Back

Back(26) Capital Investment Decisions: Methods and Applications

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Capital Investment Decisions

Introduction to Capital Budgeting

Capital budgeting is a critical process in managerial accounting, involving the planning and evaluation of investments in long-term assets. These decisions impact a company's strategic direction and financial health for years to come.

Capital asset: An operational asset used for a long period of time.

Capital investment: The acquisition of a capital asset.

Capital budgeting: The process of planning to invest in long-term assets in a way that returns the most profitability to the company.

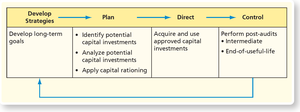

The Capital Budgeting Process

The capital budgeting process involves several stages, from developing strategies to controlling and evaluating investments. This process ensures that only the most beneficial projects are selected and monitored for performance.

Develop long-term goals

Identify and analyze potential capital investments

Apply capital rationing to prioritize projects

Acquire and use approved investments

Perform post-audits to compare actual and projected results

Capital rationing is the process of ranking and choosing among alternative capital investments based on the availability of funds. Post-audit compares actual results to projections.

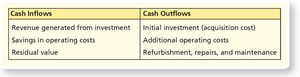

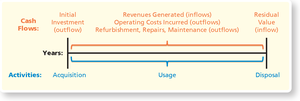

Cash Flows in Capital Budgeting

Unlike GAAP, which is based on accrual accounting, capital budgeting focuses on cash flows. Understanding the sources and uses of cash is essential for evaluating investment opportunities.

Cash Inflows | Cash Outflows |

|---|---|

Revenue generated from investment | Initial investment (acquisition cost) |

Savings in operating costs | Additional operating costs |

Residual value | Refurbishment, repairs, and maintenance |

Methods of Capital Investment Analysis

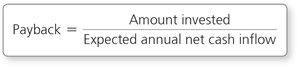

Payback Method

The payback method measures the length of time it takes to recover the cost of an investment through net cash inflows. It is a simple tool for evaluating the risk and liquidity of a project, especially for shorter-term investments.

Formula:

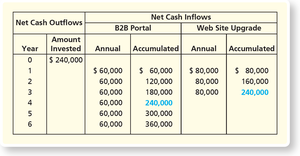

Example: If Smart Touch Learning invests $240,000 in a B2B portal expecting $60,000 per year for six years, the payback period is:

For a website upgrade with $80,000 annual inflows for three years:

Year | Amount Invested | B2B Portal Annual | B2B Portal Accumulated | Web Site Upgrade Annual | Web Site Upgrade Accumulated |

|---|---|---|---|---|---|

0 | $240,000 | ||||

1 | $60,000 | $60,000 | $80,000 | $80,000 | |

2 | $60,000 | $120,000 | $80,000 | $160,000 | |

3 | $60,000 | $180,000 | $80,000 | $240,000 | |

4 | $60,000 | $240,000 | |||

5 | $60,000 | $300,000 | |||

6 | $60,000 | $360,000 |

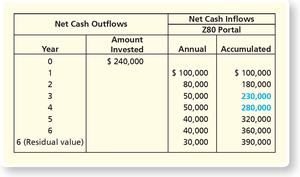

Payback with Unequal Cash Flows

When annual net cash inflows are unequal, the payback period is calculated by accumulating inflows until the initial investment is recovered.

Year | Amount Invested | Z80 Portal Annual | Z80 Portal Accumulated |

|---|---|---|---|

0 | $240,000 | ||

1 | $100,000 | $100,000 | |

2 | $80,000 | $180,000 | |

3 | $50,000 | $230,000 | |

4 | $50,000 | $280,000 | |

5 | $40,000 | $320,000 | |

6 (Residual value) | $30,000 | $390,000 |

The payback for the Z80 portal is calculated as:

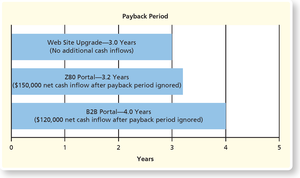

Comparing Payback Periods

Rank | Project | Payback Period |

|---|---|---|

1 | Web site upgrade | 3.0 years |

2 | Z80 portal | 3.2 years |

3 | B2B portal | 4.0 years |

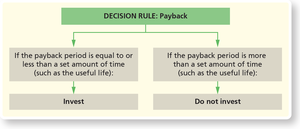

Decision Rule: Invest if the payback period is less than or equal to the set time (such as the useful life); otherwise, do not invest.

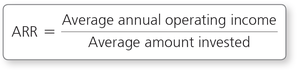

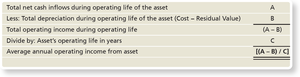

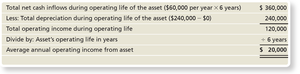

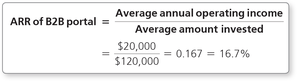

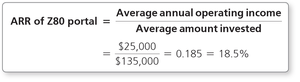

Accounting Rate of Return (ARR)

The accounting rate of return (ARR) measures the profitability of an investment based on accounting income rather than cash flows. It is useful for comparing projects with similar risk and time horizons.

Formula:

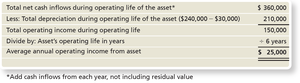

To calculate ARR, first determine the average annual operating income:

Example (B2B Portal):

Example (Z80 Portal):

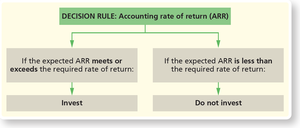

Decision Rule: Invest if the expected ARR meets or exceeds the required rate of return; otherwise, do not invest.

Time Value of Money

Concept and Importance

The time value of money recognizes that a dollar received today is worth more than a dollar received in the future due to its earning potential. This concept is fundamental to capital budgeting decisions.

Principal amount (p): The amount of the investment.

Number of periods (n): The investment's duration.

Interest rate (i): The annual percentage earned on the investment.

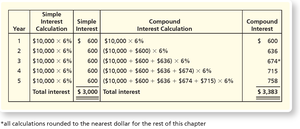

Simple vs. Compound Interest

Simple interest is calculated only on the principal, while compound interest is calculated on both the principal and previously earned interest.

Year | Simple Interest Calculation | Simple Interest | Compound Interest Calculation | Compound Interest |

|---|---|---|---|---|

1 | $600 | $600 | ||

2 | $600 | ( | $636$ | |

3 | $600 | ( | $674$ | |

4 | $600 | ( | $715$ | |

5 | $600 | ( | $758$ | |

Total | $3,000 | $3,383 |

Future Value and Present Value

The future value of an investment is its worth at a future date, including interest earned. The present value is the amount that must be invested today to achieve a specific future value, discounted at a given interest rate.

Future Value Formula:

Additional info: For more complex calculations, use present and future value tables (Appendix A) to find the appropriate factors for lump sums and annuities.