Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Inventory quiz

You can tap to flip the card.

Who sets the rules for GAAP in the United States?

You can tap to flip the card.

👆

Who sets the rules for GAAP in the United States?

The Financial Accounting Standards Board (FASB) sets the rules for GAAP in the United States.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Inventory definitions

GAAP vs. IFRS: Inventory

15 Terms

GAAP vs. IFRS: Inventory

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Fraud, Internal Controls, and Cash

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

03:23

GAAP vs. IFRS: Inventory

334

views

12

rank

Terms in this set (15)

Hide definitions

Who sets the rules for GAAP in the United States?

The Financial Accounting Standards Board (FASB) sets the rules for GAAP in the United States.

Which organization creates the International Financial Reporting Standards (IFRS)?

The International Accounting Standards Board (IASB) creates the IFRS.

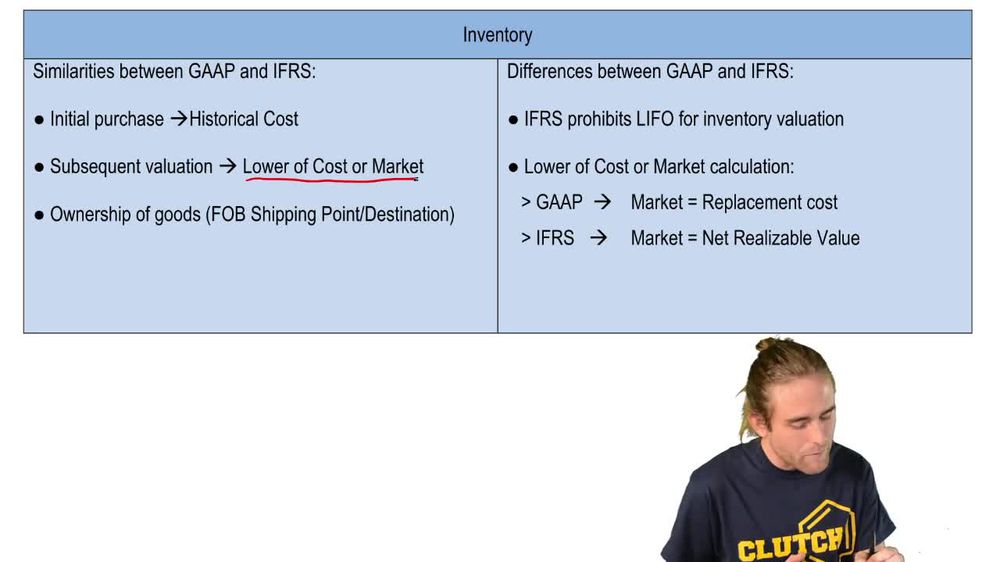

At what value is inventory initially recorded under both GAAP and IFRS?

Inventory is initially recorded at historical cost under both GAAP and IFRS.

What method do both GAAP and IFRS use for subsequent inventory valuation?

Both GAAP and IFRS use the lower of cost or market method for subsequent inventory valuation.

How does GAAP define 'market' in the lower of cost or market method?

GAAP defines 'market' as the replacement cost, which is the cost to replace the inventory today.

How does IFRS determine the value for the lower of cost or market calculation?

IFRS uses net realizable value, which is the estimated selling price minus any selling costs.

Which inventory costing method is prohibited under IFRS?

IFRS prohibits the use of the LIFO (Last-In, First-Out) inventory costing method.

Why does IFRS prohibit the use of LIFO for inventory?

IFRS prohibits LIFO because it does not reflect fair value and leaves old inventory costs on the books.

What is the main reason IFRS prefers methods other than LIFO?

IFRS prefers methods other than LIFO to ensure inventory values reflect current fair values.

Are the rules for ownership transfer of goods (e.g., FOB shipping point) the same under GAAP and IFRS?

Yes, the rules for ownership transfer of goods are the same under both GAAP and IFRS.

What does 'historical cost' mean in the context of inventory?

Historical cost means the amount paid to purchase the inventory initially.

What happens to inventory value if the market value decreases under both GAAP and IFRS?

If the market value decreases, both GAAP and IFRS require the inventory value to be written down.

What is the key difference in how GAAP and IFRS calculate the lower of cost or market?

GAAP uses replacement cost as market value, while IFRS uses net realizable value.

Why is understanding the differences between GAAP and IFRS important for inventory reporting?

Understanding these differences ensures accurate financial reporting and compliance with international standards.

Which standard is primarily used in the United States for inventory accounting?

GAAP is the standard primarily used in the United States for inventory accounting.

BackBack

BackBack

03:23

03:23