Back

BackCash Basis and Accrual Basis Accounting: Adjusting Entries and the Accounting Cycle

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Cash Basis and Accrual Basis Accounting

Key Differences Between Cash Basis and Accrual Basis

The cash basis and accrual basis are two fundamental methods for recording accounting transactions. Understanding their differences is essential for accurate financial reporting and compliance with generally accepted accounting principles (GAAP).

Cash Basis: Revenues and expenses are recorded only when cash is received or paid.

Accrual Basis: Revenues are recorded when earned, and expenses are recorded when incurred, regardless of when cash is exchanged. This method provides a more accurate picture of a business’s financial performance.

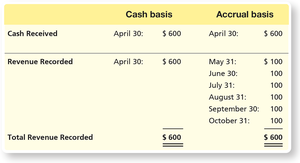

Cash basis | Accrual basis | |

|---|---|---|

Cash Received | April 30: $600 | April 30: $600 |

Revenue Recorded | April 30: $600 | May 31: $100 June 30: $100 July 31: $100 August 31: $100 September 30: $100 October 31: $100 |

Total Revenue Recorded | $600 | $600 |

Time Period Concept

The time period concept requires that accounting information is reported for specific periods, such as months, quarters, or years. This allows for meaningful comparisons and performance evaluation over time.

The Revenue Recognition Principle

The revenue recognition principle mandates that revenue is recorded when goods or services are provided to customers, not necessarily when cash is received. This ensures that financial statements reflect the actual earning process.

The Expense (Matching) Principle

The matching principle requires that all expenses incurred to generate revenue are recorded in the same period as the related revenues. This principle ensures the accurate computation of net income or net loss for a given period.

All expenses are recorded when incurred.

Expenses are matched against the revenues of the period.

Adjusting Entries

Purpose and Types of Adjusting Entries

Adjusting entries are made at the end of the accounting period to ensure that revenues and expenses are recorded in the correct period. They also update asset and liability accounts to reflect their true balances.

Needed to properly measure net income (loss) and asset/liability balances.

Two main categories: Deferrals and Accruals.

Deferrals

Deferrals postpone the recognition of revenue or expense to a future period after cash has been received or paid. Types include:

Deferred Expenses (Prepaid Expenses): Costs paid in advance and recorded as assets until used.

Deferred Revenues (Unearned Revenues): Cash received before services are performed; recorded as liabilities until earned.

Accruals

Accruals recognize expenses or revenues before cash is paid or received. Types include:

Accrued Expenses: Expenses incurred but not yet paid.

Accrued Revenues: Revenues earned but not yet received in cash.

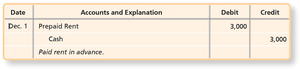

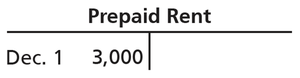

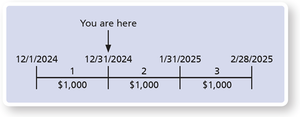

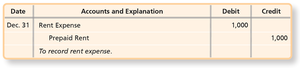

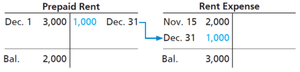

Deferred Expenses

Prepaid Rent Example

When rent is paid in advance, it is recorded as a prepaid expense (asset). As time passes, the asset is reduced and rent expense is recognized.

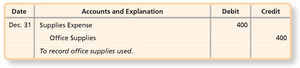

Office Supplies Example

Office supplies purchased are initially recorded as an asset. At period end, the amount used is transferred to supplies expense.

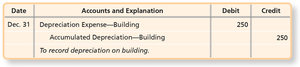

Depreciation

Depreciation of Plant Assets

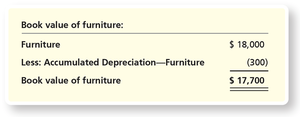

Depreciation is the allocation of the cost of long-lived assets (such as buildings, equipment, and furniture) over their useful lives. The straight-line method allocates an equal amount of depreciation each year.

Residual value: Expected value at the end of the asset’s useful life.

Book value: Asset cost minus accumulated depreciation.

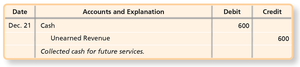

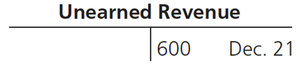

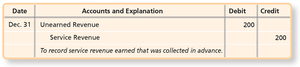

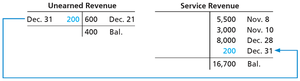

Deferred Revenues

Unearned Revenue Example

When cash is received before services are performed, it is recorded as unearned revenue (liability). As services are performed, revenue is recognized.

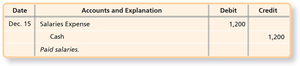

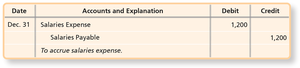

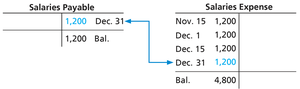

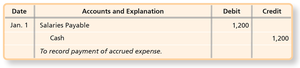

Accrued Expenses

Accrued Salaries Expense Example

Accrued expenses are recorded when incurred, even if not yet paid. For example, salaries earned by employees but not yet paid at period end are accrued as a liability.

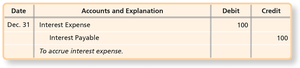

Accrued Interest Expense Example

Interest expense is accrued for the period it is incurred, even if not yet paid. The formula for interest is:

Accrued Revenues

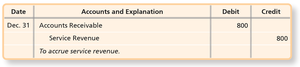

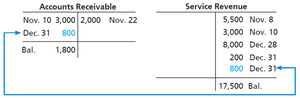

Accrued Service Revenue Example

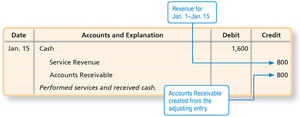

Accrued revenues arise when services are performed but cash has not yet been received. The revenue is recognized and an asset (accounts receivable) is recorded.

Adjusted Trial Balance and Financial Statements

Purpose of the Adjusted Trial Balance

An adjusted trial balance lists all accounts and their adjusted balances after posting adjusting entries. It ensures total debits equal total credits and is used to prepare financial statements.

Closing Process

Purpose and Steps

The closing process occurs at the end of the accounting period to zero out temporary accounts (revenues, expenses, dividends) and transfer their balances to retained earnings. This ensures each period’s net income is measured separately.

Temporary accounts: Closed at period end (revenues, expenses, dividends).

Permanent accounts: Not closed (assets, liabilities, common stock, retained earnings).

Post-Closing Trial Balance

The post-closing trial balance lists only permanent accounts and their balances after closing entries are posted, confirming that temporary accounts have been reset for the next period.