Back

BackBookkeeping and Financial Accounting Fundamentals: A Comprehensive Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Bookkeeping Basics

Role and Responsibilities of a Bookkeeper

The bookkeeper's primary role is to systematically track and record all financial transactions of a business. This function is essential for maintaining accurate financial records, supporting tax compliance, and generating reliable financial statements. Bookkeepers must uphold high ethical standards, including honesty, objectivity, confidentiality, and professionalism, to maintain trust and integrity in their work.

Record financial transactions: Systematic documentation of all business financial events.

Reconcile bank accounts: Matching business records with bank statements to ensure accuracy.

Manage accounts receivable and payable: Tracking money owed to and by the business.

Assist with tax compliance: Collaborating with tax professionals to ensure accurate reporting.

Generate financial statements: Preparing core documents that summarize financial activities and position.

Ethical Responsibilities

Bookkeepers are entrusted with sensitive information and must adhere to four key ethical principles:

Honesty: Report data accurately and transparently.

Objectivity: Avoid conflicts of interest and personal bias.

Professionalism: Maintain credentials and act courteously.

Confidentiality: Protect client information from unauthorized disclosure or personal gain.

Accounting Basics

The Accounting Equation

The accounting equation is the foundation of all financial accounting and is expressed as:

This equation ensures that the business's resources (assets) are always balanced by claims from creditors (liabilities) and owners (equity). The balance sheet is a direct representation of this equation.

Assets: Resources owned by the business (e.g., cash, inventory, equipment).

Liabilities: Obligations owed to others (e.g., loans, accounts payable).

Equity: Owner's residual interest after liabilities are paid.

Categorizing Transactions

Transactions are categorized as either revenue (income from operations) or expenses (costs incurred to generate revenue). Accurate categorization is essential for preparing the income statement and assessing net income or loss.

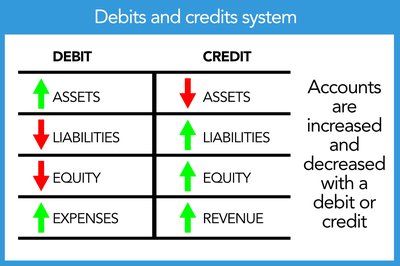

Debits and Credits

Debits and credits are the dual aspects of every transaction in double-entry bookkeeping. The cardinal rule is that total debits must always equal total credits.

Debits (Dr): Increase assets or expenses; decrease liabilities, equity, or revenue.

Credits (Cr): Increase liabilities, equity, or revenue; decrease assets or expenses.

Accounting Principles

Key Principles and Assumptions

Economic Entity Assumption: Business transactions are separate from personal transactions.

Reliability Assumption: Only verifiable transactions are recorded.

Full Disclosure Principle: All information relevant to decision-makers must be disclosed.

Conservatism Assumption: Record potential losses, not gains, when in doubt.

Materiality Principle: Only significant information is required to be reported.

Consistency Principle: Use the same accounting methods over time.

Monetary Unit Assumption: Record all transactions in a single currency (e.g., USD).

Going Concern Assumption: Assume the business will continue operating into the foreseeable future.

The Accounting Cycle

Overview of the Accounting Cycle

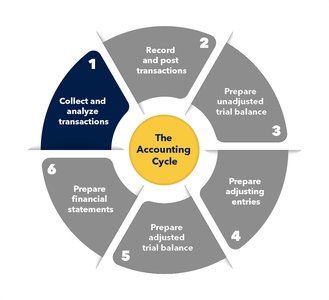

The accounting cycle is a systematic process for recording and processing all financial transactions of a business, culminating in the preparation of financial statements. The cycle consists of six main steps:

Collect and analyze transactions

Record and post transactions

Prepare unadjusted trial balance

Prepare adjusting entries

Prepare adjusted trial balance

Prepare financial statements

Step 1: Collect and Analyze Transactions

Gather all source documents (receipts, invoices, bank statements) and determine which events are financial transactions that impact the business.

Step 2: Record and Post Transactions

Record transactions in the journal and post them to the general ledger, ensuring each transaction is categorized correctly and debits equal credits.

Step 3: Prepare Unadjusted Trial Balance

List all account balances from the general ledger to check that total debits equal total credits before adjustments.

Step 4: Prepare Adjusting Entries

Make end-of-period adjustments for accruals, deferrals, depreciation, and tax adjustments to ensure revenues and expenses are recognized in the correct period.

Deferrals: Adjust for transactions assigned to a different period (e.g., prepaid expenses, unearned revenue).

Accruals: Record revenues earned or expenses incurred but not yet received or paid.

Depreciation: Allocate the cost of tangible assets over their useful lives.

Step 5: Prepare Adjusted Trial Balance

Update the trial balance to reflect all adjustments, ensuring the books are accurate before preparing financial statements.

Step 6: Prepare Financial Statements

Generate the four main financial statements: income statement, balance sheet, statement of equity, and statement of cash flows.

Financial Statements

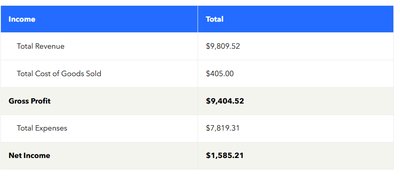

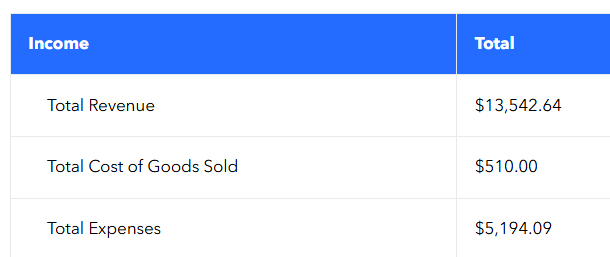

Income Statement

The income statement (profit and loss statement) summarizes revenues, cost of goods sold, and expenses to determine net income for a specific period.

Gross Profit:

Net Income:

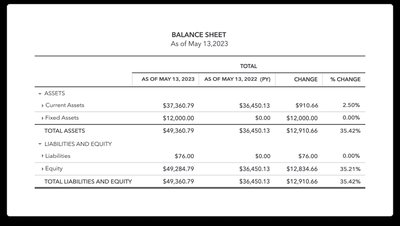

Balance Sheet

The balance sheet provides a snapshot of the business's financial position at a specific date, showing assets, liabilities, and equity.

Statement of Equity

This statement details changes in owner's equity over the reporting period, including investments, net income, and withdrawals.

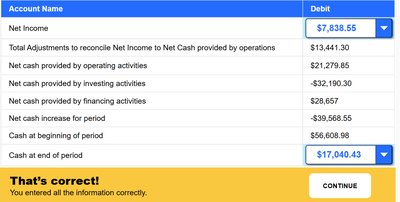

Statement of Cash Flows

The statement of cash flows tracks the movement of cash in and out of the business, categorized into operating, investing, and financing activities. It reconciles net income to actual cash available.

Double-Entry Bookkeeping and T-Accounts

Double-Entry System

Every transaction affects at least two accounts, maintaining the balance of the accounting equation. T-accounts are used to visualize the effects of debits and credits on each account.

Debits: Left side of the T-account

Credits: Right side of the T-account

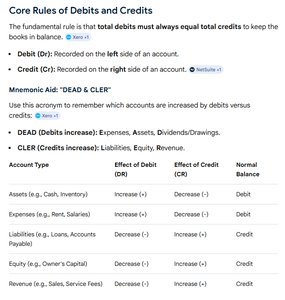

Core Rules of Debits and Credits

Account Type | Debit Effect | Credit Effect |

|---|---|---|

Assets | Increase (+) | Decrease (-) |

Expenses | Increase (+) | Decrease (-) |

Liabilities | Decrease (-) | Increase (+) |

Equity | Decrease (-) | Increase (+) |

Revenue | Decrease (-) | Increase (+) |

Accounting Methods

Cash-Basis Accounting

Records revenues and expenses only when cash is received or paid. Simple but does not track accounts receivable or payable.

Accrual Accounting

Records revenues when earned and expenses when incurred, regardless of cash flow. Required by GAAP and provides a more accurate picture of financial position.

Modified Cash-Basis Accounting

A hybrid method that records most transactions on a cash basis but includes accounts receivable and payable for better tracking of obligations.

Adjusting Entries and Depreciation

Purpose of Adjusting Entries

Adjusting entries ensure that all revenues and expenses are recognized in the correct accounting period, leading to more accurate financial statements.

Depreciation

Depreciation allocates the cost of a tangible asset over its useful life, matching expense recognition with the asset's revenue generation.

Straight-Line Depreciation Formula:

Summary Table: Financial Statement Relationships

Statement | Main Purpose | Key Components |

|---|---|---|

Income Statement | Shows profitability over a period | Revenue, Expenses, Net Income |

Balance Sheet | Snapshot of financial position | Assets, Liabilities, Equity |

Statement of Equity | Tracks changes in equity | Owner Investments, Net Income, Withdrawals |

Statement of Cash Flows | Tracks cash movement | Operating, Investing, Financing Activities |

Conclusion

Mastering the fundamentals of bookkeeping and financial accounting—including the accounting equation, double-entry system, accounting cycle, and preparation of financial statements—provides a solid foundation for analyzing and communicating the financial health of any business. Ethical conduct and adherence to core accounting principles ensure the reliability and integrity of financial information.