Back

BackAccounting for Investments: Post-Purchase Valuation and Reporting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

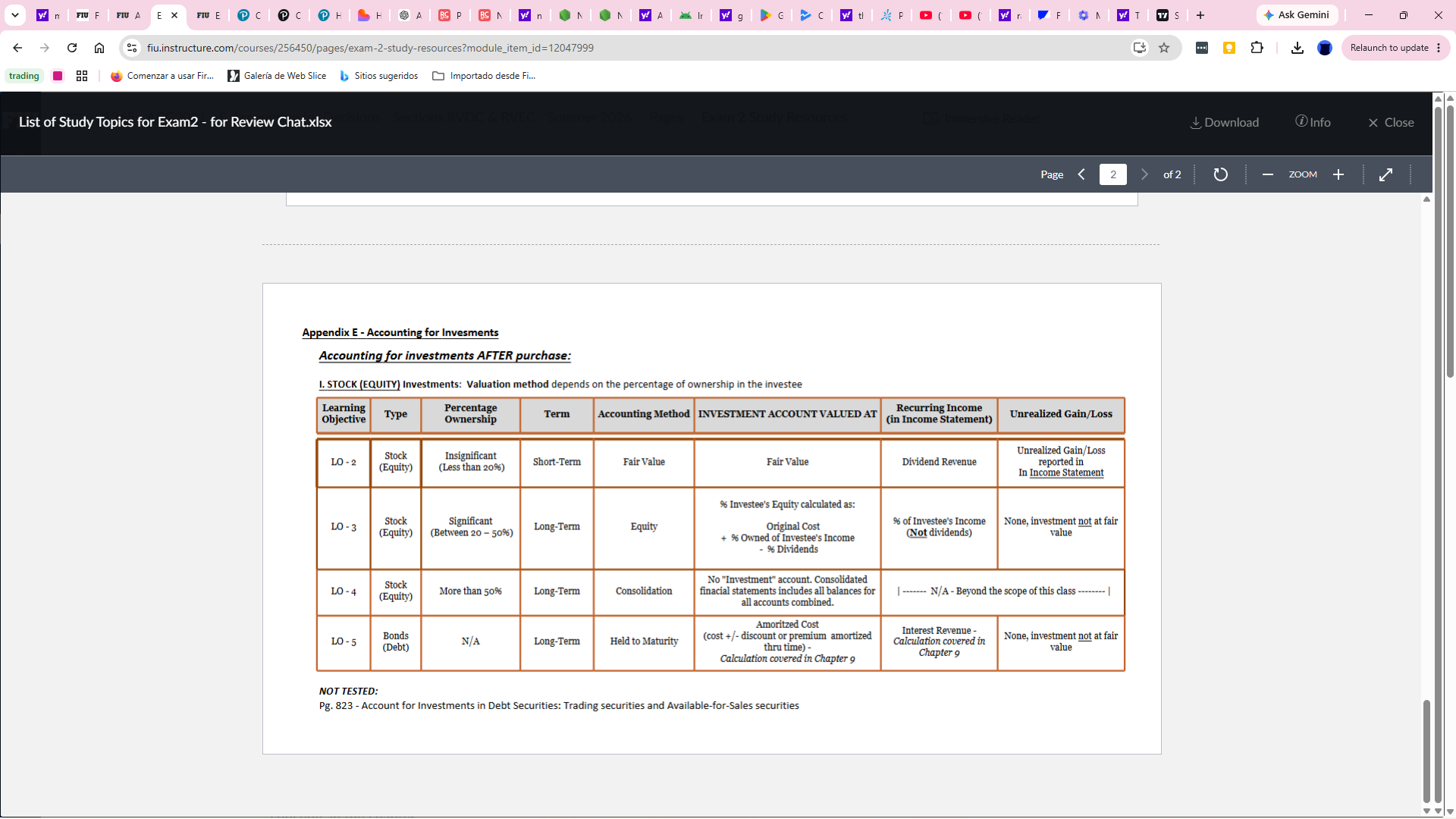

Appendix E – Accounting for Investments

Overview of Accounting for Investments After Purchase

This section explains the accounting treatment for investments after their acquisition, focusing on stock (equity) and bond (debt) investments. The valuation method and reporting depend on the percentage of ownership in the investee and the type of investment. Understanding these distinctions is crucial for accurate financial reporting and compliance with accounting standards.

Stock (Equity) Investments

Stock investments are classified and accounted for based on the investor's percentage of ownership in the investee. The main categories are insignificant influence, significant influence, and control.

Insignificant Influence (Less than 20% Ownership)

Type: Stock (Equity)

Term: Short-Term

Accounting Method: Fair Value

Investment Account Valued At: Fair Value

Recurring Income (in Income Statement): Dividend Revenue

Unrealized Gain/Loss: Reported in Income Statement

Example: An investor holds 10% of a company's shares and records changes in market value as unrealized gains or losses.

Significant Influence (20% to 50% Ownership)

Type: Stock (Equity)

Term: Long-Term

Accounting Method: Equity Method

Investment Account Valued At: Original Cost + % Owned of Investee's Income – % Dividends

Recurring Income (in Income Statement): % of Investee's Income (Not dividends)

Unrealized Gain/Loss: None, investment not at fair value

Example: An investor owns 30% of another company and recognizes their share of the investee's net income.

Control (More than 50% Ownership)

Type: Stock (Equity)

Term: Long-Term

Accounting Method: Consolidation

Investment Account Valued At: No separate investment account; consolidated financial statements include all balances for all accounts combined.

Recurring Income (in Income Statement): N/A – Beyond the scope of this class

Unrealized Gain/Loss: N/A – Beyond the scope of this class

Example: A parent company owns 80% of a subsidiary and prepares consolidated financial statements.

Bonds (Debt) Investments

Type: Bonds (Debt)

Term: Long-Term

Accounting Method: Held to Maturity

Investment Account Valued At: Amortized Cost (cost +/- discount or premium amortized over time)

Recurring Income (in Income Statement): Interest Revenue (Calculation covered in Chapter 9)

Unrealized Gain/Loss: None, investment not at fair value

Example: An investor holds a bond to maturity and recognizes interest revenue over the bond's life.

Summary Table: Accounting for Investments After Purchase

Type | Ownership % | Term | Accounting Method | Investment Account Valued At | Recurring Income | Unrealized Gain/Loss |

|---|---|---|---|---|---|---|

Stock (Equity) | Insignificant (<20%) | Short-Term | Fair Value | Fair Value | Dividend Revenue | Reported in Income Statement |

Stock (Equity) | Significant (20–50%) | Long-Term | Equity | Original Cost + % Owned of Investee's Income – % Dividends | % of Investee's Income (Not dividends) | None, not at fair value |

Stock (Equity) | Control (>50%) | Long-Term | Consolidation | All balances combined in consolidated statements | N/A | N/A |

Bonds (Debt) | N/A | Long-Term | Held to Maturity | Amortized Cost | Interest Revenue | None, not at fair value |

Key Formulas

Equity Method Investment Value:

Amortized Cost for Bonds:

Additional Notes

Trading securities and available-for-sale securities are not tested in this section (see Pg. 823 for more details).

Consolidation accounting and advanced topics are beyond the scope of this class.