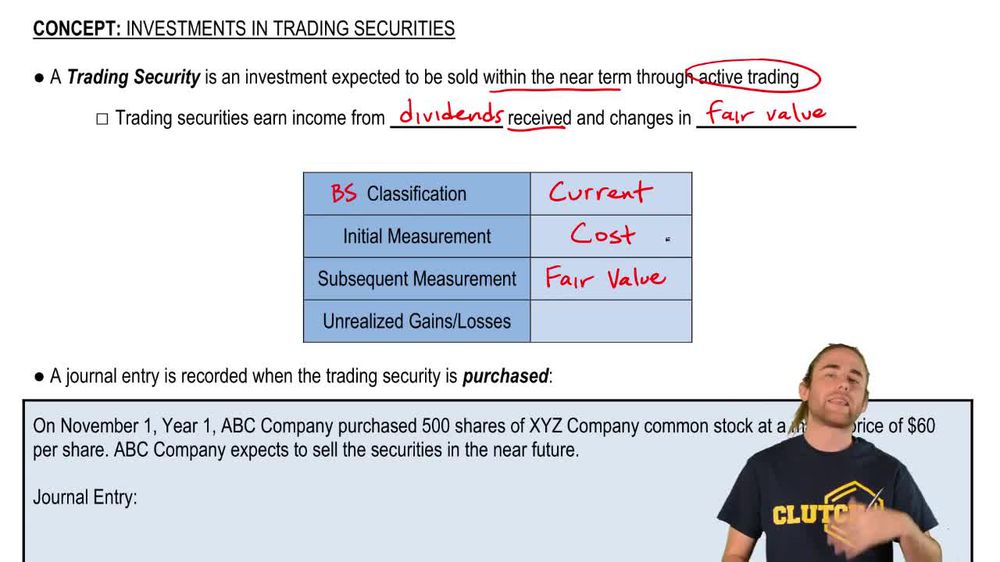

A trading security is a short-term investment expected to be sold in the near term through active trading.

How are trading securities initially measured on the balance sheet?

Trading securities are initially measured at cost when first purchased.

At what value are trading securities reported on subsequent balance sheets?

They are reported at fair value on subsequent balance sheets.

Where do unrealized gains or losses from trading securities appear in the financial statements?

Unrealized gains or losses appear on the income statement.

What is the journal entry to record the purchase of trading securities?

Debit investment in trading securities and credit cash for the purchase amount.

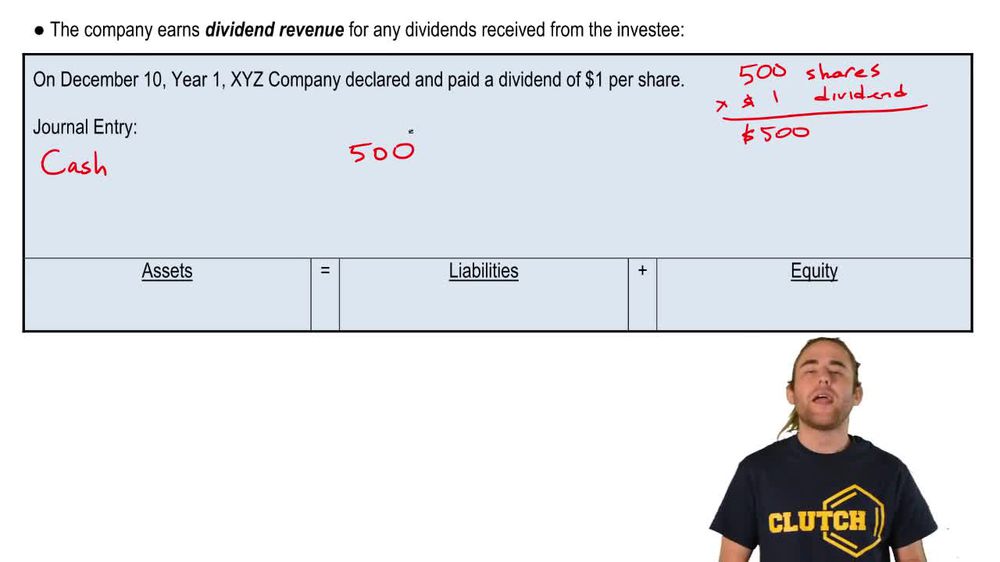

How is dividend revenue from trading securities recorded?

Debit cash and credit dividend revenue for the amount received.

Is dividend revenue from trading securities considered operating or non-operating income?

It is considered non-operating income and shown separately from operating income on the income statement.

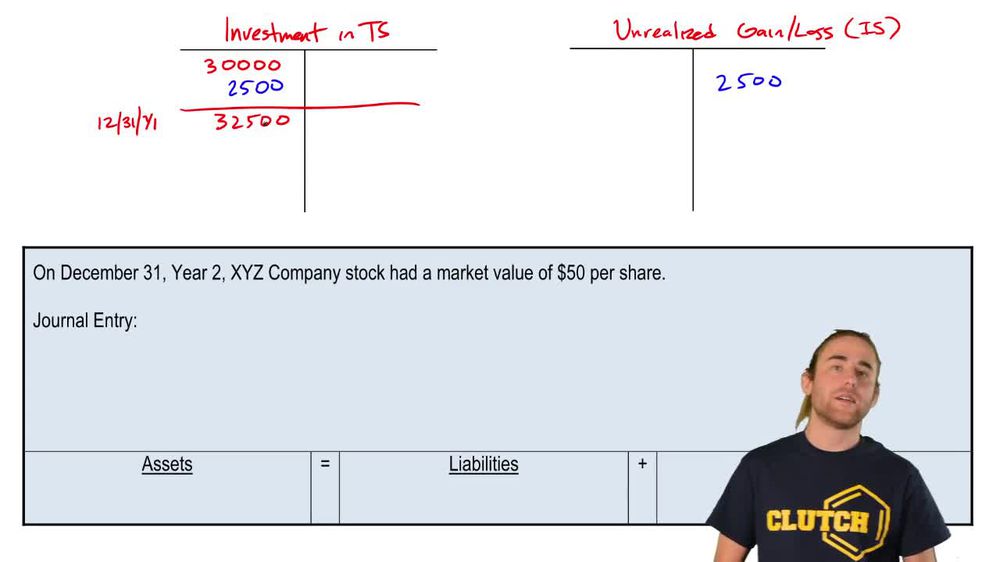

What triggers an unrealized gain or loss for trading securities?

A change in the fair value of the security at the reporting date triggers an unrealized gain or loss.

How do you adjust the investment account for an unrealized gain?

Debit the investment account and credit unrealized gain for the amount of the increase in fair value.

How do you adjust the investment account for an unrealized loss?

Credit the investment account and debit unrealized loss for the amount of the decrease in fair value.

When are realized gains or losses recognized for trading securities?

Realized gains or losses are recognized when the securities are sold.

How is a realized gain or loss calculated upon the sale of trading securities?

It is the difference between the selling price and the book value at the last revaluation.

What is the journal entry to record the sale of trading securities at a gain?

Debit cash for the sale amount, credit investment for its book value, and credit gain on sale for the difference.

How often should the fair value of trading securities be updated?

The fair value should be updated at each reporting date, such as at year-end.

What is the main difference in reporting unrealized gains/losses between trading securities and available-for-sale securities?

For trading securities, unrealized gains/losses go to the income statement, while for available-for-sale securities, they go to other comprehensive income.

Back

Back

06:22

06:22