Back

BackChapter 1: Financial Statements – Foundations of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Accounting: Introduction

Accounting’s Role in Business

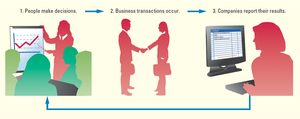

Accounting is a critical information system for businesses, enabling the measurement, processing, and communication of financial data. It supports decision-making by providing reliable financial statements and reports.

Measures business activities: Tracks financial transactions and events.

Processes data: Converts raw data into structured financial statements.

Communicates results: Shares information with internal and external decision makers.

Accounting cycle: The systematic process by which financial statements are prepared.

Decision Makers Who Use Accounting

Various stakeholders rely on accounting information for decision-making:

Individuals: Personal financial planning.

Investors and creditors: Assessing profitability and creditworthiness.

Regulatory bodies: Ensuring compliance with laws and regulations.

Nonprofit organizations: Managing resources and reporting to donors.

Types of Accounting

Accounting is divided into two main types, each serving different users:

Financial Accounting: For external users (investors, creditors, government agencies, public).

Managerial Accounting: For internal users (managers), focusing on budgets, forecasts, and projections.

Business Organization Structures

Forms of Business Organization

Businesses can be organized in several ways, each with distinct characteristics and implications for accounting:

Proprietorship: Single owner, personally liable for debts, separate entity for accounting.

Partnership: Two or more co-owners, income/losses flow through to partners, liability varies by partnership type.

Limited-Liability Company (LLC): Business liable for debts, members have limited liability, income flows through to members.

Corporation: Owned by stockholders, can raise capital via stock, limited liability, double taxation, governed by board of directors.

Accounting Concepts, Assumptions, and Principles

Professional Frameworks

Accounting standards ensure consistency and comparability:

GAAP: Generally Accepted Accounting Principles, set by FASB.

IFRS: International Financial Reporting Standards, set by IASB.

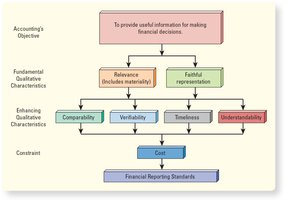

Conceptual Foundation of Accounting

The conceptual framework guides the preparation of financial statements, emphasizing relevance, faithful representation, and other qualitative characteristics.

Entity Assumption: Each organization is a separate economic unit.

Continuity (Going-Concern) Assumption: Entity will continue operating in the foreseeable future.

Historical Cost Principle: Assets recorded at actual cost.

Stable-Monetary-Unit Assumption: Dollar’s purchasing power is stable over time.

The Accounting Equation

Definition and Application

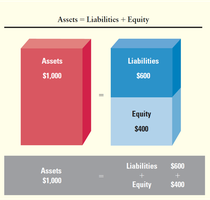

The accounting equation is the foundation of financial accounting, showing the relationship between assets, liabilities, and equity:

Assets: Economic resources expected to provide future benefits.

Liabilities: Debts owed to external parties.

Equity: Owners’ claims on assets.

Accounting Equation:

Components of Equity

Paid-in Capital: Investments by stockholders (common stock).

Retained Earnings: Earned income kept in the business.

Retained Earnings

Components and Calculation

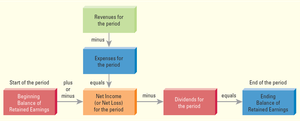

Retained earnings are affected by revenues, expenses, and dividends:

Revenues: Inflows from delivering goods/services; increase retained earnings.

Expenses: Outflows due to operations; decrease retained earnings.

Dividends: Asset distributions to stockholders; decrease retained earnings.

Retained Earnings Calculation:

Financial Statements and Their Relationships

Types of Financial Statements

Financial statements provide a comprehensive view of a company’s financial position and performance:

Income Statement: Reports revenues and expenses, resulting in net income or loss.

Statement of Retained Earnings: Shows changes in retained earnings over the period.

Balance Sheet: Reports assets, liabilities, and equity at a specific point in time.

Statement of Cash Flows: Reports cash inflows and outflows from operating, investing, and financing activities.

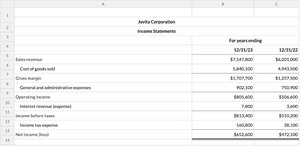

Income Statement Example

The income statement summarizes a company’s financial performance for a period:

Sales revenue minus cost of goods sold gives gross margin.

Subtract operating expenses and interest to arrive at net income.

Financial Statement Relationships

Data flows from one statement to another, linking net income, retained earnings, and balance sheet items.

Ethical Decision-Making in Accounting

Evaluating Business Decisions Ethically

Business and accounting decisions are influenced by economic, legal, and ethical factors. Ethical guidelines help ensure integrity and public trust.

Economic: Maximize benefits.

Legal: Comply with laws.

Ethical: Consider what is right beyond profitability and legality.

AICPA Code of Professional Conduct: Responsibilities, public interest, integrity, objectivity, independence, due care, scope and nature of services.

Accounting and ESG Practices

Environmental, Social, and Governance (ESG) Reporting

ESG reporting reflects a company’s commitment to sustainability and social responsibility. Accountants play a key role in measuring and assuring ESG performance.

Frameworks: GRI, ISSB, UNGC, TCFD.

Measures: Energy consumption, water usage, emissions, waste generation.

Accountant’s Role: Analysis, assurance, recommendations for improvement.

Accounting Careers and Certifications

Career Path Options

Accountants can pursue various career paths, including:

External auditor

Management accountant

Internal auditor

Budget analyst

Financial analyst

Professional Certifications

CPA: Certified Public Accountant

CMA: Certified Management Accountant

CGMA: Chartered Global Management Accountant

CIA: Certified Internal Auditor

CFE: Certified Fraud Examiner

CPA Exam: Four-section, 16-hour format covering accounting, auditing, tax, and a chosen discipline.

Tools and Technologies in Accounting

Spreadsheets

Spreadsheets are essential tools for organizing, calculating, and visualizing financial data. Microsoft Excel is the most widely used program.

Organizes data in rows and columns

Performs calculations and generates graphs

Other programs: Google Sheets, Apple Numbers

Data Analytics

Data analytics transforms raw data into actionable insights, supporting trend analysis, process improvements, and investment decisions.

Artificial Intelligence and Machine Learning

AI and machine learning automate complex tasks, enabling creative problem-solving and self-learning from data.

Robotic Process Automation (RPA)

RPA uses software bots to handle routine tasks, freeing accountants for higher-level analysis and interpretation.

Technology Risks

Proper use of technology enhances decision-making, while improper use can lead to significant errors.

Introduction to Excel

Excel’s interface includes features such as the ribbon, formula bar, worksheet tabs, and zoom slider, facilitating efficient data management.

Additional info: This guide covers foundational concepts from Chapter 1 of a financial accounting textbook, including the accounting cycle, business structures, accounting principles, the accounting equation, financial statements, ethical decision-making, ESG reporting, career paths, and technology tools.