Back

BackChapter 1: Conceptual Framework and Financial Statements – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Statements and the Role of Accounting

Accounting: An Information System

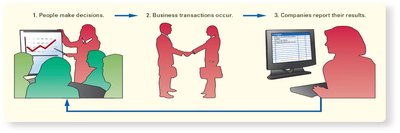

Accounting is the information system that measures business activities, processes data into financial statements and reports, and communicates results to decision makers. It is often referred to as the "language of business." The accounting cycle is the process by which a company’s financial statements are prepared.

Key Point: Accounting provides critical information for both internal and external decision makers.

Key Point: The flow of accounting information begins with business decisions, followed by business transactions, and ends with companies reporting their results.

Example: Investors use financial statements to decide whether to invest in a company, while managers use them for planning and control.

Types of Accounting and Business Organizations

Financial vs. Managerial Accounting

There are two main types of accounting:

Financial Accounting: Provides information to external users (investors, creditors, government agencies).

Managerial Accounting: Provides information to internal users (managers, executives).

Business entities can be organized as proprietorships, partnerships, LLCs, or corporations, each with different ownership structures and liability characteristics.

Proprietorship: Single owner, personally liable.

Partnership: Two or more owners, general partners personally liable.

LLC: Members not personally liable.

Corporation: Stockholders not personally liable.

Rules and Conceptual Framework of Financial Accounting

GAAP and the FASB

Financial accounting follows Generally Accepted Accounting Principles (GAAP), established by the Financial Accounting Standards Board (FASB). The conceptual framework is outlined in the Statement of Financial Accounting Concepts (SFAC).

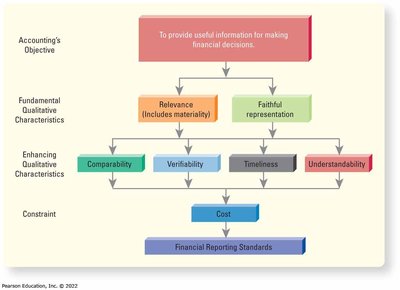

Objective: To provide financial information useful for decision making by investors and creditors.

Qualitative Characteristics of Accounting Information

Useful accounting information is distinguished by fundamental and enhancing qualitative characteristics.

Fundamental Qualities:

Relevance: Information must be capable of making a difference in decisions (includes materiality).

Faithful Representation: Information must accurately reflect what really existed or happened (includes completeness, neutrality, and freedom from error).

Enhancing Qualities:

Comparability: Information can be compared across companies.

Verifiability: Independent measurers obtain similar results.

Timeliness: Information is available before it loses relevance.

Understandability: Information is presented clearly and concisely.

Constraint: Cost of providing information should not exceed its benefits.

Assumptions and Principles in Accounting

Key Assumptions

Economic Entity Assumption: Business activities are separate from owners.

Going Concern Assumption: Company will continue to operate in the foreseeable future.

Stable-Monetary Unit Assumption: Money is the common denominator; ignores inflation/deflation.

Key Principles

Measurement Principle: Assets and liabilities are measured at historical cost or fair value.

Revenue Recognition Principle: Revenue is recognized when earned.

Matching Principle: Expenses are matched to revenues in the period incurred.

Full Disclosure Principle: Financial statements must include all information necessary for informed decisions.

The Accounting Equation and Elements

The Accounting Equation

The fundamental equation of accounting is:

Assets = Liabilities + Equity

This equation presents the resources of a company and the claims to those resources.

Assets: Probable future economic benefits (e.g., cash, receivables, inventory).

Liabilities: Probable future sacrifices of economic benefits (e.g., payables, debts).

Equity: Residual interest in assets after liabilities (contributed capital and retained earnings).

Elements during a period include investments by owners, distributions to owners, revenues, expenses, gains, and losses.

Financial Statements Overview

Income Statement

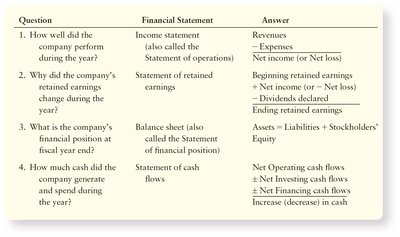

The income statement shows the results of operations (profitability) for a period of time. It answers "How well did the company perform during the year?"

Revenues: Increases in net assets from central operations.

Expenses: Decreases in net assets from central operations.

Gains: Increases from peripheral transactions.

Losses: Decreases from peripheral transactions.

Formula:

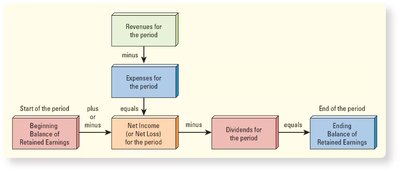

Statement of Retained Earnings

This statement explains how net income and dividends affect the company’s financial position over a period.

Retained Earnings: Accumulated earnings less dividends.

Formula:

Balance Sheet

The balance sheet shows the financial position of a company at a point in time. It demonstrates that the accounting equation is in balance.

Assets: Current and long-term resources.

Liabilities: Current and long-term obligations.

Equity: Contributed capital and retained earnings.

Formula:

Cash Flow Statement

The cash flow statement shows sources and uses of cash over a period, categorized into operating, investing, and financing activities.

Operating Activities: Cash flows from core business operations.

Investing Activities: Cash flows from buying/selling assets.

Financing Activities: Cash flows from borrowing/repaying debt and issuing stock.

Formula:

Notes to the Financial Statements

Notes provide supplemental information about the financial condition of a company, including accounting rules, additional detail, and disclosures about items not listed in the statements.

Linkages Among Financial Statements

The four financial statements are interconnected. Net income from the income statement flows into retained earnings, which appears on the balance sheet. The cash flow statement reconciles the change in cash, which is also reported on the balance sheet.

Summary of Key Concepts

Assets: Resources owned by the company.

Liabilities: Debts owed to outsiders.

Equity: Ownership interest and reinvested earnings.

Revenues: Sales from goods/services.

Expenses: Costs used up in generating revenue.

Income Statement: Shows profitability.

Balance Sheet: Shows financial position.

Retained Earnings: Net income less dividends.

Cash Flow Statement: Shows sources and uses of cash.

Liquidity: Ability to repay short-term debt.

Solvency: Ability to repay long-term debt.

Profitability: Ability to generate profit.

Annual Report: Contains the four financial statements.

Helpful Formulas:

Net Income:

Retained Earnings:

Equity:

Balance Sheet Equation: