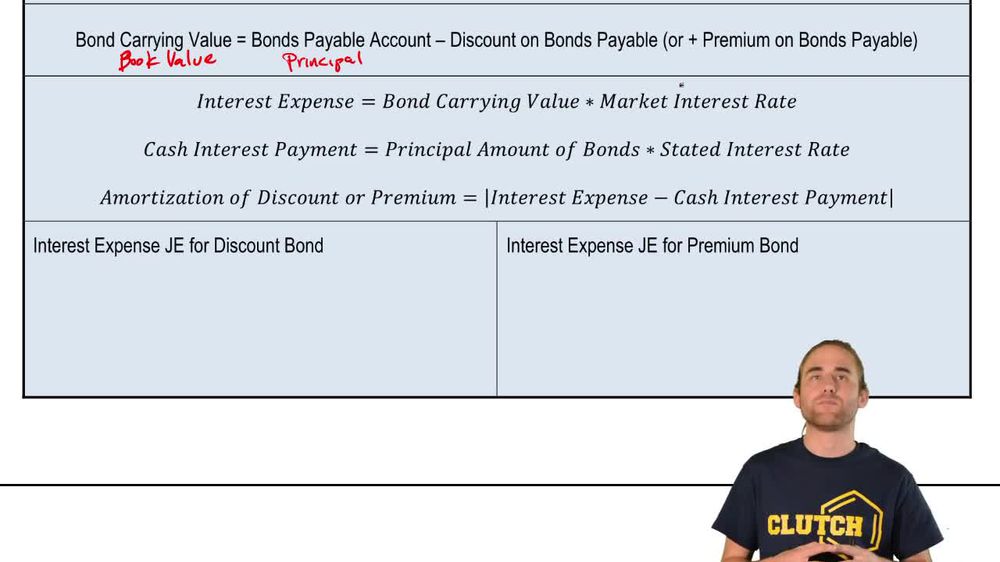

Guided course 04:24Important Equations for the Effective Interest Method of Bond Amortization908views10rank

BackBack

BackBack

04:24

04:24