Back

BackAdjusting Accounts for Financial Statements: Accrual Accounting and Adjusting Entries

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Adjusting Accounts for Financial Statements

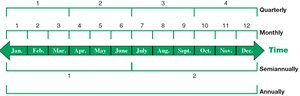

The Accounting Period

Accounting divides time into distinct periods to measure and report financial performance. These periods can be monthly, quarterly, semiannually, or annually, depending on the needs of the business and regulatory requirements. This periodic reporting is essential for providing timely and relevant financial information to stakeholders.

Monthly: 12 periods per year

Quarterly: 4 periods per year

Semiannually: 2 periods per year

Annually: 1 period per year

Accrual Accounting vs. Cash Basis Accounting

Accrual accounting records revenues when earned and expenses when incurred, regardless of when cash is received or paid. In contrast, cash basis accounting records revenues and expenses only when cash changes hands. Accrual accounting provides a more accurate picture of financial performance by matching revenues and expenses to the periods in which they occur.

Accrual Basis: Recognizes revenue when goods/services are delivered and expenses when incurred.

Cash Basis: Recognizes revenue when cash is received and expenses when cash is paid.

Example: If a company pays $2,400 for a 24-month insurance policy, accrual accounting spreads the expense over the coverage period, while cash basis records the entire expense when paid.

Revenue and Expense Recognition Principles

The revenue recognition principle requires revenue to be recorded when earned, at the amount expected to be received. The expense recognition (matching) principle requires expenses to be recorded in the same period as the related revenues, ensuring accurate measurement of profit.

Revenue Recognition: Record revenue when goods/services are provided.

Expense Recognition: Record expenses in the same period as the related revenue.

Framework for Adjustments

Types of Adjustments

Adjustments are necessary for transactions that span multiple periods. There are four main types:

Deferral of expenses (prepaid expenses)

Deferral of revenues (unearned revenues)

Accrued expenses

Accrued revenues

Adjustments follow a three-step process:

Determine the current account balance.

Determine what the balance should be.

Record an adjusting entry to correct the balance.

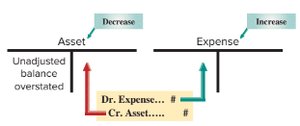

Adjusting Entries for Deferral of Expenses

Prepaid (Deferred) Expenses

Prepaid expenses are assets paid in advance for future benefits. As the benefits are used, the asset is reduced and an expense is recognized.

Examples: Prepaid Insurance, Prepaid Rent, Supplies

Example: FastForward paid $2,400 for a 24-month insurance policy. Each month, $100 is recognized as insurance expense, reducing prepaid insurance.

Formula: $2,400 / 24 months = $100 per month

Adjusting for Supplies

Supplies purchased are recorded as assets. At period end, a physical count determines the unused supplies. The difference is recorded as supplies expense.

Example: Purchased $9,720 of supplies; unused supplies at period end are $8,670. Supplies expense is $1,050.

Depreciation of Long-Lived Assets

Depreciation allocates the cost of plant assets over their useful lives. The straight-line method spreads the cost evenly.

Formula:

Example: Equipment cost \frac{18,000}{60} = 300$

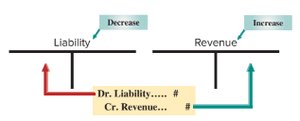

Adjusting Entries for Deferral of Revenues

Unearned Revenue

Unearned revenue is cash received before services are provided. As services are performed, the liability decreases and revenue is recognized.

Example: FastForward received $3,000 for 60 days of service. After 5 days, $250 is earned and recognized as revenue.

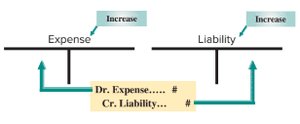

Adjusting Entries for Accrued Expenses

Accrued Expenses

Accrued expenses are costs incurred but not yet paid or recorded. An adjusting entry increases both the expense and the liability.

Example: FastForward owes $210 in salaries at year end.

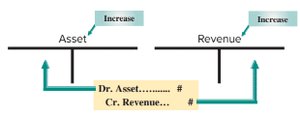

Adjusting Entries for Accrued Revenues

Accrued Revenues

Accrued revenues are earned but not yet received or recorded. An adjusting entry increases both the asset (accounts receivable) and the revenue.

Example: FastForward earned $1,800 in consulting revenue by year end, not yet received.

Preparing Financial Statements from Adjusted Trial Balance

Financial statements are prepared in a specific order using the adjusted trial balance:

Prepare the income statement using revenue and expense accounts.

Prepare the statement of owner's equity using capital and withdrawals accounts, and net income from step 1.

Prepare the balance sheet using asset and liability accounts, and updated capital from step 2.

Prepare the statement of cash flows from changes in cash flows for the period.

Profit Margin: Computation and Analysis

The profit margin ratio measures net income as a percentage of net sales, indicating profitability.

Formula:

Example: Visa's profit margin increased from 36% to 53% over two years, showing improved profitability.

Summary Table: Types of Adjusting Entries

Type | Account Affected | Adjustment Direction | Journal Entry |

|---|---|---|---|

Prepaid Expense | Asset ↓, Expense ↑ | Decrease asset, increase expense | Dr. Expense, Cr. Asset |

Unearned Revenue | Liability ↓, Revenue ↑ | Decrease liability, increase revenue | Dr. Liability, Cr. Revenue |

Accrued Expense | Expense ↑, Liability ↑ | Increase expense, increase liability | Dr. Expense, Cr. Liability |

Accrued Revenue | Asset ↑, Revenue ↑ | Increase asset, increase revenue | Dr. Asset, Cr. Revenue |

Practice: Adjusting Journal Entries and Net Income Calculation

Exercises include preparing adjusting entries for depreciation, prepaid insurance, supplies, unearned revenue, prepaid rent, and accrued wages. Adjusted net income is calculated by updating revenues and expenses based on these entries.

Adjusted Net Income Formula:

Example Calculation: If adjusted revenue is $90,700 and adjusted expenses are $83,780, then adjusted net income is $6,920.

Conclusion

Adjusting entries are essential for accurate financial reporting under accrual accounting. They ensure that revenues and expenses are matched to the correct periods, providing a true picture of financial performance and position.