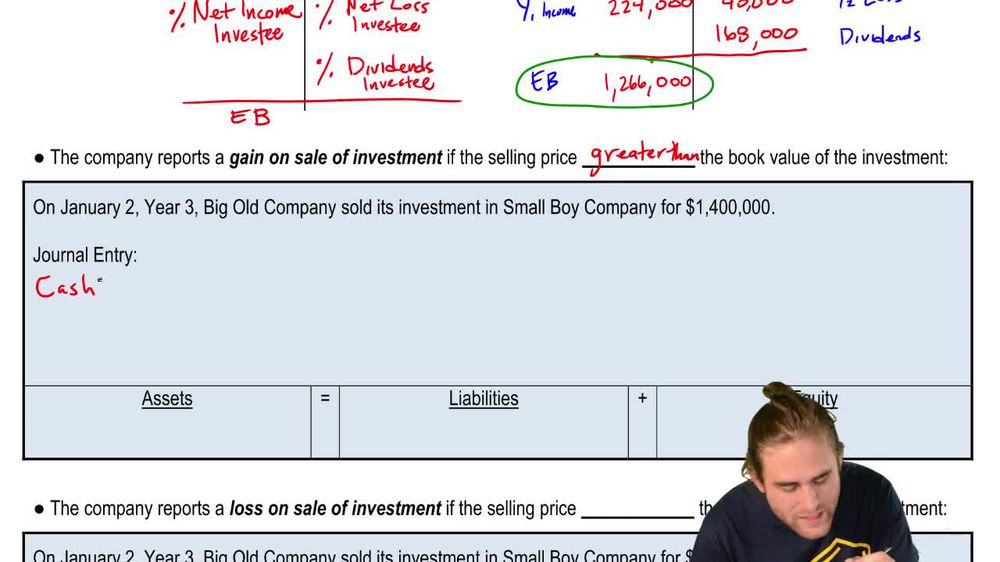

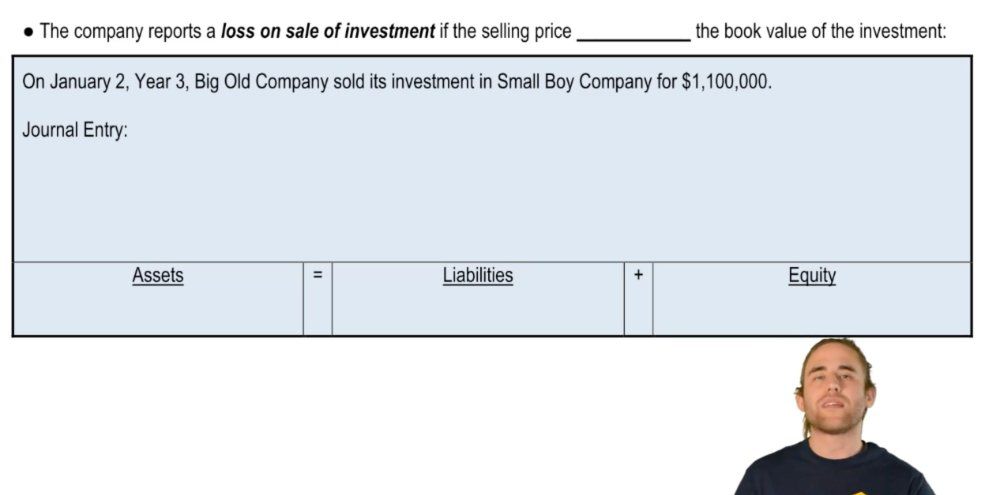

What is the equity method of accounting for investments, and when is it used?

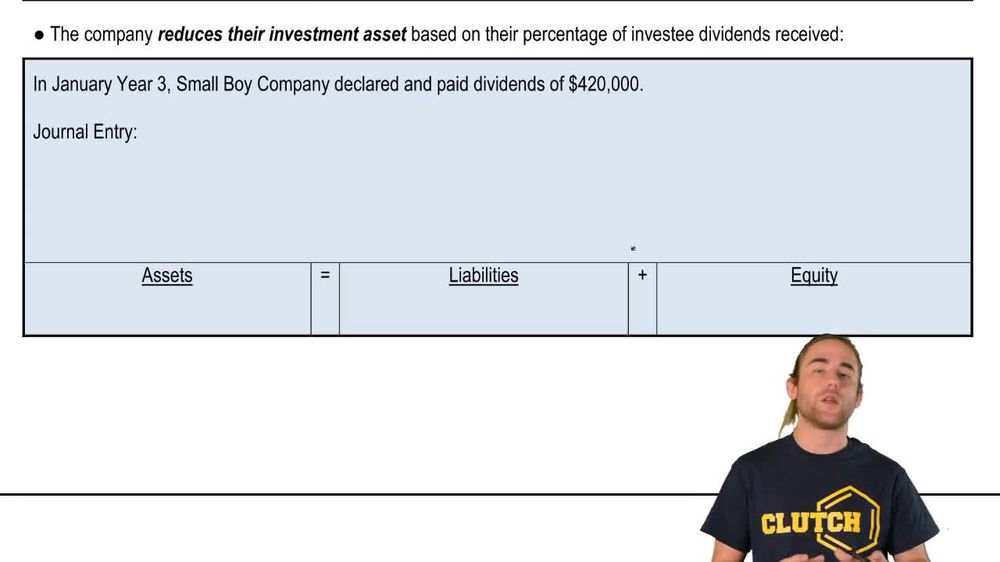

The equity method is used when an investor has significant influence, but not control, over an investee—typically owning between 20% and 50% of the company's voting stock. Under this method, the investment is initially recorded at cost, and the investor recognizes their proportional share of the investee's net income or loss, which adjusts the carrying value of the investment. Dividends received reduce the investment account rather than being recognized as income.

Back

Back

02:02

02:02