Back

BackAppendix E: Accounting for Investments – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Appendix E: Investments

Introduction

This section covers the accounting for investments, focusing on why companies invest in other companies, and the methods used to account for equity and debt securities. The material aligns with the core topics in financial accounting, specifically the recognition, measurement, and reporting of investments on financial statements.

Why Companies Invest in Other Companies

Purposes of Investment

Short-term investments: Companies use excess cash to earn additional income and raise cash for future operations. Income may include interest, dividends, and gains or losses on sales of securities.

Long-term strategic investments: Companies may invest to gain influence or control over other companies, supporting strategic objectives.

Investments are classified as either short-term (current assets) or long-term (non-current assets) based on liquidity and management's intent.

Types of Securities

Equity Securities: Investments in the capital stock of other companies.

Debt Securities: Investments in bonds or notes payable issued by other entities.

Accounting for Equity Securities

Insignificant Influence (Less than 20% Ownership)

When the investor owns less than 20% of the investee's voting stock, the investment is accounted for at fair value. All investments are initially recorded at cost. Subsequent measurement depends on the type of security and the level of influence.

Dividends received: Recorded as dividend revenue.

Fair value adjustments: At each reporting date, investments are adjusted to fair value. Unrealized gains and losses are recognized in income (for trading securities) or in other comprehensive income (for available-for-sale securities).

Example: Apple Inc. purchases 5,000 shares of Intel at $20 per share ($100,000 total). At year-end, if the fair value is $22 per share, the investment is adjusted to $110,000, recognizing a $10,000 unrealized gain.

Realized vs. Unrealized Gains and Losses

Unrealized gains/losses: Changes in fair value before sale; reported in income or OCI depending on classification.

Realized gains/losses: Recognized when the investment is sold; difference between sale price and carrying amount.

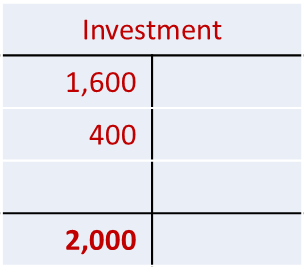

Practice Example: Trading Securities

Grady Company purchases 400 shares at $4 each ($1,600). At year-end, the fair value is $5 per share ($2,000). The unrealized gain is $400.

Journal Entry at Purchase: Debit Investment $1,600; Credit Cash $1,600

Fair Value Adjustment: Debit Investment $400; Credit Unrealized Gain $400

Accounting for Equity Securities with Significant Influence (20%–50% Ownership)

The Equity Method

When the investor owns 20%–50% of the investee's voting stock, the equity method is used. The investor is presumed to have significant influence over the investee's operations.

Initial recognition: Investment recorded at cost.

Share of income: Investor recognizes its share of the investee's net income as investment income.

Dividends received: Reduce the carrying amount of the investment (not recognized as income).

Example: Intel acquires 49% of IM Flash Technologies for $490 million. If IM Flash earns $300 million, Intel recognizes $147 million as income (49%). If IM Flash pays $200 million in dividends, Intel reduces its investment by $98 million (49%).

Investment balance: Original cost + share of income – share of dividends.

Accounting for Equity Securities with Controlling Influence (More than 50% Ownership)

Consolidation Accounting

When the investor owns more than 50% of the investee's voting stock, the investor is considered to have a controlling interest. The investee becomes a subsidiary, and the investor is the parent company.

Consolidated financial statements: Combine the financial statements of the parent and all subsidiaries as if they were a single entity.

Elimination of intercompany accounts: All intercompany transactions and balances are eliminated in consolidation.

No investment account for subsidiary: The investment is not shown as an asset; the subsidiary's assets and liabilities are included directly.

Accounting for Debt Securities

Categories of Debt Investments

Trading securities: Intended to be sold in the near term; reported at fair value with unrealized gains/losses in income.

Available-for-sale securities: Intended to be held for more than a year but not until maturity; reported at fair value with unrealized gains/losses in OCI. Additional info: Not covered in detail in this class.

Held-to-maturity securities: Company intends and is able to hold until maturity; reported at amortized cost.

Held-to-Maturity Securities: Amortized Cost Method

Investments in bonds intended to be held to maturity are recorded at cost and subsequently adjusted for the amortization of any premium or discount.

Interest revenue: Recognized as earned, typically semiannually.

Discount or premium: Amortized over the life of the bond, affecting the carrying value of the investment.

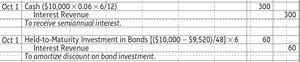

Example: Purchase and Amortization of Bonds

Intel Capital purchases $10,000 of 6% bonds at 95.2 ($9,520). The $480 discount is amortized over the bond's life. Interest is received semiannually.

Journal Entry at Purchase: Debit Held-to-Maturity Investment in Bonds $9,520; Credit Cash $9,520

Interest Receipt: Debit Cash $300; Credit Interest Revenue $300

Discount Amortization: Debit Held-to-Maturity Investment in Bonds $60; Credit Interest Revenue $60

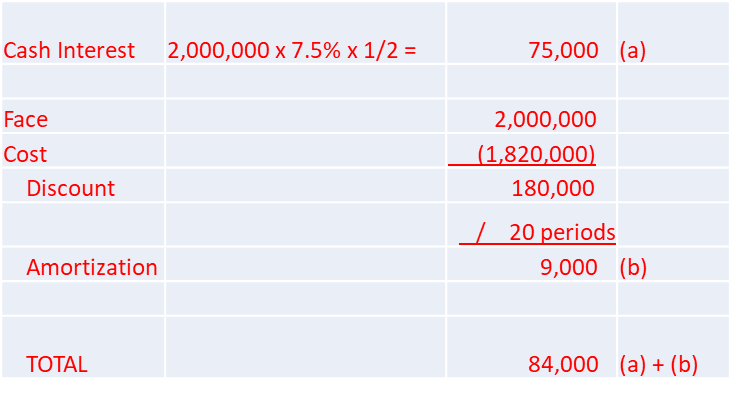

Practice Example: Debt Investment

ABC Corporation purchases $2,000,000 of 7.5% bonds for $1,820,000. The first semiannual interest receipt is $75,000. Amortization of the $180,000 discount over 20 periods is $9,000 per period. Total interest revenue recognized is $84,000 for the first period.

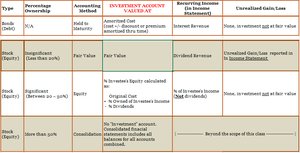

Summary Table: Accounting for Investments

The following table summarizes the accounting treatment for different types of investments based on the percentage of ownership and the nature of the security.

Key Terms and Concepts

Fair Value: The price that would be received to sell an asset in an orderly transaction between market participants.

Equity Method: Accounting method for investments with significant influence, recognizing share of investee's income and reducing for dividends received.

Consolidation: Combining financial statements of parent and subsidiaries into one set of statements.

Amortized Cost: The initial cost of an investment adjusted for the amortization of any premium or discount.

Unrealized Gain/Loss: Change in value of an investment not yet sold.

Realized Gain/Loss: Gain or loss recognized upon sale of an investment.