Back

BackChapter 1: Financial Statements – Foundations of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Accounting: Introduction and Importance

Why Accounting Is Critical to Business

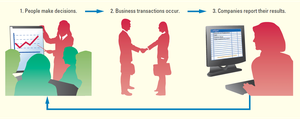

Accounting is an essential information system for all types of organizations. It measures business activities, processes data into financial statements and reports, and communicates results to decision makers. The accounting cycle is the process by which a company’s financial statements are prepared, ensuring that all transactions are accurately recorded and reported.

Measurement: Accounting quantifies business activities, such as sales, purchases, and payroll.

Processing: Data is organized and summarized into financial statements.

Communication: Results are reported to both internal and external users for decision-making.

Example: Disney’s $91 billion revenue in 2024 involved millions of transactions, all tracked and reported through accounting.

Decision Makers Who Use Accounting

Accounting information is used by a variety of stakeholders:

Individuals: Personal financial decisions.

Investors and Creditors: Assessing profitability and risk.

Regulatory Bodies: Ensuring compliance with laws and regulations.

Nonprofit Organizations: Accountability and stewardship.

Types of Accounting

Financial Accounting: For external users (investors, creditors, government agencies, public).

Managerial Accounting: For internal users (managers, budgets, forecasts, projections).

Business Organization Structures

Forms of Business Organization

Proprietorship: Single owner, personally liable for debts, distinct for accounting purposes.

Partnership: Two or more co-owners, income/losses flow through to partners, general (unlimited liability) or limited-liability partnerships.

Limited-Liability Company (LLC): Business is liable for debts, members have limited liability, income flows through to members.

Corporation: Owned by stockholders, legally distinct, can raise large capital, limited liability, subject to double taxation, governed by a board of directors.

Key Concept: Limited liability encourages investment by protecting personal assets of investors.

Accounting Concepts, Assumptions, and Principles

Professional Frameworks

Generally Accepted Accounting Principles (GAAP): U.S. standards set by the Financial Accounting Standards Board (FASB).

International Financial Reporting Standards (IFRS): Global standards set by the International Accounting Standards Board (IASB).

Conceptual Foundation of Accounting

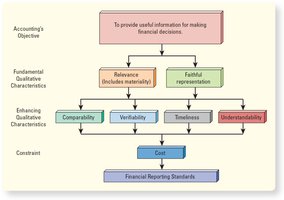

The conceptual framework ensures that accounting information is useful for decision-making. It is built on qualitative characteristics and subject to constraints.

Relevance: Information must be useful and material to users’ decisions.

Faithful Representation: Information must be complete, neutral, and free from error.

Enhancing Qualities: Comparability, verifiability, timeliness, understandability.

Constraint: Cost-benefit analysis of providing information.

Key Assumptions and Principles

Entity Assumption: Business is a separate economic unit.

Continuity (Going-Concern) Assumption: Entity will continue operating in the foreseeable future.

Historical Cost Principle: Assets are recorded at their purchase cost.

Stable-Monetary-Unit Assumption: The dollar’s purchasing power is assumed stable over time.

The Accounting Equation and Elements

The Accounting Equation

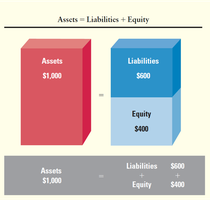

The accounting equation is the foundation of the balance sheet and expresses the relationship among assets, liabilities, and equity:

Assets: Economic resources expected to provide future benefit.

Liabilities: Debts owed to external parties.

Equity: Owners’ claims on the business (stockholders’ equity for corporations).

Accounts and Sub-Elements

Assets: Cash, accounts receivable, inventories, property, plant, and equipment.

Liabilities: Accounts payable, income taxes payable, long-term debt.

Equity: Paid-in capital (common stock), retained earnings.

Components of Retained Earnings

Revenues: Inflows from delivering goods/services; increase retained earnings.

Expenses: Outflows from operations; decrease retained earnings.

Dividends: Distributions to stockholders; decrease retained earnings (not an expense).

Gains/Losses: Inflows/outflows from activities outside main business operations.

Financial Statements and Their Relationships

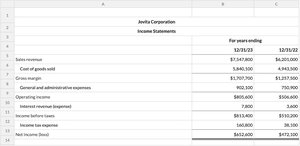

The Income Statement

The income statement (statement of operations) reports revenues and expenses for a period, resulting in net income or net loss.

Net Income: Revenues > Expenses

Net Loss: Expenses > Revenues

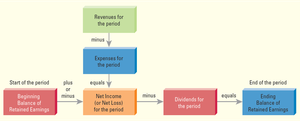

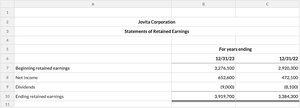

The Statement of Retained Earnings

This statement shows changes in retained earnings over a period. Net income increases retained earnings, while dividends and net losses decrease it.

Formula:

The Balance Sheet

The balance sheet (statement of financial position) reports assets, liabilities, and stockholders’ equity at a specific point in time.

Current Assets: Expected to be used or converted to cash within one year (e.g., cash, receivables, inventories).

Long-Term Assets: Benefit the company beyond one year (e.g., property, plant, equipment).

Current Liabilities: Debts due within one year (e.g., accounts payable).

Long-Term Liabilities: Debts due after one year (e.g., bonds payable).

Equity: Common stock, retained earnings, treasury stock, etc.

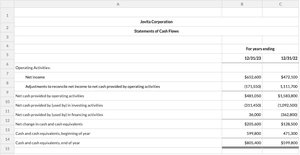

The Statement of Cash Flows

This statement reports cash receipts and payments, classified into operating, investing, and financing activities.

Operating Activities: Cash flows from core business operations.

Investing Activities: Cash flows from buying/selling long-term assets.

Financing Activities: Cash flows from borrowing, repaying, or equity transactions.

Relationships Among Financial Statements

Data flows from one statement to another. For example, net income from the income statement is used in the statement of retained earnings, which then affects the equity section of the balance sheet. The statement of cash flows reconciles the beginning and ending cash balances on the balance sheet.

Ethical Decision-Making in Accounting

Evaluating Business Decisions Ethically

Business and accounting decisions are influenced by economic, legal, and ethical factors. Ethical considerations ensure that actions are not only legal and profitable but also right.

Economic: Maximize benefits.

Legal: Comply with laws and regulations.

Ethical: Act with integrity, even beyond legal requirements.

AICPA Code of Professional Conduct

Responsibilities

Public Interest

Integrity

Objectivity and Independence

Due Care

Scope and Nature of Services

Accounting and ESG (Environmental, Social, and Governance) Practices

Role of Accounting in ESG Reporting

ESG reporting involves measuring and disclosing a company’s environmental, social, and governance performance. Accountants play a key role in preparing, assuring, and analyzing ESG data.

Frameworks: GRI, ISSB, UNGC, TCFD.

Examples of ESG Measures: Energy consumption, water usage, emissions, waste generation.

Accountant’s Role: Third-party assurance, internal reporting, analysis, and recommendations for improvement.

Accounting Careers and Professional Certifications

Career Path Options

External auditor

Management accountant

Internal auditor

Budget analyst

Financial analyst

Professional Certifications

CPA (Certified Public Accountant)

CMA (Certified Management Accountant)

CGMA (Chartered Global Management Accountant)

CIA (Certified Internal Auditor)

CFE (Certified Fraud Examiner)

The CPA exam covers accounting, auditing, tax, and a chosen discipline (business analysis, information systems, or tax compliance).

Tools and Technologies in Accounting

Spreadsheets

Spreadsheets (e.g., Microsoft Excel, Google Sheets, Apple Numbers) are essential tools for organizing, calculating, and visualizing accounting data.

Data Analytics

Data analytics involves transforming raw data into actionable insights, supporting trend analysis, process improvement, and decision-making.

Artificial Intelligence and Machine Learning

AI and machine learning automate complex tasks, such as data classification and predictive modeling, enhancing the efficiency and accuracy of accounting processes.

Robotic Process Automation (RPA)

RPA uses software bots to automate routine tasks, freeing accountants to focus on analysis and interpretation.

Technology Risks

While technology can improve decision-making, improper use can lead to significant errors or losses. Accountants must understand both the benefits and risks of technology.

Introduction to Excel

Excel is the most widely used spreadsheet program in business, supporting calculations, data organization, and visualization. Google Sheets and Apple Numbers offer similar functionalities.