Back

BackChapter 1: Accounting and the Business Environment – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accounting and the Business Environment

Introduction to Accounting

Accounting is a fundamental information system that measures, processes, and communicates financial information about a business. It is essential for both internal and external decision makers, providing the data needed to make informed business decisions.

Measures business activities: Accounting records all financial transactions and events.

Processes information: Data is organized and summarized into useful reports.

Communicates results: Reports are shared with stakeholders to support decision making.

Users of Accounting Information

Accounting information is used by a variety of stakeholders, both external and internal, to make economic decisions.

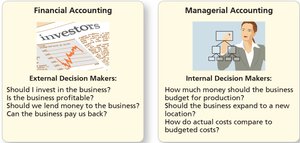

External users (Financial Accounting): Investors, creditors, and taxing authorities use financial statements to assess the financial health and performance of a business.

Internal users (Managerial Accounting): Managers and employees use accounting data for planning, controlling, and decision-making within the organization.

Types of Accountants and Accounting Positions

Accountants may serve the public, work within a single company, or be employed by government agencies. Key certifications include:

Certified Public Accountants (CPAs): Serve the general public, often in auditing, tax, or consulting roles.

Certified Management Accountants (CMAs): Specialize in internal financial management and analysis.

Accounting positions can be classified as public, private, or governmental.

Organizations and Rules That Govern Accounting

Governing Organizations

Several organizations oversee the creation and enforcement of accounting standards:

Financial Accounting Standards Board (FASB): Sets accounting standards in the U.S.

Securities and Exchange Commission (SEC): Regulates U.S. financial markets and enforces accounting standards for public companies.

International Accounting Standards Board (IASB): Issues International Financial Reporting Standards (IFRS) used globally.

Generally Accepted Accounting Principles (GAAP)

GAAP are the rules and guidelines that govern financial accounting and reporting in the U.S. Useful accounting information must be:

Relevant: Capable of influencing decisions.

Faithfully represented: Complete, neutral, and free from error.

Key Accounting Assumptions and Principles

Economic Entity Assumption: Each business is treated as a separate entity from its owners or other businesses.

Cost Principle: Assets are recorded at their historical cost.

Going Concern Assumption: The business will continue to operate in the foreseeable future.

Monetary Unit Assumption: Only transactions that can be measured in monetary terms are recorded.

Business Organization Types

Sole Proprietorship: Owned by one individual.

Partnership: Owned by two or more individuals.

Corporation: Separate legal entity, ownership divided into shares of stock.

Limited Liability Company (LLC): Hybrid structure with limited liability for owners.

Ethics and Regulation in Accounting

Audits: Independent examination of financial statements.

Sarbanes-Oxley Act (SOX): U.S. law requiring companies to review and improve internal controls to prevent fraud.

The Accounting Equation

Definition and Components

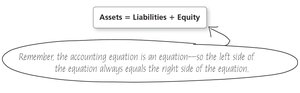

The accounting equation is the foundation of double-entry accounting, showing the relationship between a company's assets, liabilities, and equity:

Assets: Economic resources expected to benefit the business (e.g., cash, inventory, land).

Liabilities: Debts owed to creditors (e.g., accounts payable, notes payable).

Equity: Owners' claims on the business, consisting of contributed capital and retained earnings.

The basic accounting equation is:

Expanded Accounting Equation

Equity can be further broken down into contributed capital (common stock) and retained earnings (revenues, expenses, dividends):

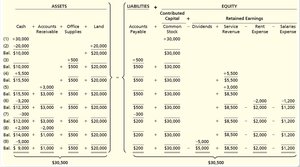

Analyzing Transactions Using the Accounting Equation

What is a Transaction?

A transaction is any event that affects the financial position of a business and can be measured reliably. Only measurable events are recorded in the accounting system.

Transaction Analysis Example: Smart Touch Learning

Each transaction affects at least two accounts in the accounting equation. Below are examples of how common transactions impact the equation:

Owner Contribution: Increases both cash (asset) and common stock (equity).

Purchase of Land for Cash: Increases land (asset), decreases cash (asset).

Purchase of Supplies on Account: Increases supplies (asset) and accounts payable (liability).

Earning Revenue: Increases cash or accounts receivable (asset) and service revenue (equity).

Paying Expenses: Decreases cash (asset) and increases expenses (reduces equity).

Paying Dividends: Decreases cash (asset) and increases dividends (reduces equity).

Preparation of Financial Statements

Types of Financial Statements

Financial statements are formal records that communicate the financial activities and condition of a business. The four primary statements are:

Income Statement: Reports revenues and expenses to show net income or net loss for a period.

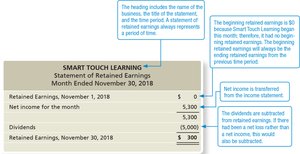

Statement of Retained Earnings: Shows changes in retained earnings from net income and dividends.

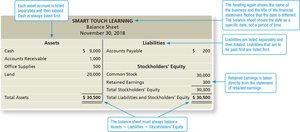

Balance Sheet: Presents assets, liabilities, and equity as of a specific date.

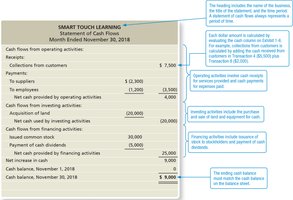

Statement of Cash Flows: Reports cash inflows and outflows from operating, investing, and financing activities.

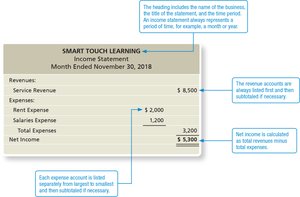

Income Statement

The income statement summarizes revenues and expenses, resulting in net income or net loss for a specific period.

Statement of Retained Earnings

This statement explains the changes in retained earnings over a period, including net income and dividends paid.

Balance Sheet

The balance sheet provides a snapshot of the company's financial position at a specific date, listing assets, liabilities, and stockholders' equity.

Statement of Cash Flows

This statement details the cash inflows and outflows from operating, investing, and financing activities during a period.

Evaluating Business Performance: Return on Assets (ROA)

Return on Assets (ROA)

ROA is a key profitability metric that measures how efficiently a company uses its assets to generate net income. It is calculated as:

Net Income: Found on the income statement.

Average Total Assets: Calculated as the average of beginning and ending total assets for the period.

A higher ROA indicates more efficient use of assets.