Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Receivables quiz

You can tap to flip the card.

Who sets the accounting standards for GAAP?

You can tap to flip the card.

👆

Who sets the accounting standards for GAAP?

The Financial Accounting Standards Board (FASB) sets the standards for GAAP in the US.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Receivables definitions

GAAP vs. IFRS: Receivables

14 Terms

GAAP vs. IFRS: Receivables

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Long Lived Assets

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

02:42

GAAP vs. IFRS: Receivables

356

views

3

rank

Terms in this set (15)

Hide definitions

Who sets the accounting standards for GAAP?

The Financial Accounting Standards Board (FASB) sets the standards for GAAP in the US.

Who is responsible for creating IFRS?

The International Accounting Standards Board (IASB) creates IFRS.

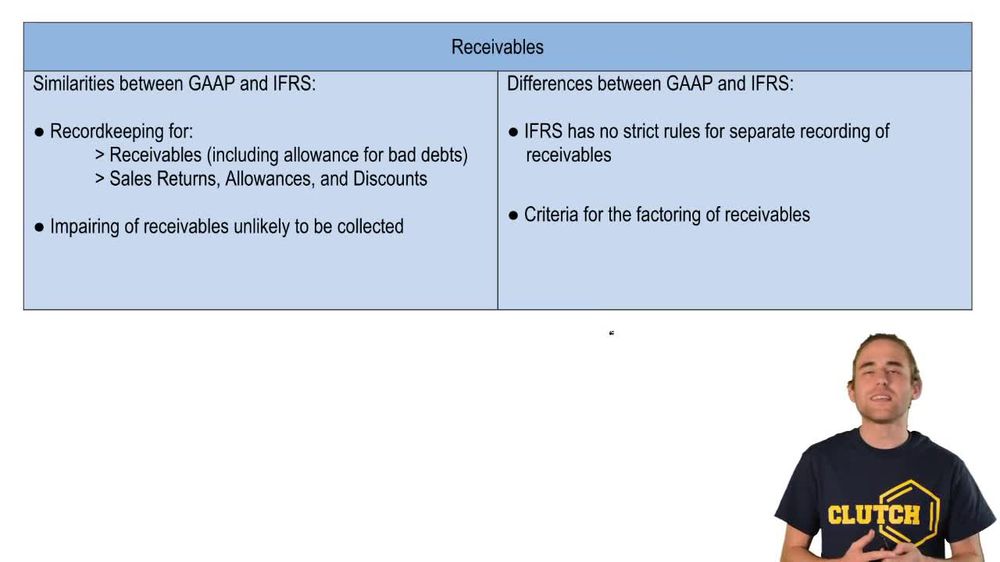

What is a key similarity between GAAP and IFRS regarding receivables?

Both GAAP and IFRS use similar record-keeping practices for receivables, including allowances for doubtful accounts.

How do GAAP and IFRS handle impairment of receivables?

Both GAAP and IFRS require impairment of receivables when collection is unlikely.

What is the main difference in account titles for receivables between GAAP and IFRS?

GAAP requires strict use of specific account titles for receivables, while IFRS is less strict but emphasizes transparency.

What is factoring of receivables?

Factoring is the process of selling receivables to another company to expedite cash collection.

Why might a company choose to factor its receivables?

A company may factor receivables to receive cash more quickly, especially if it is in a cash crunch.

Do GAAP and IFRS have the same rules for factoring receivables?

No, GAAP and IFRS have different criteria and rules for factoring receivables.

What is the main goal of accounting under both GAAP and IFRS?

The main goal is to be as transparent as possible in financial reporting.

Are sales returns, allowances, and discounts handled similarly under GAAP and IFRS?

Yes, these are handled in much the same way under both GAAP and IFRS.

What happens to receivables that are unlikely to be collected under both standards?

They are impaired, meaning their value is reduced on the financial statements.

Is it required under IFRS to use separate account titles for different types of receivables?

No, IFRS does not have strict rules for separate recording of receivables.

What is an allowance for doubtful accounts?

It is an estimate of receivables that may not be collected, recorded under both GAAP and IFRS.

Who takes on the risk of collection when receivables are factored?

The company that buys the receivables takes on the risk of collecting from customers.

Is the difference in factoring rules between GAAP and IFRS covered in detail in this course?

No, the specific criteria and rules for factoring under GAAP and IFRS are beyond the scope of this course.

BackBack

BackBack

02:42

02:42