Back

BackCash, Receivables, and Revenue: Reporting and Valuation in Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Cash and Receivables: Reporting and Valuation

Overview of Asset Valuation

In financial accounting, different asset types are valued using distinct measurement bases to ensure accurate and relevant financial reporting. The valuation method depends on the nature of the asset and the associated risks or uncertainties.

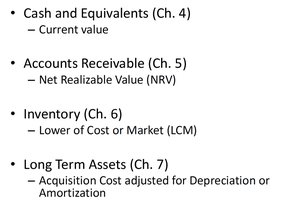

Cash and Equivalents (Ch. 4): Reported at current value.

Accounts Receivable (Ch. 5): Reported at Net Realizable Value (NRV).

Inventory (Ch. 6): Reported at the Lower of Cost or Market (LCM).

Long-Term Assets (Ch. 7): Reported at acquisition cost adjusted for depreciation or amortization.

Reporting Cash and Cash Equivalents

Definition and Examples

Cash includes money and any instrument that banks will accept for deposit and immediate credit, such as currency, checking accounts, and certain negotiable instruments (e.g., checks, money orders).

Cash equivalents are short-term, highly liquid investments with original maturities of three months or less, which are readily convertible to known amounts of cash and are subject to an insignificant risk of changes in value. Examples include:

Certificates of deposit (time deposits)

Treasury bills

Cash and equivalents are reported together on the balance sheet and exclude most equity securities and illiquid investments.

Accounts Receivable and Revenue Recognition

Revenue Recognition Process

Revenue recognition is a critical process in financial accounting, as it determines when a company can record revenue in its financial statements. The process follows a five-step model:

Identify the contract with the customer

Identify the separate performance obligations

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognize revenue when (or as) the entity satisfies a performance obligation

Example: A company sells goods on credit, offering customers the ability to pay later. Revenue is recognized when the performance obligation is satisfied, even if cash is not yet received.

Accounts Receivable (A/R)

Accounts receivable are amounts owed by customers from prior revenue transactions. They are initially recognized at the time of sale and subsequently adjusted for collections and uncollectible accounts.

When a sale is made on credit: Dr. Accounts Receivable (A) Cr. Revenue (RE/SE)

When cash is collected: Dr. Cash (A) Cr. Accounts Receivable (A)

Uncollectible Accounts (Bad Debts)

Some customers may not pay their debts, resulting in uncollectible accounts (also called bad debts or doubtful accounts). There are two main methods to account for these:

Direct Write-off Method: Recognizes losses when specific accounts are deemed uncollectible. Not allowed under GAAP/IFRS due to violation of the matching principle.

Allowance Method: Estimates total expected losses in the period of the related sales, matching expenses to revenues. Required under GAAP/IFRS.

Valuation of Accounts Receivable

Accounts receivable are reported on the balance sheet at Net Realizable Value (NRV):

Gross Accounts Receivable (total owed by customers)

Less: Allowance for Uncollectible Accounts (AUA) (estimated uncollectible amount)

= Net Accounts Receivable

The Allowance for Uncollectible Accounts is a contra-asset account with a credit balance, reducing the gross A/R to its expected collectible amount.

Estimating Uncollectible Accounts

Methods of Estimation

There are two common methods for estimating the allowance for uncollectible accounts:

Percentage-of-Sales Method: Estimates uncollectible expense as a percentage of credit sales for the period.

Aging-of-Receivables Method: Estimates uncollectibles based on the age of outstanding receivables, applying higher percentages to older accounts.

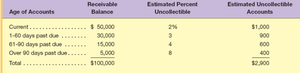

Aging-of-Receivables Example

The following table illustrates how the aging method is applied to estimate uncollectible accounts:

Age of Accounts | Receivable Balance | Estimated Percent Uncollectible | Estimated Uncollectible Accounts |

|---|---|---|---|

Current | $50,000 | 2% | $1,000 |

1-60 days past due | $30,000 | 3% | $900 |

61-90 days past due | $15,000 | 4% | $600 |

Over 90 days past due | $5,000 | 8% | $400 |

Total | $100,000 | $2,900 |

Journal Entries for Allowance Method

To record estimated uncollectibles: Dr. Uncollectible-Account Expense (RE/SE) Cr. Allowance for Uncollectible Accounts (XA)

To write off a specific account: Dr. Allowance for Uncollectible Accounts (XA) Cr. Accounts Receivable (A)

Impact: Write-offs do not affect net income, as the expense was already recognized when estimated.

Notes Receivable and Interest Revenue

Definition and Calculation

Notes receivable are formal written promises to receive a specific amount of cash, usually with interest, at a future date. Key terms include:

Principal: Amount borrowed/lent

Interest: Cost of borrowing, stated as an annual rate

Maturity date: Date payment is due

Maturity value: Principal plus interest

Interest calculation formula:

Example: For a $1,000 note at 12% interest for 60 days: Interest = $1,000 × 12% × (60/365) = $19.73 (rounded)

Accounts Receivable Turnover and Days Sales Outstanding

Key Ratios for Analysis

These ratios help assess how efficiently a company collects cash from customers:

Accounts Receivable Turnover: Number of times receivables are collected during a period.

Days Sales Outstanding (DSO): Average number of days to collect receivables.

Interpretation: Higher turnover and lower DSO indicate faster cash collection.

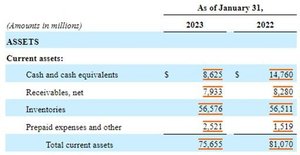

Example: Walmart's Receivables Turnover and DSO

Net Sales (2023): $611,289 million

Average Receivables, net: (8,280 + 7,933) / 2 = $8,106.5 million

Receivables Turnover: $611,289 / $8,106.5 = 75.4

DSO: 365 / 75.4 = 4.8 days

This means Walmart collects cash from sales in about 4.8 days on average.

Summary Table: Asset Valuation Methods

Asset Type | Valuation Basis | Relevant Chapter |

|---|---|---|

Cash and Equivalents | Current Value | Ch. 4 |

Accounts Receivable | Net Realizable Value (NRV) | Ch. 5 |

Inventory | Lower of Cost or Market (LCM) | Ch. 6 |

Long-Term Assets | Acquisition Cost (adjusted for depreciation/amortization) | Ch. 7 |

Additional info: The notes above integrate textbook-level explanations, examples, and formulas to provide a comprehensive review of cash, receivables, and revenue reporting and analysis for financial accounting students.